Mini deep dive on Celsius Holdings ($CELH)

Typically all of my deep dives and mini deep dives are behind paywalls for paid subscribers only however this mini deep dive on CELH will be the exception.

Paid subscribers to Jonah’s Growth Stock Deep Dives receive ~3 deep dives per month (~8,000 words) and ~3 mini deep dives per month (~2,000 words) plus access to my current investment portfolio (up +134.7% in 2023 and up +1,130% since January 2020) plus my investment models and daily webcasts.

I also run a Stocktwits rooms where I post about my investment portfolio (up +134.7% in 2023) and my trading portfolio (up +97.3% in 2023) including morning newsletter, daily activity updates, daily charts, market/macro opinions, quarterly earnings analysis, daily webcasts and much more.

Over the past few years I’ve posted hundreds of times about CELH on Twitter, here are a few recent ones…

January 10th: https://x.com/JonahLupton/status/1745091263605485929?s=20

January 6th: https://x.com/JonahLupton/status/1743654052330688848?s=20

December 20th: https://x.com/JonahLupton/status/1737510731912749308?s=20

November 14th: https://x.com/JonahLupton/status/1724533782160560540?s=20

October 17th: https://x.com/JonahLupton/status/1714298178336420314?s=20

October 5th: https://x.com/JonahLupton/status/1709906449994772943?s=20

I’ve also done a bunch of posts about CELH on Substack, here is one from November 2022…

and here is a longer one from March 2021 which provides an overview of the company, their main products, business model, distribution strategy, etc — keep in mind that alot has changed (for the better) since this deep dive almost 3 years ago.

If you follow me at twitter.com/jonahlupton there’s a decent chance that some of the content in this mini deep dive will be repetitive but maybe it will be helpful to see it again.

Company: Celsius Holdings ($CELH)

Website: Celsius.com

Investor Relations: CelsiusHoldingsInc.com

Stock Price: $60.35

Shares Outstanding: 231.7 million

Market Cap: $13.98 billion

Net Debt/Cash: $759 million

Enterprise Value: $13.22 billion

Average Price Target: $72.50

MY PERSONAL BACKGROUND STORY with CELSIUS:

As some of you know, I’ve been a CELH shareholder for quite some time. I made my first purchase of CELH way back in May 2020 which means I’m up almost 2,000% on that first purchase.

Unfortunately that first purchase was very small, however over the past ~44 months I’ve added to my CELH position at least 100 times which means CELH has become a considerable part of my overall holdings.

In full disclosure, I recently moved 1/3 of my CELH shares into a separate account that I’m planning to leave alone for the next 5+ years because I not only believe in the long-term potential but selling CELH at these prices would trigger a large taxable gain. I also did this because all of my paid subscribers have access to my current investment portfolio and I thought it was irresponsible to show my full CELH position, I was fearful that a new subscriber would see my large CELH position and try to copy it without knowing the full backstory. My overall CELH position is very large because I’ve owned it for 3+ years and I’ve added dozens of times along the way. FWIW, my last CELH adds were ~4 weeks ago when the stock pulled back to the 200d ema and bounced along there for a couple weeks.

OVERVIEW OF CELSIUS:

I’m not going to get too deep into this overview section because that’s not what these mini deep dives are for, if you want to learn more about CELH you can read my twitter posts as well as my previous deep dives and quarterly updates. However I will cover the basics…

CELH is a healthy energy drink company, based in Boca Raton, FL that has taken the beverage industry by storm over the past several years. In that description I used the term “energy drink” which is more generic however the people that know this company best prefer the term “functional beverage” and if you’re someone like me that loves/craves caffeine (especially in the morning), you understand how “non-functional” we can be before we have our Celsius. For me personally, CELH helps me get through my day which starts at 5am with my work routine (chart reviews, newsletter, etc) and then my morning workout, all of which happens before I spend the next 8-10 hours sitting at my desk, staring at 6 screens (and trading), running multiple investment services for thousands of subscribers then I go back to the gym for another afternoon workout followed by sauna, music studio session and more work at my desk before trying to fall asleep around midnight. There’s no way I’m getting through this day without some caffeine and for me the option is simple, it’s Celsius or nothing. Not only do I love the taste of my favorite Celsius flavors (especially compared to coffee or other energy drinks) but I’m also getting some valuable nutrients and most importantly CELH gives me a sustained energy boost and not the spike/crash you get with most other products in the category ie Red Bull, Monster, Rockstar, C4, etc.

When I first invested in CELH they were fighting for warm shelf space and trying to grow their distribution through small regional operators but mostly doing DTR (direct to retailer) which means they were shipping product to stores (either directly or through the retailer’s distribution center) and then relying on employees to stock the shelves. Lots of young companies need to start with DTR but it’s not ideal especially for a beverage company that wants to be in the coolers.

Then in 2020, Bang left Anheuser-Busch and went over to Pepsi which opened the door for CELH to begin working with Anheuser-Busch. That really helped accelerate growth for CELH as they began to expand into larger retain chains and they started getting some cooler space (but not much). Over the next ~2 years, the # of stores that carried CELH grew by approximately 10x, going from 15k to 150k. Things were going well but Anheuser-Busch distribution is actually dozens and dozens of smaller regional operators which is much harder and more expensive to manage. Bang and Pepsi got off to rough start (for reasons I won’t discuss here) and then Bang got sued by Monster in 2 different lawsuits, both of which Bang lost for a total judgement of ~$500 million which forced Bang into bankruptcy. As this was happening Pepsi terminated their distribution agreement with Bang. Then, in August 2022 they announced they were investing $550 million into CELH for an 8.5% stake as well as taking over distribution. This was a gamechanger for CELH, the customers and the shareholders. Pepsi ($PEP) is not only one of the most recognizable brands on the planet but they’re also the largest beverage distributor so this was a massive win for CELH and opened the door to unlimited growth opportunities in the US and abroad.

Usually when I tell the CELH story to someone and try to explain how they’ve grown sales by 25x over the past 5 years I say it was a combination of the following… great product, great execution, great marketing and some luck. The first three are rather obvious at this point but the luck part has to do with Bang because if they had never left Anheuser-Busch then CELH may never have gotten a chance to work with a top 4 beverage distributor in the US and then when Bang lost those lawsuits it opened the door for CELH to work with PEP which may not have happened if Bang’s CEO wasn’t such a lying lunatic that single-handedly destroyed Bang and wiped out ~$6 billion of market value.

By the way, Monster ended up buying Bang in bankruptcy and is trying to revive the company but it’s not going well. Coca Cola is Monster’s distributor and that’s been a fabulous partnership for the past 10+ years however if Bang is going to get any cooler space it will come directly from Monster and Reign which means that any future success with Bang will probably be at the expense of Monster and their other brands.

Bang was becoming popular with the females and the fitness crowd but it’s safe to say that Celsius has taken over both of those demographics however I will mention that Ghost, Alani Nu, and several others are also trending higher but none of them are growing as fast as Celsius and none of them can work with Pepsi for distribution.

The consumer base for Monster and Red Bull is approximately 70% male and 30% female however I can’t remember the last time I saw a female drinking either of these products/brands. Celsius on the other hand is 50% male and 50% female so they’ve done a phenomenal job of appealing with women and I believe it’s for the following reasons:

women prefer the CELH flavor profiles

women prefer the CELH marketing message

women prefer the smaller CELH cans

If Celsius is going to get to 10% global market share in the next ~8 years it’s critical for them to have a large female consumer base and right now they’re definitely building one. Just spent 30 minutes on Instagram or TikTok, search for #Celsius hashtags and you’ll see thousands of consumers (especially females) talking about how much they love CELH.

I also know for a fact that CELH appeals to consumers of all ages, I know 16 year old’s that drink CELH and I know 80-year old’s that drink CELH, this is definitely not true with other brands like Monster, Red Bull, Rockstar, C4, etc.

The global coffee industry is valued at more than $550 billion so it’s at least 5x bigger than the energy drink industry, however the energy drink industry is growing ~2x faster than the coffee industry. This information doesn’t surprise me because I know dozens of people that have started replacing their daily coffee with a Celsius (this includes me); instead of having a coffee with breakfast and/or lunch, they now have a Celsius, same goes for that late-morning and/or mid-afternoon “pick me up” when you need some caffeine and now that person is drinking CELH for their caffeine needs.

FWIW, if the coffee industry continues growing at 4.3% per year and the energy drink industry continues growing at 8.5% per year than it would take 42 years for the energy drink industry to surpass the coffee industry. I’ll be pleasantly surprised if the energy drink industry is still growing this fast in 15+ years but it’s always possible especially if these energy/functional beverage products continue to get better and healthier which means they’ll continue to bring in new consumers.

INVESTMENT THESIS:

CELH is still one of my favorite stocks/companies and one of my highest conviction ideas for the next 5+ years but let’s be clear about something… the stock is up almost 2,000% since I started buying shares in May 2020 which means the “easy big” money has been made and nobody reading this mini deep dive should expect anything close to these returns over the next 5-10 years.

If almost everything goes right for CELH over the next ~8 years and they hit my estimates (in the chart below) then I think CELH has at least ~350% upside over the next ~8 years which would be a 21% CAGR — not bad and probably 2-3x higher than whatever the indexes do but it’s clearly less than the 110% CAGR I’ve gotten over the past ~4 years. As many of us know from being CELH shareholders, the stock can be very volatile with frequent pops and drops of 15% or more so it’s certainly possible some shareholders will see better than a 21% CAGR if they are trading around their core position, averaging down on pullbacks and/or using options to compliment their equity position.

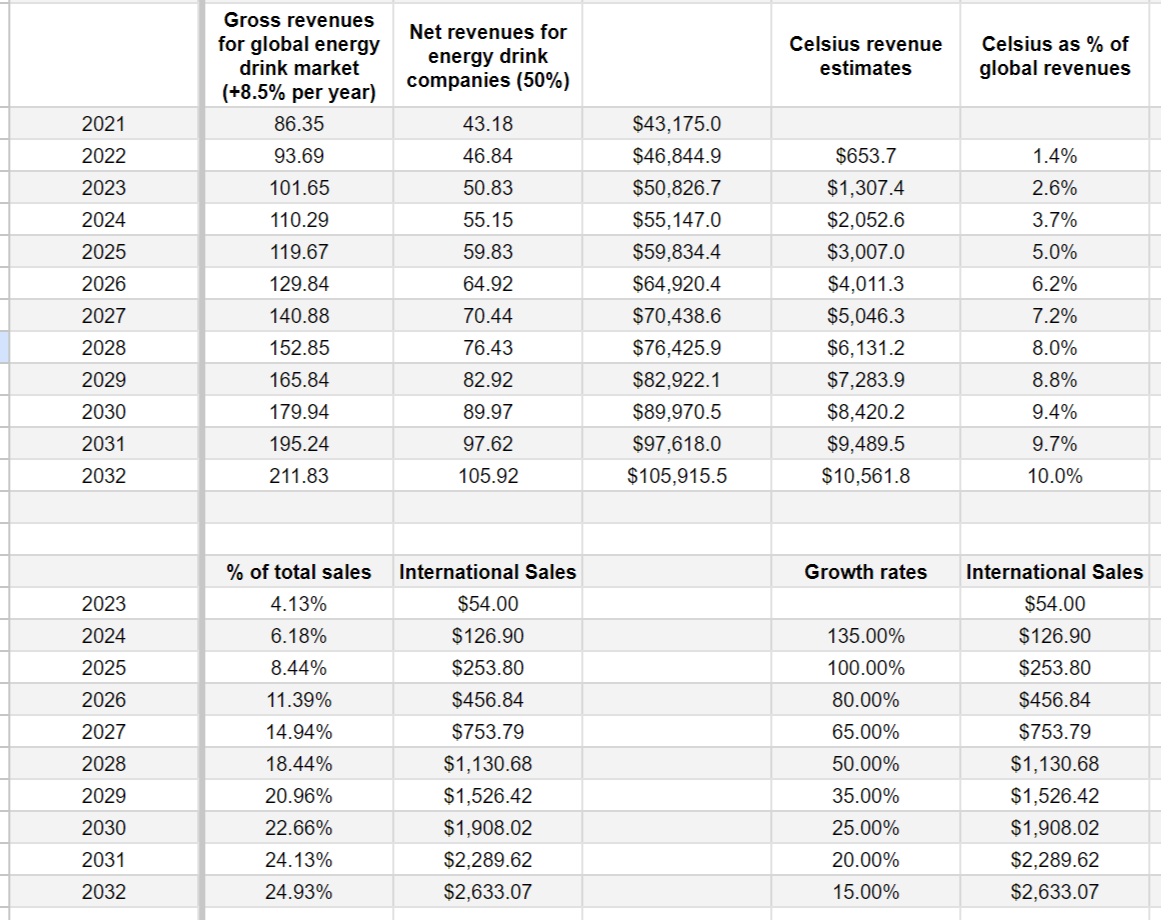

I mentioned my estimates in the paragraph above so here you go.. obviously the actual numbers will be higher or lower but these are my estimates for now:

I’m sure most of you are familiar with Monster and Red Bull which are the two largest energy drink companies in the world. Together they did approximately $18 billion in revenues in 2023 which means CELH (which should do at least $1.3 billion in 2023, we won’t know until they report their Q4 earnings) only does about 7% of their combined revenues. This just shows how much opportunity remains for CELH as they continue to take market share and expand outside of the US.

In 2024 the energy drink market is expected to reach ~$110 billion, growing at 8-9% per year which means it will double over the next 8-9 years (rule of 72). Currently, CELH gets less than 4.5% of their total revenues from outside the US versus 40-50% for Red Bull and Monster.

CELH is about to report it’s third straight year of triple digit revenue growth which is unheard of for a publicly traded company. When I invested in CELH in May 2020, they had just reported $75 million in revenues for all of 2019 and now less than 5 years later I believe CELH has a shot at $2+ billion in revenues for 2024 which is more than 26x revenue growth. Never in my wildest dreams did I think CELH would grow this fast but alot has gone right (including some luck) which I’ll get into a little bit later.

CELH growth rates in the US will begin to slow down (can’t grow triple digits forever) but some of this deceleration will be offset by international expansion which started last week with the announcement that CELH was now available in Canada. CELH is launching with 7-11 but will expand to many other large, national chains later this month. CELH is currently available in parts of Europe and Asia but it’s never been a priority for the company and Pepsi was never involved until now.

With regards to Canada they setup a separate website at Celsius.ca — the flavors are limited for now but that will certainly change. I’ve lost track of how many flavors we have in the US, if you count the 12 oz cans and the 16 oz cans I think we’re well past 30 flavors for now which some might say is too many but I love it because it means every consumer should be able to find a handful of flavors they really love but encourage them to continue trying new flavors. This image below is only about half of the flavors, I still can’t find an image of all of them together.

FWIW, my top 10 favorite flavors in order are:

Green Apple Cherry

Lemon Lime

Orangesicle (16 oz can)

Cherry Limeade (16 oz can)

Tropical Vibe

Mango Tango (16 oz can)

Grape

Oasis Vibe

Cosmic Vibe

Mango Passionfruit

I’m always amused when people tell me their favorite flavors because they are usually very different than mine. I know plenty of people that love kiwi guava and mandarin marshmallow but I’m not a big fan of either.

Pepsi has already made a huge impact in the US because they’ve opened a variety of new channels that CELH’s prior distributor (Anheuser Busch) could not have gotten them into including schools, hospitals, restaurants, bars, stadiums, movie theatres, airports, hotels and so many other places. This is why we saw massive revenue acceleration from the summer of 2023 through the summer of 2024 but now we’re seeing growth slow down because we’ve lapped the 1-year anniversary of Pepsi taking over distribution. As a reminder, when CELH was working with Anheuser Busch they were actually working with dozens and dozens of regional distributors whereas now they just work with Pepsi so everything on the operations side (manufacturing, shipping, fulfillment, etc) has gotten very streamline and efficient which is one reason why we’ve seen profit margins move much higher over the past 5+ quarters. I believe we’ll continue to see margins improve over the next 5-10 years, eventually we could/should see net income margins above 20% which is where Monster’s margins were pre-pandemic.

In my investment model I have net income margins (NIMs) improving by 75 bps per year, it’s possible this is too conservative if Pepsi is able to increase operational efficiencies while CELH is able to reduce S&M (sales & marketing) as a % of total revenues which is currently at 20% but I’d love to see that number start heading towards 15% as they continue scaling up revenues. NIMs improving by 75 bps per year would end up being too optimistic if we saw significant increases in freight costs, raw material costs, manufacturing costs, S&M costs, legal costs, payroll costs, etc — this is definitely something to watch going forward.

Currently CELH uses co-packers for manufacturing, I wonder if this will change at some point. Perhaps we’ll even see Pepsi takeover manufacturing which could increase additional cost savings for CELH. Now that CELH is expanding outside of the US they’ll need to add more manufacturing capacity/partners which will likely be localized to reduce excessive freight costs and comply with local regulations. CELH is not going to make product in the US and ship it to Germany or Australia. With regards to CELH product in Canada, I’m not sure if they’re making that product in Canada or the US, I’m sure we’ll get clarity on the Q4 earnings call. I know that CELH had to lower the caffeine content (down to 180 mg) and add different labels in order to comply with Canadian laws.

In the most recent Nielsen report it showed that CELH is still growing US retail sales by more than 100% but this number will continue to come down over time. Nobody expected CELH to keep triple digit retail sales growth as long as they did and it had to start slowing down at some point. We’re also dealing with much larger numbers now than we were when Pepsi took over. Keep in mind that CELH is still growing 10x faster than Monster and 20x faster than Red Bull.

I know that I’m bouncing around so hopefully you’re able to keep up with me, it’s hard to know exactly what to cover in this deep dive and which details to include.

I mentioned above that the energy drink market is expected to hit ~$110 billion in 2024, just to be clear those are gross revenues recognized by the end seller (retail store, Amazon, Costco, etc) so the net revenue number recognized by the energy drink companies is approximately 50% of that gross number or $55 billion. Since I believe CELH will do $2+ billion in revenues this year it means they could have 3.7% global market share by year end. I believe they can get to ~10% global market share over the next ~8 years. Keep in mind that Monster has ~16.5% global market share and Red Bull has ~20% global market share — I expect global market share for Red Bull and Monster to decline over the next 5-10 years thanks to Celsius as well as some of the other emerging brands like Ghost, Alani Nu, C4 and Prime.

Since I believe CELH has a chance to reach 10% global market share in ~8 years, here’s the road map on how it happens:

To be honest, I’m very curious to see how the international markets accept CELH compared to the US and whether the same marketing strategies that worked in the US will also work outside of the US.

If CELH is going to get to ~10% global market share in ~8 years then international needs to become a bigger piece of the overall pie, ideally getting to ~25% or more in 2032 which would still be only halfway to Red Bull’s international revenues as a percentage of their total revenues (~50%).

CELH has a much different consumer base than Red Bull and Monster… the average CELH consumer is younger and more female. I suspect these same trends will carry over to international markets given the brand image and flavor profiles. I have no doubt that CELH will be very successful outside of the US over the long-term but in the short-term I’m just wondering how quickly and aggressively Pepsi will take CELH into new regions and what the specific, localized sales/marketing strategy will be (versus the US or other regions) and perhaps most importantly is how much money will CELH/PEP need to spend to order to ensure successful launches in every region. Lots of questions that we won’t have the answers to for many more quarters.

I know that CELH has crushed it with Instagram and TikTok, on their own channels as well as partnering with influencers, athletes, etc so I’m assuming this marketing strategy will work almost anywhere in the globe especially Canada and Europe which will probably be the focus for 2024 then maybe we see Asia, Africa, Australia and South American in 2025 (just my guess).

PRODUCT PIPELINE:

Right now CELH has 3 main products which are the 12 oz cans (200 mg of caffeine), the 16 oz cans (280 mg of caffeine) and the powder sticks (great for traveling). They also have a BCAA product but I’m not a fan and I don’t know anyone that drinks them so I’ll leave them out for now. With regards to the 16 oz cans, these product line used to be called Celsius Heat but it was rebranded as Celsius Essentials back in December.

")

As far as I can tell, CELH has at least 24+ flavors in the 12 oz cans, 6+ flavors in the 16 oz cans and at least 9+ flavors in the powder sticks. It appears that CELH wants to keep adding more flavors (SKUs) for these three product lines which I’m totally fine with however there are 4-5 products that I hope CELH brings to market in the next 12-18 months…

100 mg product (10 oz can) — this would be ideal for people more sensitive to caffeine or the people that would like to drink a Celsius in the afternoon but don’t want the 12 oz can with 200 mg of caffeine

0 mg product (12 oz or 16 oz can) — I honestly believe a caffeine free product would be huge for Celsius because it would allow them to compete in the soda and seltzer categories which are both enormous

hydration product (20 oz or 24 oz bottle) — I’ve been a big Gatorade Zero drinker for the past couple years, I’ve also tried BodyArmor, Prime and several others but none of them would stack up against a Celsius hydration or intraworkout product. I think it would fit perfectly with the current brand image and consumer base

protein drink (20 oz bottle) — I’d be less excited about this product, not because I don’t think it would be awesome and generate some revenues but because there’s already a ton of RTD (ready to drink) protein products on the market including Fairlife, Premier Protein, Muscle Milk, Lean Body and dozens more. Just not sure it makes sense for CELH to get into the protein shake market.

BCAA product — CELH currently has a BCAA product but I think it sucks, it should be either discontinued or improved and it should not have caffeine in it. CELH should develop a new BCAA product that can be consumed intra-workout or post-workout, ideally with 10g of BCAAs (perhaps some creatine and other nutrients). There’s definitely some overlap in a hydration product and BCAA product, I believe there’s room for both since they do serve different purposes but I’d also be fine with combining these two into one amazing hydration/BCAA/intra-workout drink but the right way to do it would be separate products because my bodies needs during a workout are different than what I need after a workout when my muscles are depleted and better prepared to absorb the BCAAs and creatine for repair and recovery.

Not only do I think it’s important for CELH to expand the current product lineup in order to continue growing revenues and bring more consumers into the ecosystem, but CELH now has 20,000+ branded coolers placed in high-traffic retail stores/locations which are perfect for showcases products besides the 12 oz energy drinks.

If we don’t see any new products in the next 12-18 months I’ll be extremely disappointed and will probably my CELH position because it shows me that management isn’t willing to be as aggressive as I want them to be. It also shows me that Pepsi isn’t looking for CELH to launch any new products that might compete with their own products inside the coolers. Pepsi owns Gatorade so if we don’t see a hydration product from CELH it’s very possible that Pepsi was throwing up the roadblocks and I’m guessing that CELH would not develop any products that Pepsi wasn’t willing to distribute.

VALUATION:

As of Friday’s close, CELH has an enterprise value (EV) of $13.22 billion; I’m going to use my 2024 estimates because I honestly don’t care what the analysts think since they’ve been playing catchup for the past few years.

I believe CELH will do $2.05 billion of revenues this year with 49.5% gross margins, 23.0% EBITDA margins and 15.5% net income margins, these numbers/margins would result in $1.015 billion of gross profit (GP), $472 million of EBITDA and $318 million of net income (NI).

If CELH does indeed hit my estimates, the stock is currently trading at:

6.45x EV/SALES

13.0x EV/GP

28.0x EV/EBITDA

41.5x EV/NI (non-GAAP P/E)

CELH is not a cheap stock but it shouldn’t be when you consider the fundamentals (ie growth rates) because based on my estimates EBITDA would grow by 60-65% in 2024 and net income would grow by 60-65% in 2024 so paying 41x net income for 60% growth would be a bargain and justify multiple expansion over the next 6-12 months (assuming they hit my estimates).

Right now the analysts are looking for $1.8 billion of revenues with 21.1% EBITDA margins and 13.5% net income margins which means CELH is trading at 34.7x EV/EBITDA and 54.4x EV/NI, and CELH only does these numbers then I would agree the stock is fairly valued at current prices.

The only real comp for CELH would be Monster (MSNT) which current has an enterprise value of $58.5 billion with revenue estimates of $8.013 billion in 2024 with 54% gross margins, 30.9% EBITDA margins and 23.8% net income margins. Using these numbers MNST is currently trading at:

7.3x EV/SALES

13.5x EV/GP

23.6x EV/EBITDA

30.6x EV/NI

MNST looks a little bit more expensive on a couple valuation metrics and slightly cheaper on others but when you consider that MNST is only growing revenues by 12% and earnings by 15% the stock looks way more expensive than CELH. Given all the new competition that MNST is facing, I wonder if they can even hit $8 billion this year, in which case the stock is even more expensive than the numbers above would suggest.

CONCLUSION:

I’ll admit that my commentary might be a little biased but that’s because I’m a large shareholder and nobody (including the analysts) has been more right about CELH than me. With that said, I also believe there’s still plenty of upside to justify holding or even buying at these prices when you consider the total market size ($110B) growing at 8-9% per year, CELH global market share potentially going from ~2% to ~10% over the next 8-10 years, new product launches that expand the current TAM, growing international sales from ~4% of total sales to ~25% of total sales over the next 8-10 years, improving gross/profit margins with the help of Pepsi by increasing operational efficiencies, and so much more.

Now you know how large the energy drink market is today and how large it could be in ~10 years, if CELH can get to ~10% global market share in the next decade than the stock still has another 300-400% upside from here, maybe more if margins expand faster than my models and/or they expand their TAM but entering new product categories like hydration drinks, protein shakes, caffeine free, etc. in which case maybe we’re talking about $12-15 billion of revenues in ~10 years (assuming they are still an independent company).

The question I get asked the most is whether I believe Pepsi will someday buy CELH since they already have an 8.5% stake. Common sense tells me that Pepsi would love to own Celsius but like everything else it comes down to price. When PEP made that investment in August 2022 they got preferred shares at $25 which ($75 pre-split) looks like an incredible purchase price, I’m sure PEP regrets not investing more money for a bigger stake or perhaps just buying the entire company but they were coming off a broken partnership with Bang not to mention the $4+ billion disaster with Rockstar so I’m sure the Pepsi management team wasn’t about to drop $10-15 billion to acquire CELH until they got the product into their system and had a better idea of how quickly international sales could ramp up. I certainly don’t blame PEP for taking this more conservative approach however the decision to wait on an acquisition could be a costly one because they might have been able to buy CELH last August for $10 billion but an acquisition today would cost at least $20 billion.

In case you didn’t know, approx ~9 years ago Coca Cola ($KO) was already distributing MNST but they decided to invest $2.1 billion for a 16.7% stake which valued MNST at $12.5 billion. This turned out to be quite an investment because that stake in MNST is now worth ~$12 billion — a pretty sweet 470% ROI for Coca Cola. I guarantee KO executives which they had just acquired MNST back in 2015 and I’m sure PEP executives don’t want to make the same mistake. If CELH does indeed grow into a $60 billion company over the next decade than PEP could certainly justify paying $20 billion for that asset today which would be a 200% ROI.

In all honesty, I don’t care if PEP buys CELH or not. If it happens I hope it’s not for a few more years but I have plenty of high-conviction stock ideas to redeploy my CELH proceeds and if an acquisition doesn’t happen I’m more than happy to hold my CELH shares for the long-term as long as the fundamentals remain strong and valuation remains reasonable.

Over the past ~3 years CELH has had at least 11 pullbacks of 23% or more with an average pullback of 34%, however many of these bigger pullbacks were before the Pepsi deal which really helped change the narrative and give credibility to the company/story so it’s very possible we don’t see anymore 40% pullbacks for CELH which means if that’s what you’re waiting for to start buying shares than your opportunity may never arrive and I’d argue if CELH did drop 40% would you have the nerves to actually buy or just keep waiting for it to go lower but never actually pull the trigger.

CELH is up +24% in the past couple weeks after pulling back -29% from the all-time high in September. Even though I have a large position I’d consider adding to my position if the stock pulled back to the 50d sma at $54 and then again at the 200d sma ~$50, there’s really no reason for me to add above $60.

If you’re looking to start a CELH position but worried the stock might pullback I’ll give you the same advice that I give my friends which is start a 1/3 position. If the stock rips higher than you’ll be glad you bought some shares. If the stock pulls back you’ll be glad you only had a 1/3 position and now you can average into a larger position at lower prices. This strategy is a win/win and one that I often use in my own investment portfolio.

For instance, early last year I started small positions in ONON and SDGR. Shortly afterwards ONON crushed earnings and popped 60% in just few days. SDGR got caught up in the AI-hype cycle and went up 200% in just a few months so I was able to sell and lock in the gains. Looking back I wish I had started bigger positions but I was glad that I at least had a 1/3 position in both.

I’m going to end it there. I’m sure I could have made this mini deep dive 5x longer and still just scratched the surface of my CELH thoughts and investment thesis but I think I covered most of the main points that I wanted to. Perhaps after CELH reports Q4 earnings and provides more clarity on their international growth plans for this year I’ll be able to put together a follow up note. I guarantee as soon as I hit send I’m going to remember 5 things that I wanted to include in this deep dive but forgot about until now. Oh well.

Please feel free to share this CELH mini deep dive with your friends.

Have a great week,

Jonah Lupton

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.