In addition to my Substack newsletter, I also run a Stocktwits room where I post my current holdings, buys & sells, investment models, technical analysis and market commentary for both my Investment Portfolio (long term, strong fundamentals, 20-30 holdings) and my Trading Portfolio (short term, strong technicals, 0-10 holdings). The two options are $15/month for the monthly plan [click here] or $150/year for the annual plan [click here].

You can now signup for my new Substack called Jonah’s Trading Charts which is focused exclusively on the technicals — every day (usually pre-market) I’ll send out an email with my favorite trading charts/setups. You’ll also have access to my trading portfolio with current positions/sizes, entry/exit prices, profits/losses and much more. I’m also doing live charting and live trading 3-4 times per week.

Nu Holdings Ltd (NU) is one of the WORLD’S largest digital banking platforms with 70M customers and they are just getting started.

Massive TAM within LatAm outside of main Brazil operations.

NU has proven their compounding effects of increasing active customers (75% YoY) and their respective average revenue per customer (105% YoY), which is translating into sky-high revenue growth of 230% YoY to $1.2B.

Warren Buffett ($BRK) has invested $1B to date.

Opportunities outweigh the risks = asymmetric risk-reward.

THE NUMBERS:

Current stock price: $4.40

52 week high: $12.24

52 week low: $3.26

Shares outstanding: 4.676 billion

Current market cap: $20.58 billion

2021 revenues: $1.7 billion (actual)

2022 revenues: $4.2 billion (estimated)

2023 revenues: $6.0 billion (estimated)

INVESTMENT THESIS: A Compounding Ecosystem

Founded in May 2013 and IPO’d in Dec 2021 (at $9/share), NU is a founder-led digital banking platform with over 70M customers as of September 26, 2022 across Brazil (66.4M), Mexico (3.2M), and Colombia (0.4M). NU leverages technologies and innovative business practices to create new financial solutions and experiences for individuals and SMEs that are simple, intuitive, convenient, low-cost, empowering, and human. NU’s mission is “fostering access to financial services across Latin America”.

NU is capitalizing on the underbanked population of LatAm while maintaining a high Net Promoter Score (NPS) of around 90. They have already provided over 5M people with their FIRST bank account or credit card

(Source: Nubank Q2 Earnings)

COMPETITIVE ADVANTAGES:

NU is well positioned to capitalize on major secular tailwinds and demographic trends of digitization that we are seeing among the younger generation in emerging markets.

The network effect of being the #1 card issuer in all 3 countries gives them cross-selling opportunities to their now multi-product platform. The two newer countries (Mexico & Colombia) to NU are in their infancy and have higher growth rates than Brazil did in its early stage.

(Source: Nubank Q2 Earnings)

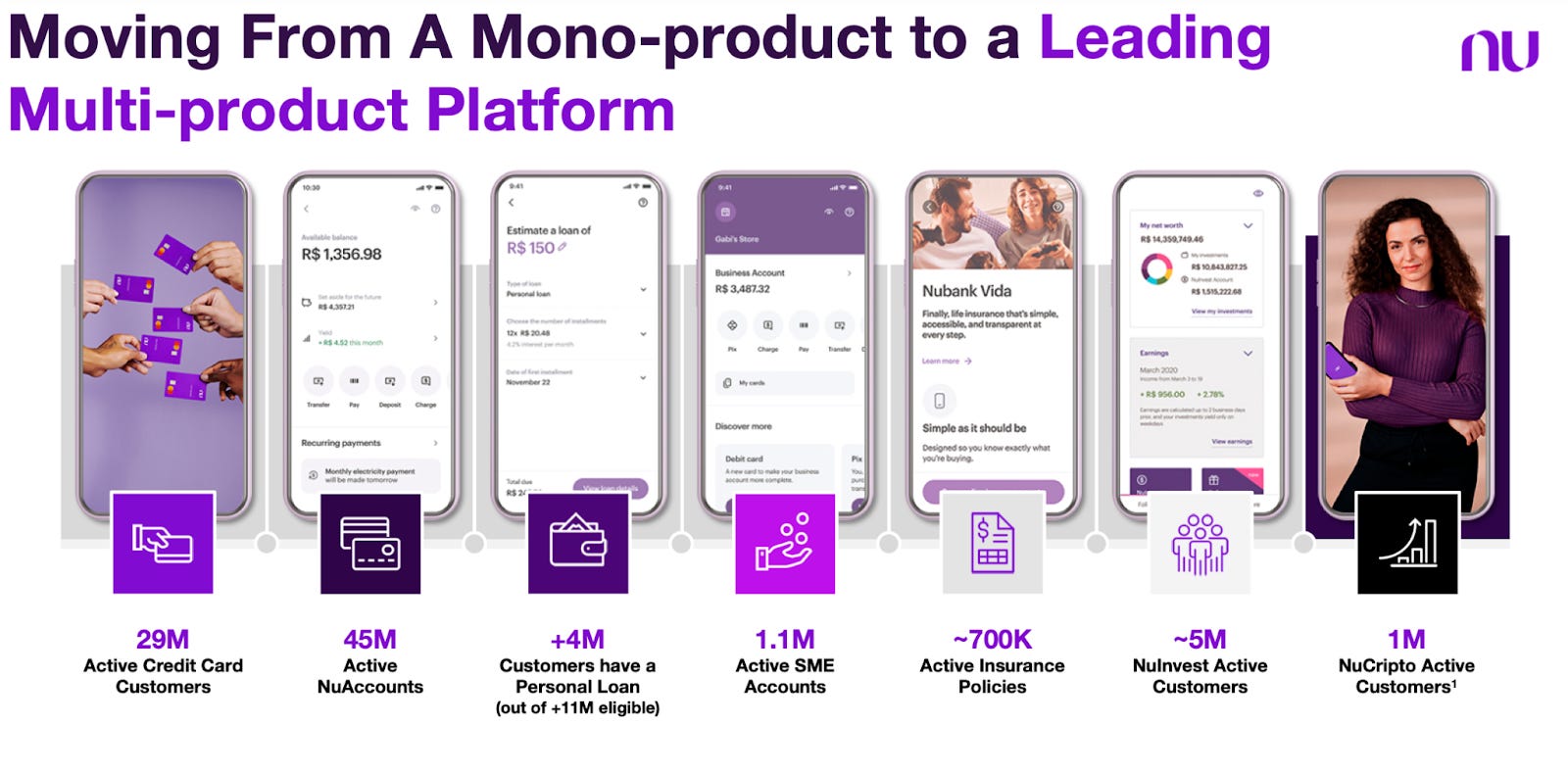

NU is increasingly moving from single-product platform to multi-product platform and capturing not only individuals, but SMEs as customers too (2M already!). This enhances their ecosystem offering and essentially “builds a fence” around their customers for long-term retention.

(Source: Nubank Q2’22 Earnings)

FINANCIAL METRICS & GROWTH:

Formula for Success: Their core focus/formula is one of their most significant strengths because they are very engrossed in enhancing the below 3 metrics. It’s evident that they have capitalized on this thus far, but they are still early in their growth trajectory.

(Source: Nubank Q2’22 Earnings)

Compounding Effect = Higher ARPAC: NU’s ability to cross-sell to their customer base has been steadily improving and much quicker than previous quarters. The average number of products per client is now 3.7. This effect is an obvious trust builder between customers and NU as more customers (55%) are using NU as their primary bank account. I expect this to continue as new products get released and enhanced, which ultimately makes their customer’s financial lives easier (and cheaper!).

(Source: Nubank Q2’22 Earnings)

Revenue Growth: Nothing short of impressive especially given the global macro headwinds and the additional LatAm/Brazil exogenous factors. Revenue grew 230% YoY (FX-neutral basis) to $1.2B in Q2’22 - yes, that is NOT a typo. In addition, the ARPAC increased 105% YoY to $7.80/month. $7.80 may not seem significant, but when combined with a $0.80/month “cost to serve” then you get a lean and high margin business primed for operating leverage.

Although I don’t expect NU to continue growing at 230%, I wouldn’t be surprised at continued triple-digit growth in the short-term. NU is also showing sneak-peeks of profitability in their higher penetrated market, Brazil (36% capture of total adult population).

Profitability: Brazil region had net income of $13M in the first half of 2022 for the first time ever. NU has overall profitability in its sights, but will balance it with growth/expansion by being the lowest cost operating platform in the industry as noted by the CEO:

VALUATION:

While valuing hyper-growth companies is proven difficult due to not being optimized for income yet, we can still look to the Price/Sales ratio for some insights.

(Source: TIKR Terminal)

The NTM P/S is currently at 3.61x, whereas the average since IPO has been 11.08x.

While traditional valuation metrics don’t provide much substance, it is often far more constructive to evaluate hyper-growth businesses based on their business progress/metrics and KPIs like we have done above for NU. Therefore, I place little weight on valuation ratios, but we can conclude that we have seen significant multiple contraction since IPO.

RISKS:

Macroeconomic Factors

Lots of economic uncertainty is present with the main headlines of recession and inflation. In addition to the global headwinds, there are region specific risks to Brazil such as high inflation, currency devaluation, Presidential election which could contribute to a country-wide downturn in the economy. If this materializes further it could impact customer spending habits, credit demand, payment volumes, and loss of trust in the financial system of Brazil.

Competition

There are many VC dollars flowing into LatAm fintech in recent years ($4.1B in 2020 to $15.7B in 2021 according to LAVCA), therefore competition is bound to become more fierce. This is relatively mitigated by their first-mover advantage, but needs to be monitored going forward to ensure NU remains a category leader.

CONCLUSION:

It’s undeniable that LatAm is a massive fintech opportunity poised to decrease the unbanked population and provide better/cheaper access to financial products. I believe NU is at the forefront of this digitization and destined to capitalize on these geographic and consumer trends while expanding their product offering.

(Source: Nubank Q1’22 Earnings)

Given the significant pullback in the stock following the $9.00 IPO in Dec 2021, I believe the current price of around $4.40 presents a strong case for upside over the next 12 months and more importantly, larger potential upside over the next 3-5 years given their strong acceleration in business metrics and hyper-growth in new countries. As NU becomes profitable we could see triple digit GAAP EPS and non-GAAP EPS growth over the next few years leading to multiple expansion and strong stock performance.

Looking at the technicals, NU bounced off the 100d SMA on Friday which looks like the only support unless you count the volume shelf. If NU can’t hold the 100d SMA then I don’t like the risk/reward in the short term however if you’re a long term investor your best strategy might be to average down into your ideal position size.

Disclosure: I do not own shares of NU but it’s on my watchlist and I may start a position at some point in the near future

It’s very possible that a longer writeup on NU could be coming in the next couple months, perhaps after they report Q3 earnings.

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.

Jonah’s Growth Stocks is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.