Deep dive writeup on Matterport ($MTTR)

For all subscribers

In addition to my Substack newsletter, I also run a Stocktwits room where I post my current holdings, buys & sells, investment models, technical analysis and market commentary for both my Investment Portfolio (long term, strong fundamentals, 20-30 holdings) and my Trading Portfolio (short term, strong technicals, 0-10 holdings). The two options are $15/month for the monthly plan [click here] or $150/year for the annual plan [click here].

You can now signup for my new Substack called Jonah’s Trading Charts which is focused exclusively on the technicals — every day (usually pre-market) I’ll send out an email with my favorite trading charts/setups. You’ll also have access to my trading portfolio with current positions/sizes, entry/exit prices, profits/losses and much more. I’m also doing live charting and live trading 3-4 times per week.

Company: Matterport

Ticker: $MTTR

Website: Matterport.com

Founded: 2011

Current stock price: $8.00

52 week high: $37.60 on December 1, 2021

52 week low: $7.50 January 28, 2022

IPO date: July 23, 2021 — this is when the company deSPAC’d from $GHVI and started trading under $MTTR, you can read more here [click here]

Outstanding shares: 261.7 million

Current market cap: $2.1 billion

Current enterprise value: $1.8 billion

Headquarters: Sunnyvale, CA, United States

Number of employees: 500+

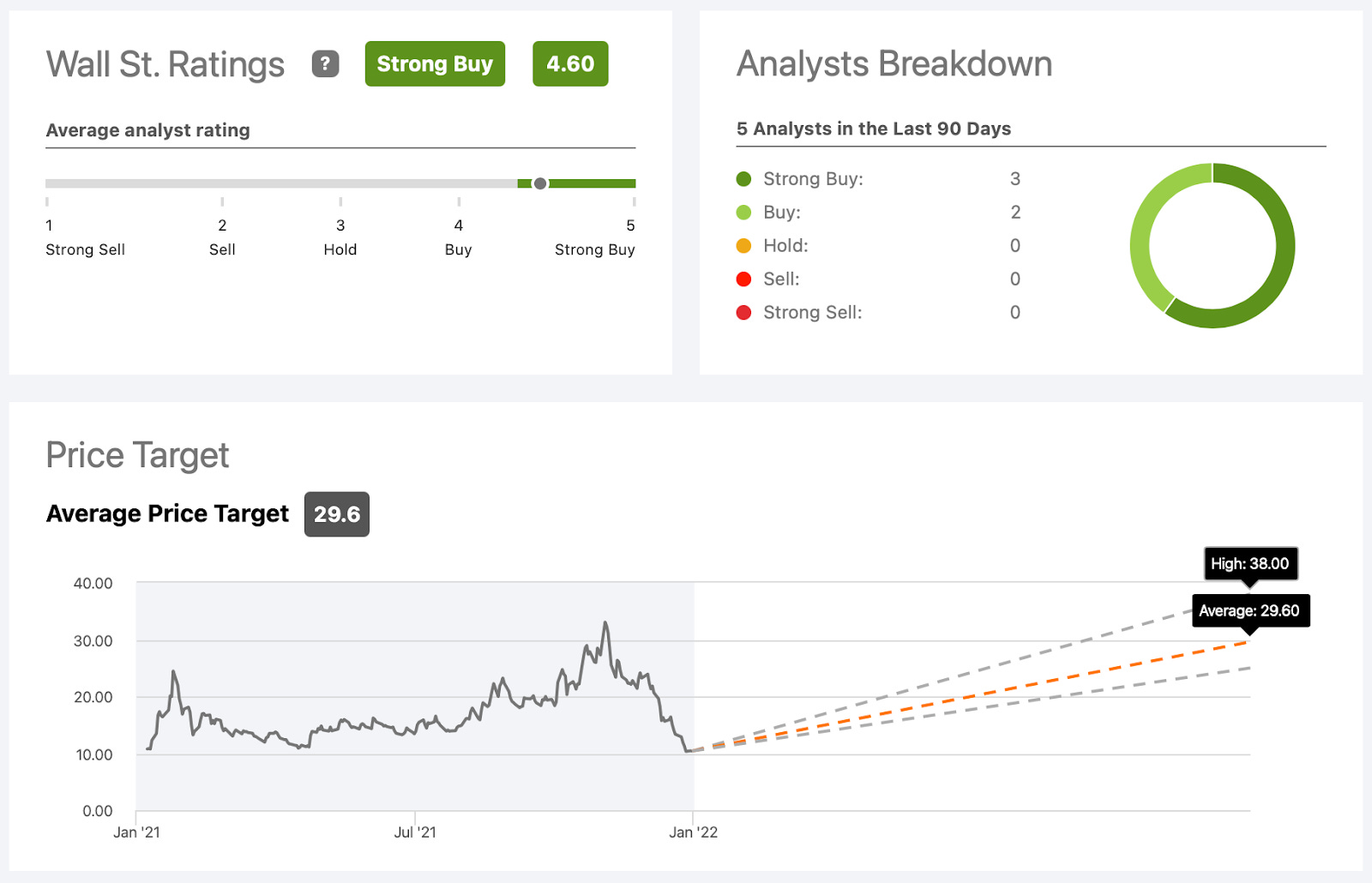

Average price target from analysts: $29.60

Investor relations [click here]

2021 Q3 earnings report [click here]

2021 Q3 earnings presentation [click here]

2021 Q3 earnings call transcript [click here]

Wells Fargo 5th Annual TMT Summit, December 2021 [click here]

Matterport hires Tom Klein as Chief Marketing Officer [click here]

More company related news [click here]

INTRODUCTION:

First off I want to disclose that I do not currently have a position in $MTTR but it’s definitely on my watchlist. I find $MTTR very intriguing for all the reasons we’re going to discuss in this writeup. I believe their “digital twins” and the spatial database they are building will provide massive value for all sorts of companies in the future from real estate to logistics to retail to hospitality. There’s certainly a chance that I could start a position in $MTTR after they report 2021 Q4 earnings and give us some 2022 guidance.

I did own $MTTR for several months last year from $16 to $24 but sold the stock after they reported Q3 earnings because I wasn’t impressed enough with the growth and monetization for a $6B company — I was worried the stock would selloff on a re-rating via multiple contraction. Unfortunately for me, the stock did the opposite and rallied all the way up to $37.60 on December 1st because of all the hype around the “metaverse”.

However, over the past 2 months $MTTR has dropped 78% from $37.60 down to $8.20 and I’m still not sure we’ve seen the lows. $MTTR has not announced when they’re reporting Q4 earnings — if that report is disappointing it’s very likely the stock drops even further. The market likes to overshoot in both directions — clearly $MTTR was overvalued in the mid $30s but it’s possible it’s not undervalued in the single digits. This next earnings report will give us some much needed clarity around the proper valuation.

I hope you enjoy the writeup on $MTTR and please let me know if you have any questions.

I worked on this $MTTR writeup with Dan, you can find him at @10baggerdan

MATTERPORT IN 90 SECONDS:

BACKGROUND:

Matterport was founded in 2011 by Matt Bell and Dave Gausebeck. Right from the beginning, the company attracted a lot of attention for its technology from well-known investors in Silicon Valley. After going to Ycombinator in 2012, the company raised over $100M in several investing rounds before going public in late July 2021 via a merger with a special purpose acquisition company (SPAC).

Matterport emerged on the back of the 3D printing boom in the early 2010s. The founders invented a small scanner that could scan any space or object and then create a 3D model. At that time, their technology was truly remarkable and disruptive.

“We turn reality into 3D models and our scanner is 20 times faster and 18 times cheaper than any other tool on the market,” says Matterport co-founder Michael Beebe, “We are creating fundamentally new technology, like the steam engine or the car.”

Until 2018, the company focused mainly on the residential real estate market. They became the gold standard in creating 3D virtual tours. But that has changed with the appointment of RJ Pittman as a CEO, who had much bigger ambitions for the company than just a place for 3D walkthroughs. He saw Matterport as a spatial data platform.

"So I posed a question to the investors, board members, and founders: "Have you ever thought of being a data company? What if you unlocked all of the insights that are trapped inside each and every Matterport space?” And they all said, “We’re in.” They were ready to turn Matterport into a platform business.", said RJ Pittman in one of his early interviews as a CEO.

That's how Matterport has pivoted and became the company we know today – the world’s leading platform for the digitization and datafication of the built world.

By turning buildings and spaces into digital twins, Matterport unlocks spatial data insights to better design, build, promote, and manage the most valuable asset in the world.

OPPORTUNITY:

According to Savills World Research, there are around 4 billion buildings (20 billion spaces) in the world, representing $230 trillion in total property value. It is by far the largest asset class, and it remains largely offline.

With the world rapidly shifting to online with the help of technology, the digital transformation of the built world, the largest undisrupted market, is just getting started. Approximately only 0.1% of all buildings are now digitized, making it one of the biggest opportunities to capitalize on.

But turning a building into a 3D digital twin is just one part of the opportunity. The greater value comes from the insights that can be gathered from spatial data of these 3D digital twins.

Imagine you want to know the average square feet of apartments in New York or how many light bulbs are used in the office building with seven floors in Canary Wharf, London.

Today, Matterport transforms buildings into data, and tomorrow that data will increase the value of every building. Matterport does something similar to what Google (now one of the most valuable companies in the world) did a decade or so ago by indexing the world wide web with all its knowledge and information and making it available to everyone in the world. Matterport is indexing the built world and already making it available for others. It will eventually create absolutely new business models and opportunities for industries like hospitality, facilities management, insurance, construction, real estate, retail, and others.

But the opportunity for Matterport does not end there. There is a lot of hype now surrounding the metaverse, and with the recent collaboration between Matterport and Meta (FB) on creating the world's largest dataset of 3D spaces for academic research, many started to believe that Matterport could be the leading facilitator to Meta's desire of building the metaverse world where physical spaces like museums, landmarks, theaters, to name a few will transform into online 3D objects that could be used with VR headsets. It gets even more interesting because all digital twins created on Matterport's platform are already VR-ready and supported by Oculus. I won't speculate on metaverse at this stage, but if it is somewhat true, it provides huge optionality for Matterport in the future and makes an investment thesis even stronger.

TECHNOLOGY:

Capture Devices:

It all starts from the devices that can capture spaces and objects. There is a solution for any space of any size, scale, and difficulty: from homes to high-rises, from one-room layouts to complicated floor plans.

Users can create digital twins with a wide range of cameras (LiDAR, spherical, 3D and 360), as well as smartphones (on iOS and now also on Android).

Matterport Capture App:

All capture devices must connect to the Matterport mobile app available both on iOS and Android. The app allows users to quickly capture depth, data, and imagery of a space as simple as a press of a button, making the entire process completely automated.

The captured images are then uploaded to the Matterport Cloud, where the processing of assets happens.

Matterport Cloud:

Matterport Cloud is powered by Cortex, an AI-powered software engine that turns scans into interactive 3D models.

Cortex includes a deep learning neural network that uses the spatial data library to understand how a building or space is divided into floors and rooms, where the doorways and openings are located, and what types of rooms are present.

Cortex can also identify and classify the contents inside a building or space, like doors, windows, light fixtures, etc.

Matterport Workshop:

Once the processing is completed and the digital twin of the captured space is created, the user can edit it in the Matterport Workshop, a desktop app that allows customizing, adding additional details, measuring, labeling, and sharing digital twins with others to further collaborate on them.

Users can also access aggregated property trends and operational and valuation insights.

Matterport Showcase App:

The final version of the digital twin can be shared with others via a standalone app (available both on iOS and Android) or through a web app (available in any browser).

The app allows users to experience the space in several modes: walk-through mode, dollhouse view, and floor plan mode. It can also be viewed in VR, using WebVR.

There are other features like embedding into any website, publishing to Google Street View, VRBO, Realtor.com and other platforms, sending schematic floor plans, and many more.

Matterport Platform Ecosystem:

The future of Matterport lies in its platform approach that allows any third party to develop an app (through an API and with the use of Matterport's SDK) on top of the existing functionality and further extend the platform capabilities.

Moreover, Matterport is working on the marketplace (similar to what Shopify did several years ago) for software add-ons (that will also enable a new revenue stream for the company). Third-party developers will be able to sell or license (through a recurring subscription) these add-ons to any Matterport user.

REVENUE MODEL:

The company's revenue model is a classical representation of a transaction-based model where revenue is generated by selling a product or service directly to a customer where the price of the product or service is formed from the production costs and a margin.

Matterport used to make only one-time sales, but not so long ago began a switch to a hybrid type of transaction-based model, where the user starts from a freemium plan and then moves to a paid subscription after a certain limit is reached.

What is interesting with Matterport's freemium model is that it only includes one user and one space and lacks sharing and embedding features that are only available in the paid plans (starting at $9.99 per month). The company allows trying the core of the product – creating a digital twin. But if a user wants to use it for commercial purposes, it requires a paid subscription. This approach should help the company dramatically accelerate the conversion of free users into paid ones in the upcoming years.

Apart from subscriptions that account for 57% of total revenue as of Q3 2021, the company generates revenue from several other streams:

Products (30% of total revenue) – sales of Matterport Pro 2 camera (starting $2,795) and accessories;

Services (12% of total revenue) – on-demand capture services provided in the US, the United Kingdom, France, Netherlands, Ireland, Canada, and Singapore, priced by the size of the space (starting $129) + additional services such as schematic floors plans and MatterPak™ technical files;

License (<1% of total revenue) – access to spatial data of all 3D digital twins captured on Matterport platform to date.

The company currently goes through a transitional period of moving away from the one-time sales model to subscription-only. It will provide more stable and projected revenues with a much higher gross margin. For example, the license revenue stream will totally transform from one-off payment to subscription in the next few years. By 2025 the company wants to reach 86% of the total revenue generated from subscriptions of different types. That is where I see the long-term growth opportunity for the company.

I also believe that over time Matterport will add additional revenue streams as they will explore more applications of its technology and spatial data they collect.

COMPETITIVE ADVANTAGES:

Matterport has several competitive advantages (also called Moat) that help the company differentiate and protect itself from its competitors.

But let's first look at the competition. Matterport is not the only company operating in this field. There are a number of alternatives that offer similar features and services. Below is the list of companies worth looking at:

Metareal – the new kid on the block that tries to copy-paste most of the Matterport's main features like a dollhouse view. Their technology allows making floorplans and 3D virtual tours from 360 photos. The tours are created by their staff in semi-manual mode. There is no option to shoot with the phone, only with selected 360 cameras. There is also no mobile app. The Metareal plans look cheaper than Matterport's, but only for hosting. Since Metareal builds 3D tours for its customers, they will charge bizarrely high fees for this. This solution is only suitable for those who know how to work with 3D modeling and build tours themselves.

Asteroom – an all-in-one 3D tour solution that also offers similar features like Matterport, including a dollhouse view. Asteroom has a mobile app, and it allows to shoot with the phone. The company offers to build a tour for the customers and charges a fee per tour. The fee includes hosting for 180 days. After that period, the customer needs to pay an additional fee for extending the hosting. The company also offers to hire a professional that will do all the work for the customer. The pricing is higher than Matterport offerings for the same service.

Cupix – positions itself as the industry's most advanced 3D digital twin platform. However, their solution is mainly designed for the construction industry, in which Matterport had historically shown less interest (maybe until recently when they introduced the BIM File offering). Cupix does have a separate 3D virtual tour solution built on their main platform, but it works only with a few 360 cameras and costs three times higher than Matterport (for the starter plan). Although the platform itself is rich in features and looks quite promising.

EyeSpy360 – offers the creation of 3D tours and floor plans. They position themselves as a 360 Virtual Tour Platform. However, there is no platform as such. Users just upload 360 photos of their spaces, the company does the work (most likely manually) to transform these photos into a virtual tour, 3D model, and floor plans, and then returns them to the user within a specific time frame. The company charges a processing fee ($15 per space) and then a monthly subscription fee ($19.99) for hosting and some additional features with minimal customization and editing capabilities. The company also offers professional services for capturing spaces (starting at $249 per space). Both offerings are more expensive than Matterport's.

Zillow 3D Home Tour – the most-visited real estate website in the United States has its own solution that offers the creation of virtual tours that can be added to listings. It is a do-it-yourself solution with quite limited features, and it is offered for free to anyone with a paid subscription for Zillow's main products. However, it only works with the Zillow platform (only in the US) and could not be brought outside their ecosystem.

It is important to mention that big companies like Nvidia (Omniverse), Microsoft (Azure Digital Twins), and Amazon (AWS IoT TwinMaker) are also working on something in virtual world space, but their products are much more complex, have different applications, and are targeted at very large enterprises.

After analyzing the competition, I came to the conclusion that Matterport is a true leader in the space of its core competence. Other solutions address only a portion of the functionality and value that the Matterport platform provides. Moreover, Matterport has the first-mover advantage. Being on the market for over a decade, they have almost half a million subscribers and over 6 million spaces under management, which is at least 100 times more than the rest of the market combined.

Being the first-mover also helped the company create the most extensive library of spatial data that continues to compound and enhance with more and more spaces added every day. This creates strong network effects.

The massive spatial data library itself is a significant advantage. I doubt anyone could ever replicate anything even slightly close to what Matterport already has.

Matterport also holds some critical patents (38 issued and 28 pending patents) on the capture technology side. Its software framework enables support for a wide variety of capture devices. No one in this space can offer that. Only Matterport can produce true, dimensionally accurate 3D results while automatically creating a final product in photorealistic 3D. The ability to easily capture spatial data removes friction to the adoption and scale of the Matterport platform.

And Matterport's brand also plays a vital role. The company has been carefully building a brand in the past ten years that now helps them attract and maintain subscribers. I had a chance to speak with some people from the real estate industry, and every single one of them at least heard about Matterport before.

And finally, now with access to public capital, Matterport will strengthen its position as an innovative leader and break away even further from anyone who would want to compete with them. If needed, most of the competitors are small companies that Matterport could buy out anytime.

CUSTOMERS:

According to Matterport's management, the total addressable market (TAM) for 3D reconstruction is estimated to be more than 20 billion spaces across the world. The company is looking to serve (serviceable addressable market or SAM) around 1.3 billion spaces (6.5% of TAM). As of Q3 2021, the company served just under 6 million spaces, representing <1% of SAM.

Matterport serves customers of all sizes, at every stage of maturity, from individuals to large enterprises. Though the company sees opportunities for growth across all of their customer segments, they are particularly focused on enterprise customers, ranging from Fortune 100 companies to small-and-medium-sized businesses.

These enterprise customers are concentrated in 6 different verticals:

Real Estate – by far is the largest vertical for the company right now, delivering 2/3 of all revenues in Q3 2021. The company actively targets major residential and commercial real estate brokerages and internet real-estate websites like Redfin. For real estate, whether it is an agent, a broker, or a property manager, Matterport's 3D virtual tours can increase commissions, reach a wider audience, and close on properties faster. Statistics show that 74% of agents using Matterport win more listings.

Travel & Hospitality – is very similar to the Real Estate vertical. For travel & hospitality, whether it is vacation rentals, hotels, or event spaces, Matterport's 3D virtual tours can increase bookings, drive higher occupancy rates, and increase engagement rates. Statistics show an increase of 14% in bookings and over 300% greater engagement with 3D tours vs. 2D images.

Insurance – the fastest-growing vertical for Matterport. Insurance companies can more precisely document and evaluate claims and underwriting assessments with efficiency and precision. From Q3 2021 Earnings Call: "For insurance, building owners can quickly document a home, assets, warranties, upgrades, personal property, and even keep active records of how the property, its contents, and condition have changed over the years. They can also easily capture a Matterport model on a loss to quickly document things such as subrogation, insurance fraud, sub-bids, approval questions, and resolution disputes."

Public Sector – is the newest vertical introduced by Matterport in late August 2021. Matterport deployed the first government-compliant 3D spatial data platform for the modeling of interior spaces on AWS GovCloud, intending to digitize all government facilities and infrastructure. From Q3 2021 Earnings Call: "The market opportunity for digitizing the public sector is substantial, spanning federal, state and local government agencies, the segments include education, law enforcement, military, infrastructure and health care, building assets, infrastructure and other physical spaces within the U.S. Federal government alone exceeds $260 billion in value, according to a study done by the Obama administration in 2017, representing hundreds of thousands of buildings and spaces and infrastructure budgets that are measured in the trillions of dollars in the U.S. alone." Here is an example of what Matterport's solution can provide to governments: in the event of an incident or crisis, the police and fire departments will now have detailed knowledge of the building layout, ingress, egress, and where the critical infrastructure is located from a remote location and long before entering the building.

AEC (architecture, engineering and construction) – a vertical that Matterport has neglected for too long but with the recent introduction of BIM files, Matterport is finally getting serious about it. From Q3 2021 Earnings Call: "Creating a digital BIM enables those who interact with the building to optimize their actions, resulting in a greater whole life value for the asset. Using software, such as Autodesk Revit, professionals can create models for conceptual design, visualization, analysis and construction. Until now, it has required a considerable amount of measurements and CAD translation labor to put all the data into the system to realize the full benefits of BIM. The process can take several weeks or longer, depending on the size and complexity of the project. Today, we are speeding this process up dramatically with the launch of the Matterport BIM file add-on service, available to every Matterport digital twin on the platform. Our customers can quickly transform a Matterport digital twin into a ready-to-use Autodesk BIM file at the click of a button. Receiving the final output in days versus weeks or months, and most importantly, delivered at a fraction of the cost."

Industrial & Facilities Management – the last vertical for Matterport as of now. Matterport offers the most efficient, effective method to survey the existing buildings and report on the building layouts and conditions to manage maintenance and develop remodeling plans. For facilities management companies, Matterport's digital twin gives immersive access to critical building intelligence, including accurate measurements of the structure and dimensions of the equipment within.

Matterport generates the most significant portion of its revenue from enterprise customers, but there is no customer concentration. No more than 10% of the total revenue is generated from the top 10 customers. This is possible thanks to Matterport's global reach.

Matterport is truly a global company with a significant presence in North America, Europe and Asia. They have separate leadership teams and a go-to-market infrastructure in each of these regions. In total, the company has customers in more than 150 countries. International markets are where the company sees additional growth potential, as currently, they represent only 35% of all revenues.

And it seems customers of all sizes and from different locations love the product. Matterport has tens if not hundreds of case studies on its website. In addition, Matterport has a solid rating (4.6/5) on the App Store with more than 1000 ratings in the US alone. The app on Google Play has just recently exited from beta and requires more time for ratings to be collected.

Matterport will eventually extend use cases and introduce new applications to drive subscriber growth further. The company strives to expand to entirely new industries such as manufacturing and oil and gas. With plans to increase investments in industry-specific sales and marketing initiatives, the number of enterprise customers around the world is projected to increase many-fold in the upcoming years.

MANAGEMENT:

Only one of the two founders is still involved in the company. Dave Gausebeck is the Chief Scientist Officer at Matterport. He leads the technological research and operations in the company. The other founder, Matt Bell, left the company in late 2017 after a number of disagreements with then CEO, Bill Brown.

Bill Brown had worked in the CEO role for almost 6 years, from 2013 till 2018. Brown's role in Matterport's growth was immense. While Bell and Gausebeck were mostly visionaries, Brown is the one who took the company from pre-revenue and pre-product to a market-leading company in this space.

Eventually, R.J. Pittman replaced Bill Brown in late 2018. He was the perfect fit for this role. Being an entrepreneur, product developer and real estate investor, Pittman had all the right qualifications to take the company to the next level.

Here’s my interview with the CEO of $MTTR from September 2021:

Pittman’s career spans startups, venture capital, and the biggest companies in technology. Before joining Matterport, Pittman spent five years leading product, design, engineering, mobile, payments, and brand as CPO for eBay. Prior to eBay, he led the global e-commerce platform for Apple’s online stores and led product innovation for Google’s next-generation consumer search properties. Pittman also served as a co-founder and CEO of Groxis, the advanced search engine technology company that created the industry’s first graphical information interface used by hundreds of prominent content services, including Google, Yahoo, and Amazon. Alongside his career in technology, Pittman has spent more than 20 years following his passion for design, architecture, and real estate development. He has been involved in dozens of innovative real estate projects throughout the US and the UK, affording him a unique perspective on the profound impact of technology on the built environment.

Alongside Pittman, the company is full of other experienced executives, whose average tenure in the company is over three years.

JD Fay, Chief Financial Officer

Jay Remley, Chief Revenue Officer

Japjit Tulsi, Chief Technology Officer

Dave Gausebeck, Chief Scientist/Co-Founder

Matterport's Board of Directors is relatively small compared to the average board of public companies but well experienced. Apart from Pittman, there are just three more members:

Mike 'Gus' Gustafson – has 30 years of experience leading multiple technology companies and teams, including public and private, enterprise SaaS and infrastructure/software offerings, high growth businesses from pre-revenue to multi-billion dollar revenues. Board member since 2018.

Peter Hebert – the co-founder of Lux Capital, for which he has served as the Managing Partner since 2000. Hebert is an early investor in Matterport and dozens of other successful companies. Board member since 2013.

Jason Krikorian – has served as a General Partner of DCM, an international venture capital firm, since 2010 and is the co-founder of Sling Media, the DCM-backed pioneering digital media company that created Slingbox. Board member since 2014.

All board members are owner-oriented, as they all hold a significant portion of the company directly or through their firms.

CULTURE:

Matterport is a mission-driven company. Its mission statement goes as follows: "To digitize and index the built world."

The company has set out to fundamentally improve the way people understand and interact with the physical world. They strive to change how homes are bought and sold, retail stores are planned out, hotels or vacation homes are marketed, facilities are managed, and design and construction projects are completed.

To deliver on its mission, the company has committed to creating a workplace that is innovative, forward-thinking, and inclusive.

The company centers its work on three core values:

Think like leaders (all team members share the responsibility to deliver success)

Act to be inclusive (the company seeks out different voices, engage in honest conversations and gain new perspectives through its speaker series)

Help the customer win (make the technology that helps customers)

Diversification plays a crucial role in the company's culture. Being a global company, they don’t just value differences – they prefer them. The company created Employee Resource Groups for the black, Latin, and AAPI communities, women, and LGBT. These groups offer a safe platform to begin conversations and connect on a deeper level with other employees. Interesting fact, 40% of all Matterport's employees are women.

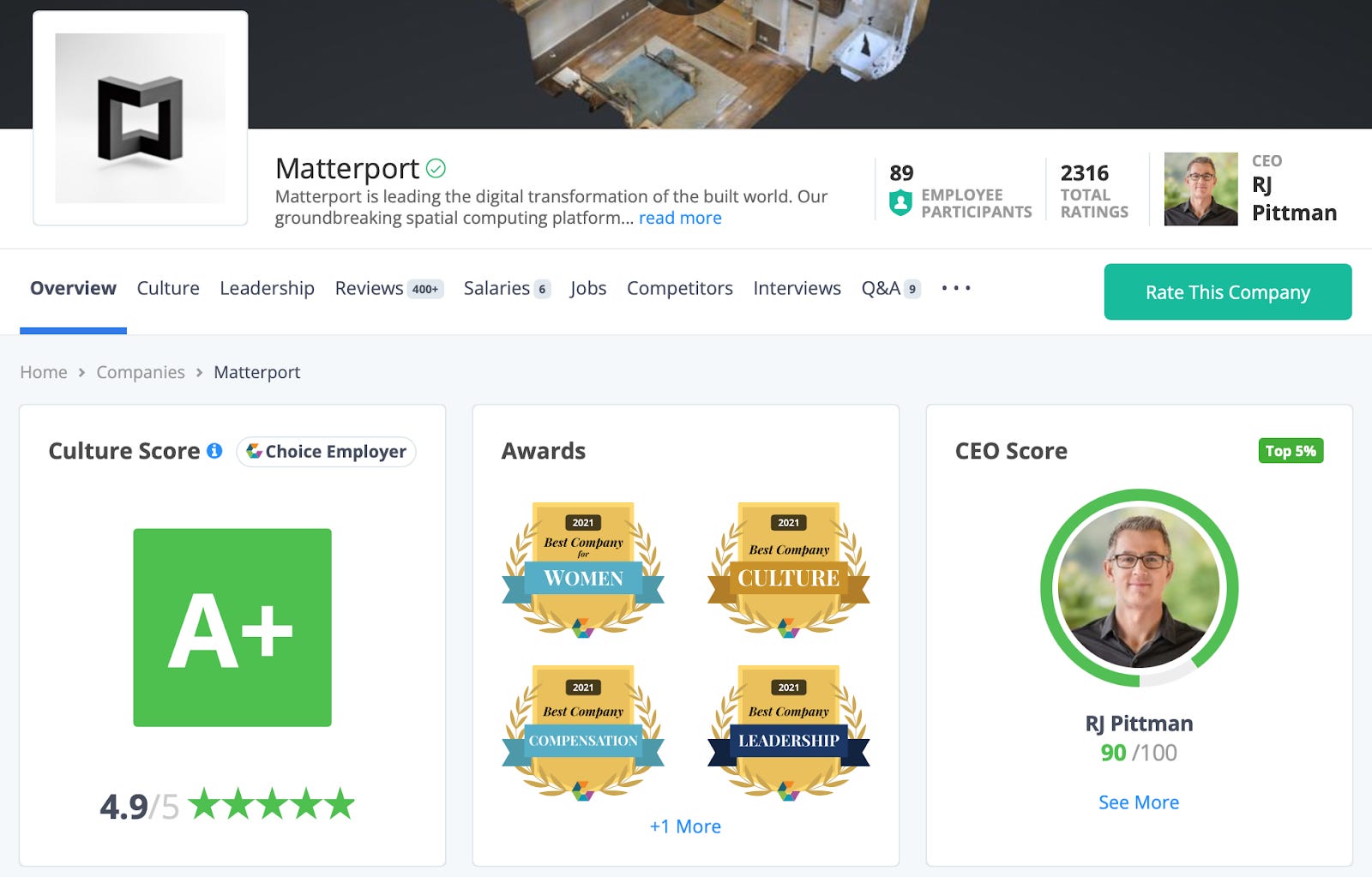

For all of its efforts, Matterport has just recently won two Comparably Awards: Best Company Culture and Best Company For Women. They also won the Best Company Leadership award and were ranked among the top 50 small-to-mid-sized companies with the Best Company Outlook also by Comparably. They were previously named one of the best places to work for LGBTQ by the Human Rights Campaign Foundation.

Indeed, it looks like employees do enjoy working in Matterport and rate the company and the management very high. Though Matterport has a verified page on Glassdoor, a place where I usually check what employees think about the company and management, it seems the company is not that active there. Instead, they are highly engaged on Comparably, the employer-friendly Glassdoor competitor.

The company has an A+ score with a 4.9/5 rating based on over 2300 ratings. 441 Matterport current or former employees reviewed the company, and 96% gave a positive sentiment about the company.

Matterport's CEO, RJ Pittman, has 91 employee ratings and a score of 90/100, placing Matterport in the Top 5% of similar size companies on Comparably with 201-500 Employees and Top 5% of other companies in San Francisco.

And here is what employees say about the company's culture:

Comparably also provides an Employee Net Promoter Score (eNPS) that tracks employees' answers to the question: "On a scale from 0-10, how likely are you to recommend working at Matterport to a friend?" Today, 77% of Matterport employees would encourage their friends to become coworkers, whereas 17% are neutral, and 6% would not recommend working at Matterport to their friends.

Here’s a peek into Matterport’s current hiring trends:

FINANCIALS:

All information below is based on the financial performance of Matterport in the most recent quarter (Q3 2021).

Income Statement:

Revenue:

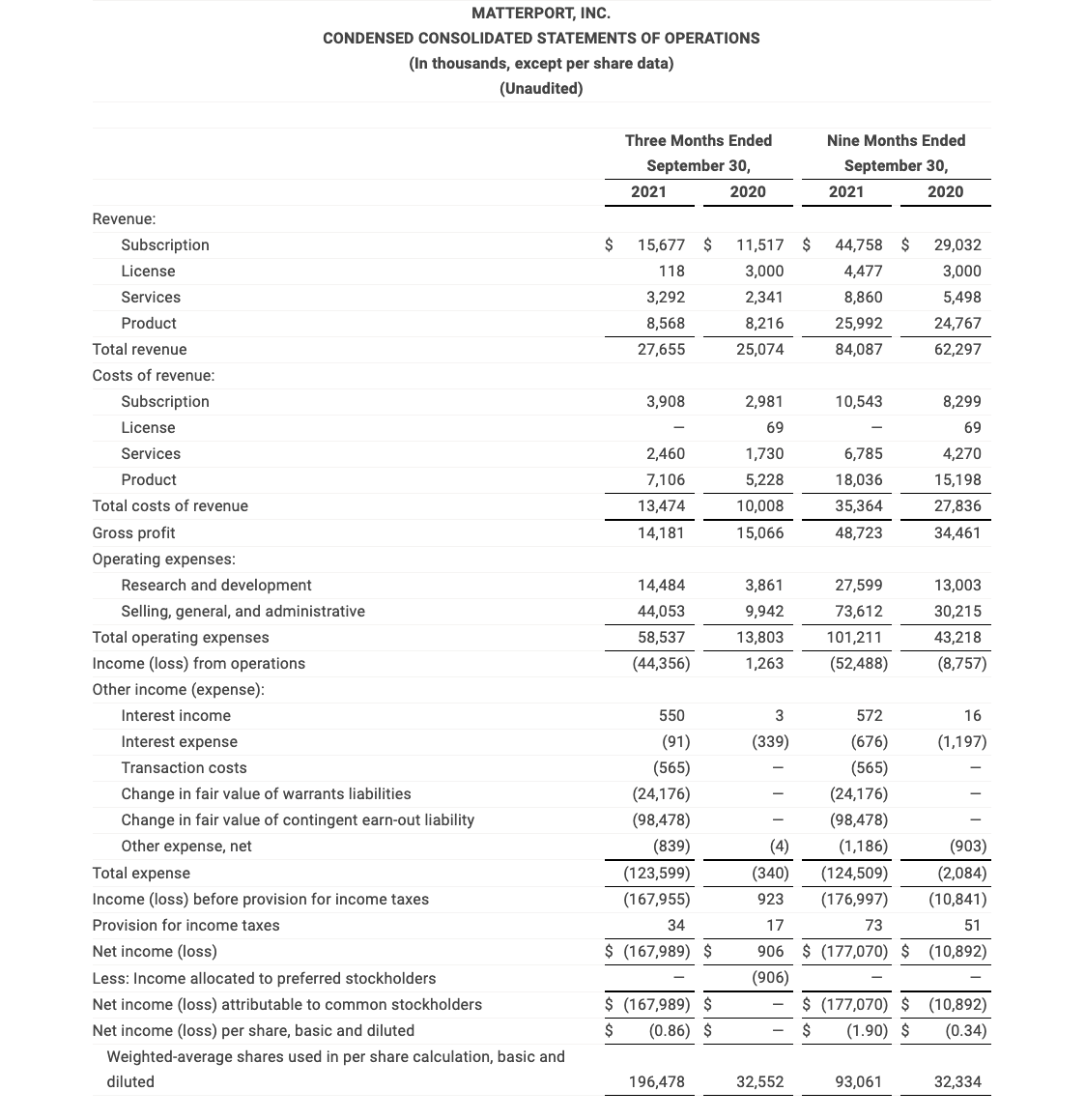

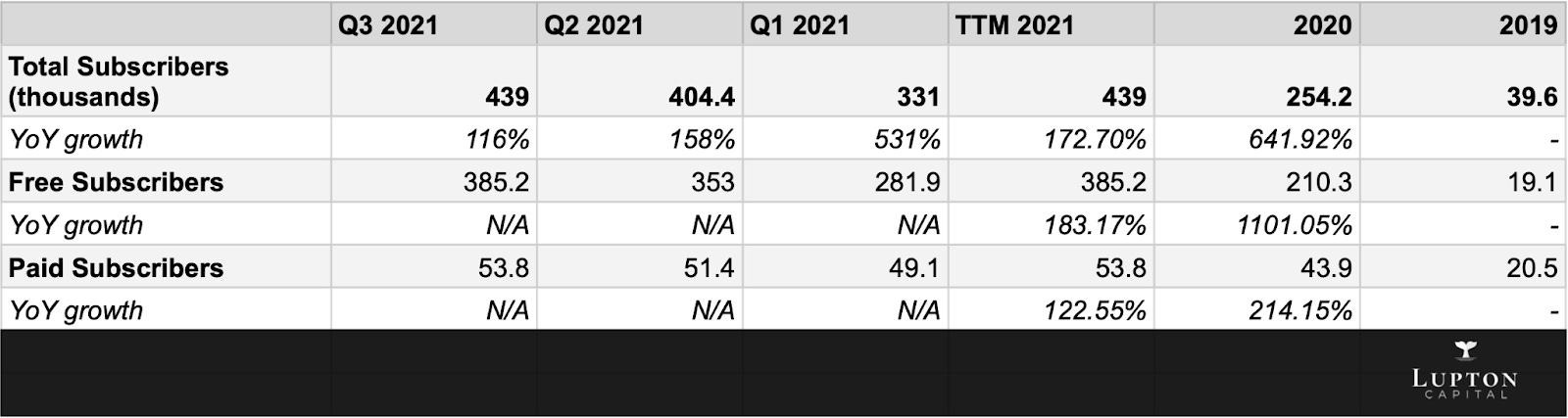

Matterport reported a record third-quarter revenue of $27.7M, but up only 10% YoY. Subscription revenue grew solid 36% YoY to $15.7M and was 57% of total revenue compared to 46% in the year-ago period.

Paid subscribers increased from 40k to 54k, while free subscribers grew an astonishing 216% YoY from 203k to 439k. This growth in paid subscriptions is the result of Matterport's impressive conversion rate of 8% from free to paid users during this quarter.

Services revenue was $3.3M, up 41% YoY. The growth is mainly attributed to additional services, such as schematic floor plans or scan to BIM files, but the company also expanded the availability of capture services, now covering 80 cities in the US and another 25 internationally in the UK, France, Netherlands, Ireland, Canada, and Singapore.

Product revenue was $8.6M, just up 4% YoY. Toward the end of the quarter, the company started to experience impacts from the global supply chain constraints. As a result, they sold out all Pro 2 cameras at the end of the quarter. Without this factor, the management anticipated they could have shipped up to 15% more products (>$1M in revenue).

License revenue was $0.1M compared to $3M last year. License revenue can be very lumpy from quarter-to-quarter depending on the timing of completed transactions and any associated implementation work that company must perform to recognize revenue. As I mentioned before, the license revenue (that is a one-time fee as of now) will be recognized as recurring subscription revenue over the next several quarters.

Gross Margin:

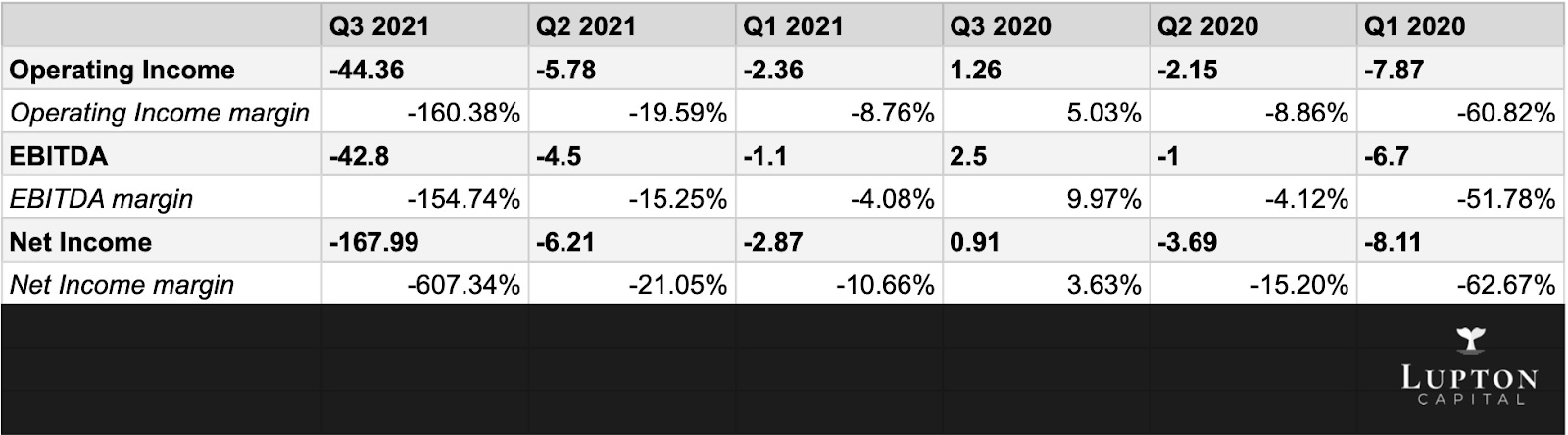

The total gross margin for the third quarter was 51%, a decrease of 15.3% from Q2 2021 (60.4%) and 14.6% from Q3 2020 (60.1%), primarily because of the decline of product gross margin.

Subscription gross margin increased by 2.4% to 77%. Product gross margin was 23% compared to 37% last year, as the company continues to use the Pro 2 camera as an on-ramp for subscriptions by offering discounts, special promotions, and bundles. Services gross margin grew to 33% from 26% in Q3 2020, and license gross margin was 100%.

Costs of Revenue:

Toward the end of the quarter, the company began expediting materials where possible to meet customer demand, which increased the product costs of goods sold. As a result, total costs of goods sold increased by 34% compared to Q3 2020.

Operating Expenses:

Research & development (R&D) expenses were $14.48M compared to $3.86M a year before. It is an increase of 275%. According to the company, such growth in spending is planned and primarily attributable to headcount investments to increase the product development capabilities and throughput.

SG&A (selling, general, and administrative) expenses were $44.05M compared to $9.94M in Q3 2020, representing an increase of 343%. The company continues to aggressively invest in sales and marketing initiatives to drive further growth. They have also added capabilities in the G&A organization as they transitioned to being a public company in the quarter.

Total operating expenses in the quarter were $58.53M compared to $13.8M last year. It is up 324% YoY.

Guidance:

At the time of going public, the company provided guidance for total revenue in 2021 of $120M-$126M. However, in the recent quarter results, they lowered the previous expectations by approximately 15%, and they now expect full-year 2021 total revenue to be in the range of $107M to $110M. It is still up 28% from $86M in 2020.

Balance Sheet:

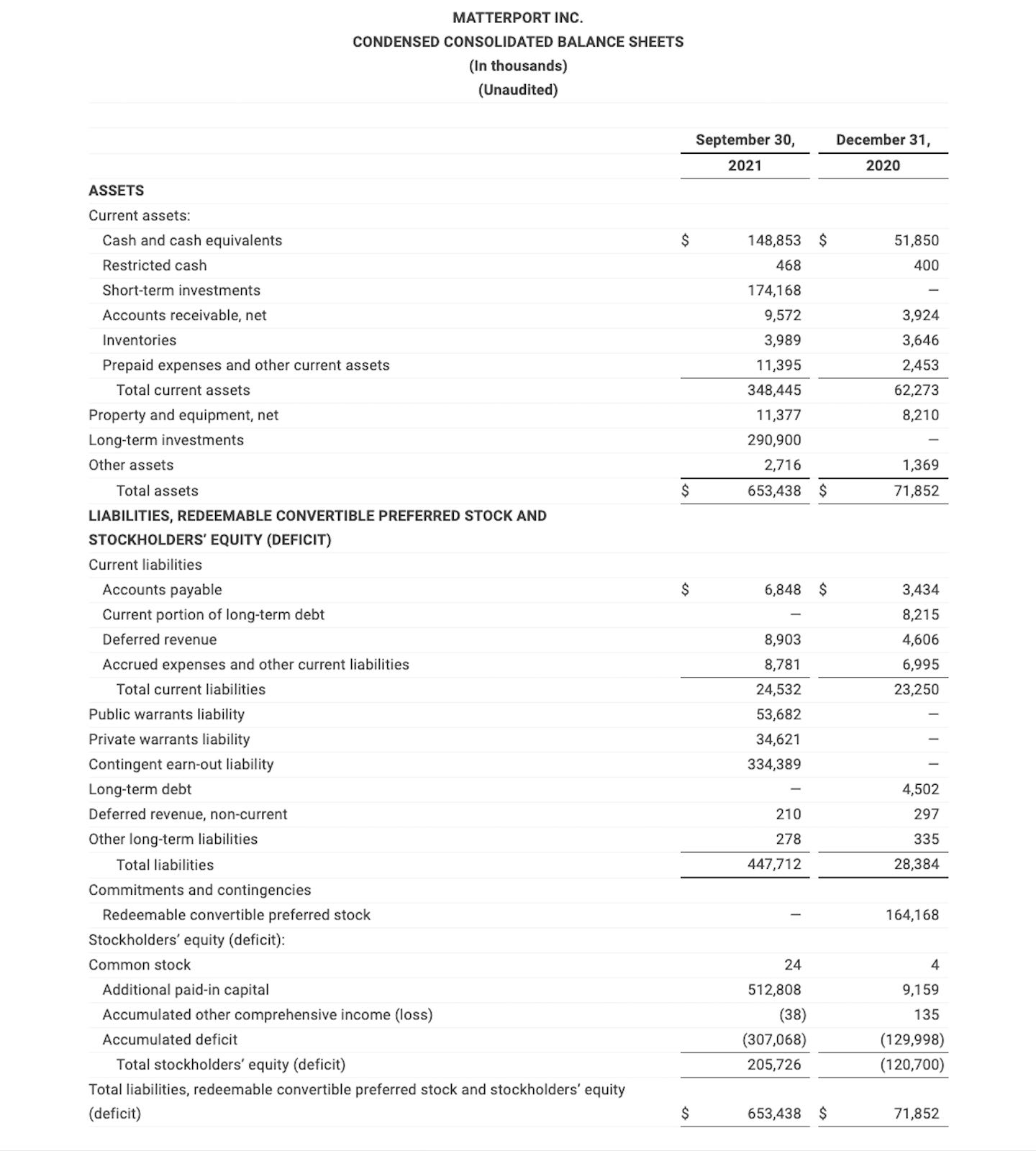

The company has ended the third quarter with $653M on its balance sheet. Most of it comes from short ($174M) and long-term ($290M) investments and cash ($148M).

The company has a very healthy balance sheet with no debt. Such a strong balance sheet will give the company tremendous flexibility to accelerate the growth, both organically and inorganically.

Profitability:

The company reported an operating loss of $44M in Q3 2021, and EBITDA came at a negative $42.8M. Net loss was $167M, primarily because of the expenses incurred with becoming a public company.

Prior to IPO, the company adjusted its cost structure to drive toward profitability, prioritizing it over revenue growth. Now that the company has strengthened the balance sheet and has access to public capital, they switched to rapid growth in light of the market opportunity ahead of them. The company does not plan to be profitable for at least another three years.

Cash Flow:

Cash flow from operations for the first 9 months of 2021 came in at a negative $21M, with a net loss of $177M.

Cash flow from investing for the first 9 months of 2021 came in as an outflow of $473M, mainly attributable to the purchase of investments (investment in marketable and equity securities).

Cash flow from financing for the first 9 months of 2021 came in at $591M as an inflow from proceeds raised through a SPAC sponsor and PIPE investors and partially offset by the full repayment of debt.

Right now, the company burns cash to fuel the growth. As a result, it has a negative free cash flow of $26.8M for the first 9 months of 2021. The company will continue burning cash until at least 2024, when they forecast to ramp up the main phase of its high-growth and turn cash-flow positive.

KEY METRICS:

There are several key metrics to follow to gain a deeper insight into how Matterport performs as a business. These key metrics help the company evaluate its business overall, identify trends affecting it, formulate business plans, and make strategic decisions.

Spaces Under Management:

The number of spaces that have been scanned and filed on the Matterport platform is referred to as spaces under management. The company believes this number is an indicator of market penetration and the growth of the business.

A space can be a single room or entire building or a contiguous scan of a discrete area. It is composed of a collection of imagery and spatial data captured and reconstructed in a dimensionally accurate digital twin of the scanned space.

The company has a solid history of growing the number of spaces under management, as seen in the chart below:

The scale of spaces under management allows the company to directly monetize each space managed for paid subscribers as well as increase the ability to offer new and enhanced services to subscribers, which in turn provides an opportunity to convert subscribers from free subscription plans to paid plans.

Total Subscribers:

A “subscriber” is an individual or entity that has signed up for a Matterport account during the applicable measurement period. The company includes both free and paid subscribers in the total subscriber count.

A “free subscriber” refers to a subscriber that has signed up for a free account and typically scans only one free space allocated to the account. A “paid subscriber” refers to a subscriber that has signed up for one of the paid subscription levels and typically scans at least one space.

The company generally considers a single organization to be a single subscriber if the organization has entered into a discrete enterprise agreement with the company, even if the organization includes multiple divisions, segments, or subsidiaries that utilize the platform.

The company demonstrated strong growth in the number of free and paid subscribers on the platform, as seen in the charts below:

The number of paid subscribers on the platform is an important indicator of future revenue trends, as well as the number of free subscribers because free subscribers may, over time, become paid subscribers.

Net Dollar Expansion:

The ability to retain and grow the subscription revenue generated by existing subscribers is another crucial measure of the business's health and future growth prospects.

The company measures the net dollar expansion rate from the same set of customers across comparable periods and calculates it on a quarterly basis.

The company historically has a reasonable net dollar expansion rate, as seen in the chart below:

However, it can fluctuate from quarter to quarter due to a number of factors, including, but not limited to, the number of subscribers that upgrade or downgrade their subscriptions or a higher or lower churn rate during any given quarter.

It can also be driven by enterprise customers, where the company still has relatively low penetration. But the company is working hard to move enterprise customers upward to higher plans as they grow their usage of Matterport's platform.

Annual Recurring Rate:

With the rapid shift to the subscription revenue model, the annual recurring rate will become an increasingly vital metric for the company going forward.

ARR shows how much recurring revenue the company expects on a yearly basis. Significant growth in this metric would indicate that the company is delivering well on the plan to move to a subscription-mainly business.

Right now, the company is slowly but surely moving the ARR up, as seen in the chart below:

ARR's growth should pick up in 2022 and beyond.

OPTIONALITY:

As I stated earlier, Matterport has a variety of possible applications of its technology and spatial data they haven't touched yet or even discovered.

This opens up endless opportunities for new revenue streams to occur, some of which will be outside of Matterport's core business.

The one, in particular, is the opportunity in metaverse space. If it plays out, it could become as big or even more significant than the company's main part of the business.

And none of these is priced in. That's why I mostly look for companies with optionality, and Matterport fits into this category.

RISKS:

Matterport's growth and financial performance are dependent upon many factors. Below are the most significant:

Penetrating a Largely Undigitized Global Property Market:

The company is highly dependent upon the continued adoption of spatial data and the use of the platform by consumers, which may not occur at the levels the company currently anticipates or at all. The market for spatial data is relatively new, and though the demand for spatial data has grown in recent years, there is no guarantee that such growth will continue. The potential subscribers may not perceive the platform and products as useful.

Adoption by Enterprise Customers:

The company's growth is especially dependent on enterprise customers. Not only more enterprise customers must adopt the use of the platform, but they need to convert to paid subscribers. The company must continue to deliver significant commercial value to enterprise customers in order to make them pay. The company may also spend a lot of resources (both financial and time) to educate the potential customers.

Retention and Expansion of Existing Subscribers:

The company's ability to increase revenue depends heavily on retaining the existing subscribers and expanding their use of the platform. Not only the company needs to succeed in keeping all current customers, but they also need to make these customers switch to higher subscription plans and buy additional services.

International Expansion:

Going to international markets is part of the company's growth plan. Such international expansion efforts require additional investments in product development, sales and marketing. Operating on international markets also poses additional challenges with local laws, taxes, foreign currency exchange risks, staff, etc.

Competition:

The company already faces competition from a number of companies (in each of the vertical markets, as well as from traditional, offline methods of interacting with and managing buildings and their spaces). It expects to face significant competition in the future as the market for spatial data develops.

Investing in Research and Innovation:

The continuous growth requires the company to heavily invest in research and development. The company also must defend its positions and stay competitive. Not only does it require capital, but also hiring and retaining top talent. The company is heavily dependent on highly qualified personnel, and it has struggled to find and hire such for the entire 2021.

VALUATION:

Coming up with a fair valuation for an unprofitable company like Matterport is tricky. There are a few metrics we can use including EV/Revenues and EV/Gross Profit. Another way is to look ahead 3-4 years when the company should be profitable, apply some reasonable multiples then calculate potential CAGR from current prices.

These estimates below could certainly change when $MTTR reports 2021 Q4 earnings and provides 2022 guidance. That’s when the analysts will update their numbers. For the following calculations we’re going to use $MTTR’s current EV (enterprise value) of $1.8 billion.

$MTTR is currently trading at 16.5x 2021 EV/Revenues

$MTTR is currently trading at 11.2x 2022 EV/Revenues

$MTTR is currently trading at 28x 2021 EV/GP

$MTTR is currently trading at 18.7x 2022 EV/GP

I think these multiples are very fair for a company that is expected to grow revenues by 4x over the next few years but it’s the lack of profits that have investors concerned plus there’s no guarantee these growth estimates pan out.

If you look at Matterport’s EV/GP over the last 6 months you’ll see how far it’s come down. Obviously it was ridiculous that $MTTR was trading at 129x LTM EV/GP in early December but now that number has plummeted to 31.5x for trailing 12 months and 18.7x for next 12 months — this makes the stock look way more attractive at current prices and multiples.

Here are my BEAR, BASE and BULL case scenarios for Matterport.

For the BEAR case I used 30% revenue growth and 10% net income margins.

For the BASE case I used 40% revenue growth and 20% net income margins.

For the BULL case I used 50% revenue growth and 30% net income margins.

Obviously there are a hundred different ways to play around with these numbers but at least this gives us somewhere to start. It’s also hard to estimate what an appropriate P/E multiple might be in 2025 but it would most likely be tied to the earnings growth rates in those scenarios.

TECHNICALS:

I’ll be honest, the technicals are nothing short of disgusting but that’s not a surprise when you’re looking at stock that is down 75% from the highs and trading just above the all time lows.

I’m not interested in $MTTR because of the technicals because right now they are garbage, I’m interested in $MTTR because of the massive “digital twin” database they are building that could and should be monetized in the years to come.

The only thing I’d say about this chart with regards to risk management is this… if you decide to get into $MTTR before they report Q4 earnings, you might want to consider setting your stop loss just below the current 52-week low which is $7.50 — this way if the stock takes another nosedive you can get out with a small loss then wait for a better entry point.

SHAREHOLDERS:

Matterport's ownership breakdown as of Q3 2021:

From a shareholder standpoint $MTTR is unlike most other companies I have covered. Perhaps it’s because they were a SPAC with heavy retail interest from the start but it’s very unusual to see the “general public” owning 2/3 of a company like this. I don’t think this is necessarily a bad thing, however if $MTTR is going to move higher it will be more support from institutional investors ie big funds, hedge funds, etc.

R.J. Pittman (CEO) owns approximately 4% of the company, while other executives together hold just a little bit above 1%. The two largest VC/PE investors (Lux Capital and DCM Ventures) hold around 15% of the company and they will likely be sellers over the next 12-24 months.

Alec Gores, a SPAC sponsor who brought Matterport public, has a 4.7% share of the company — I have no idea what his timeframe for holding might be. If he owns these shares personally then he might be a longer term holder than the VC’s mentioned above which need to eventually get out so they can return that capital to their LPs.

Institutional investors, among which are Tiger Global Management, Vanguard Group, Morgan Stanley Investment Management and others, hold approximately 15% of Matterport.

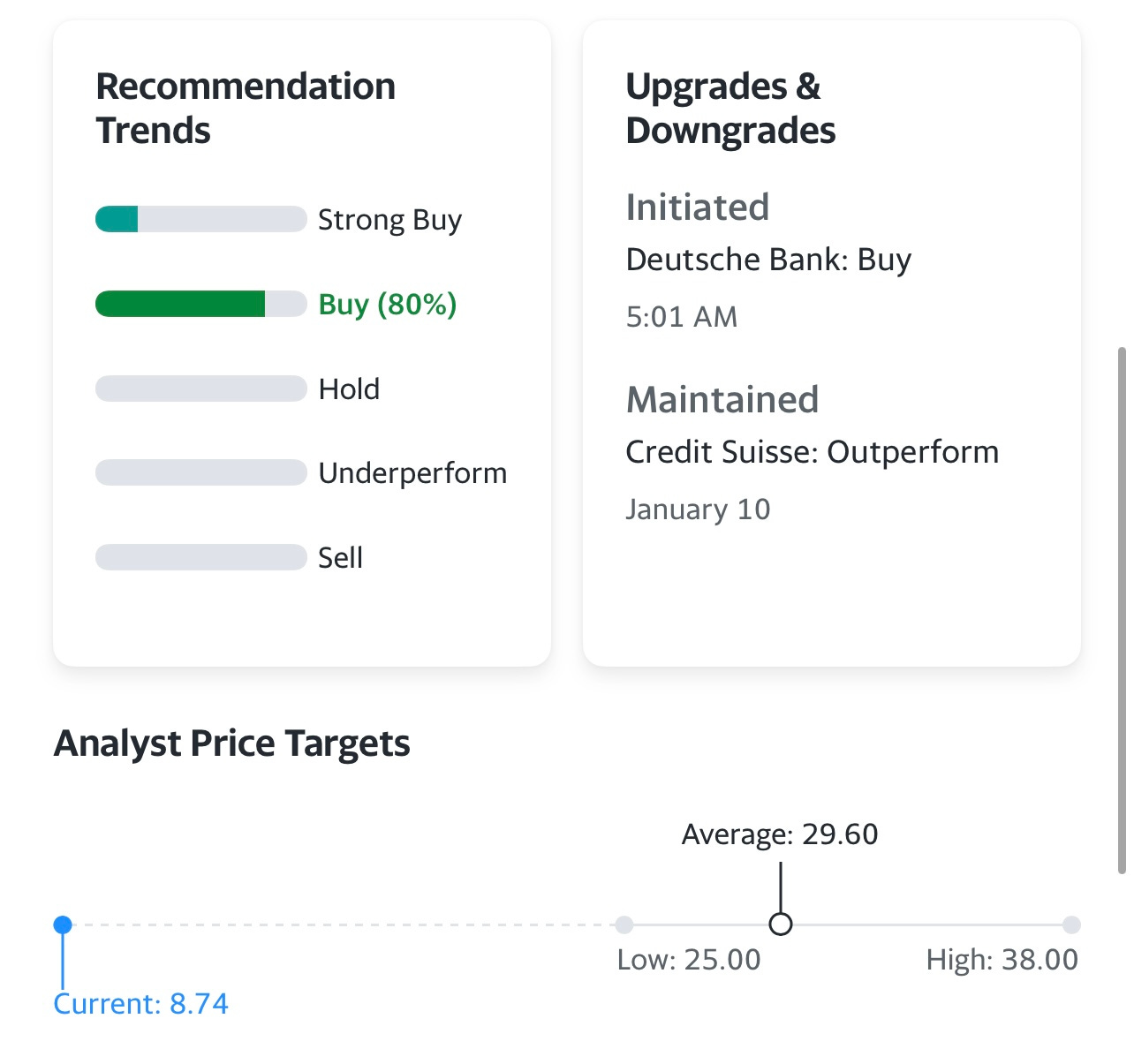

ANALYSTS:

As a freshly IPO’d company that also went public in a non-traditional way (via SPAC merger), there are only 5 analysts covering Matterport right now. The consensus among these analysts is a BUY rating with an average price target of $29.60 — once again these ratings and price targets will likely change after $MTTR reports Q4 earnings. That’s when analysts like to update their numbers and ratings.

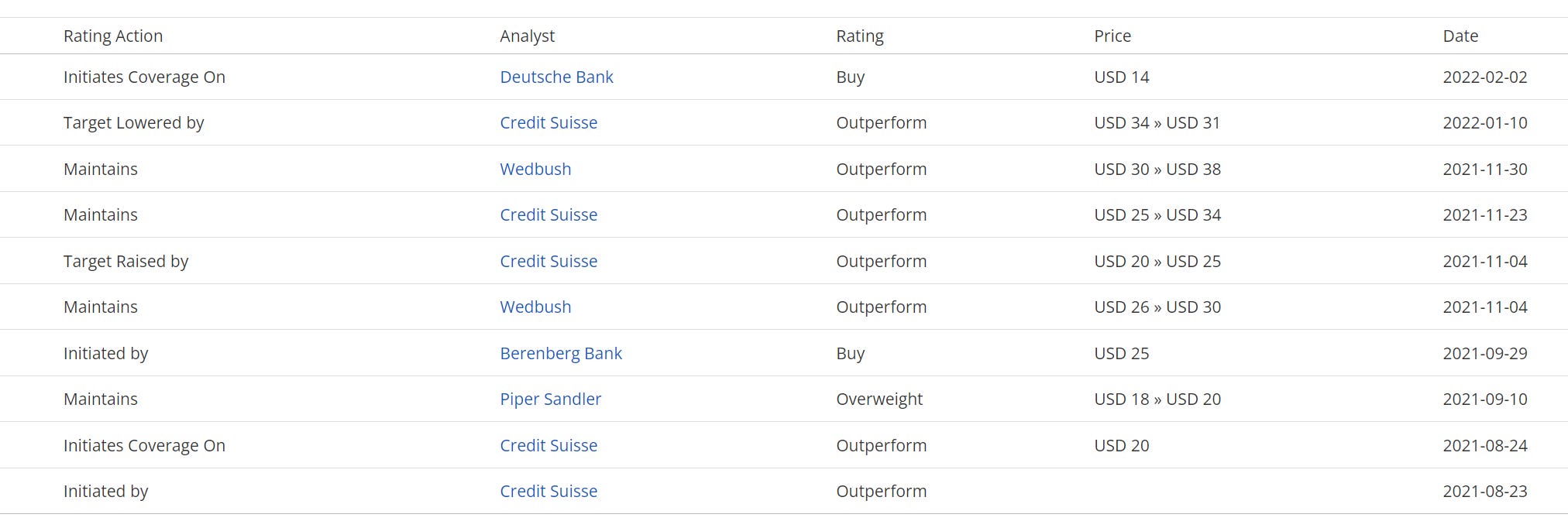

You can see down below the most recent update is from Deutsche Bank with a BUY rating and $14 price target. Regardless of what $MTTR says in their next quarterly report, these analysts have seen the stock fall 75% in the last 2 months and there’s no doubt that most of them will cut their PT’s to $15-25 while keeping the BUY ratings. This is just what they do — they are price chasers to the upside and the downside.

Here is what one of the analysts, Daniel Ives from Wedbush, who covers the company, said about Matterport: "Matterport is in the early innings of a massive growth story playing out over the coming years. Based on our conversations with investors over the past few months, we believe this tech story remains 'under the radar' among growth investors. The company's free-to-paid conversion model and further penetration of the real estate vertical remain near-term keys to a "stepped-up" growth story. Penetration on the retail verticals remains very untapped. Nonetheless, this is a highly speculative story stock."

CONCLUSION:

Matterport is in the early innings of it’s growth story. It is not clear yet if this is a hyper-growth story and great margins or a story with mediocre growth and average margins — the opportunity is definitely there but the company needs time to execute. If you are not a patient investor then I’d suggest staying away from $MTTR.

There are certainly many things to like about Matterport and I tried to cover most of them in this writeup. Matterport is still a young company with lots of prove. The company will probably look very different in several years. For example, I think mobile devices will become the primary way to capture the spaces as the cameras on devices will significantly advance (LiDAR, 360), which in turn will reduce the need for in-house cameras. The hardware business is low-margin anyway (just like Peloton). The success of these types of companies is their data and their recurring revenue model ie subscriptions.

Like I stated above, I still think there is room for the stock price to go lower depending on their Q4 results, their 2022 guidance, the macro data and of course the overall markets. $MTTR is still considered a high-multiple growth stock so anymore pain in this area of the market will certainly affect Matterport too.

I would never buy a stock based on the hope that it gets acquired but it’s certainly possible that a company like $FB (Facebook) or $ADSK (Autodesk) or $ADBE (Adobe) or $GOOG (Google) or $AAPL (Apple) or $MSFT (Microsoft) could buy Matterport without any anti-trust issues. This is pure speculation and please don’t buy the stock hoping for this kind of outcome.

Finally… We like to say that data is the next oil, well, Matterport is building one of the most unique “data-bases” in the world.

I hope you enjoyed this writeup on Matterport, if you have any questions, thoughts or comments please feel free to reach out.

Regards,

Jonah Lupton

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.