Part 1: Deep dive on Albemarle ($ALB)

In addition to my Substack newsletters, I also run a Stocktwits room where I post my current holdings, daily activity, investment models, technical analysis, live charting, live trading and market/macro commentary for both my Investment Portfolio (long term, strong fundamentals, 20-30 holdings) and my Trading Portfolio (short term, strong technicals, 10-20 holdings). The two options are $15/month for the monthly plan [click here] or $150/year for the annual plan [click here]. Prices will be increasing on February 15th.

Several weeks ago I launch Trading Charts which is focused exclusively on my trading portfolio. Every morning I send out an email with my 10-20 of favorite trading charts/setups for the day. You’ll also have access to my current trading portfolio with current positions/sizes and entry/exit prices. I also do live charting/trading sessions everyday with a market/portfolio recap at 4pm. Prices will be increasing on February 15th.

Company: Albemarle Corporation

Ticker: (ALB)

Website: Albemarle.com [click here]

IPO date: February 22, 1994

IPO price: $7.25

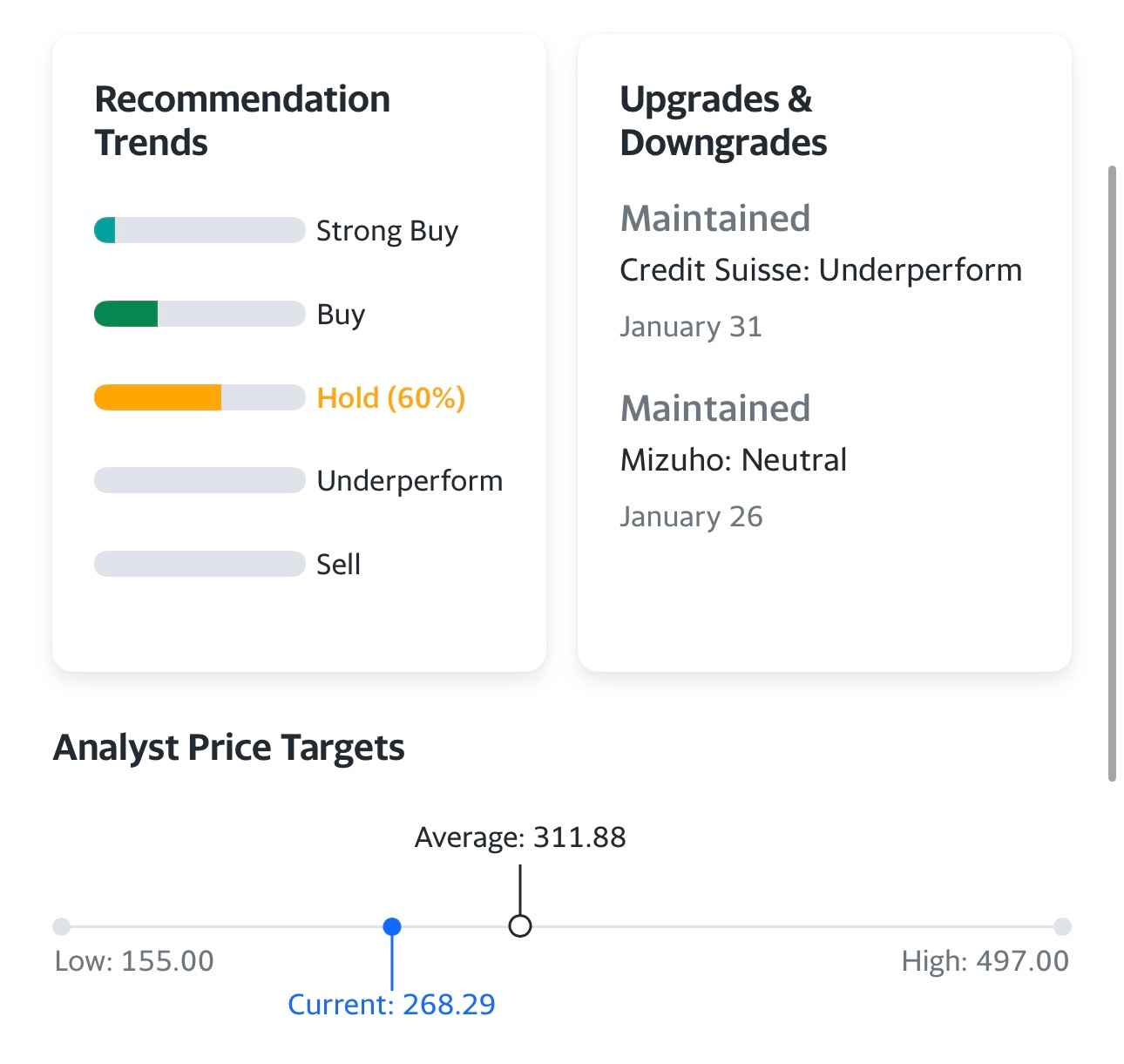

Current stock price: $268.29

Outstanding shares: 117.8 million shares

52 week high: $334.55 on November 11, 2022

52 week low: $169.93 on February 24, 2022

ATH: $324.85 on November 11, 2022

Market cap: $31.6 billion

Net cash/debt: +$2.35 billion (debt)

Enterprise value: $33.9 billion

Headquarters: Charlotte, North Carolina, United States

Number of employees: 6,000+

Average price target from analysts: $311.88

Next earnings date (Q4 2022) is Wednesday, February 15th

Investor Relations [click here]

Investor Day 2023:

Q3 2022 Earnings Report [click here]

Q3 2022 Earnings Presentation [click here]

Q3 2022 Earnings Call Transcript [click here]

Outline

Introduction [part 1]

Company Background [part 1]

Opportunity [part 1]

Products / Customers [part 1]

Business Model [part 1]

Competitive Advantages [part 1]

Management [part 2]

Culture [part 2]

Financials [part 2]

Risks [part 2]

Ownership [part 2]

Valuation [part 2]

Investment Model [part 2]

Analysts [part 2]

Technicals [part 2]

Conclusion [part 2]

Part 2 of the ALB writeup should be out tomorrow (Feb 12th) or Monday (Feb 13th).

Introduction

Disclosure: I currently have a 4.25% position in ALB

I’ve had a position in ALB for 12 months but I’ve never been more bullish on the company than I am today because of their recent strategic business update [click here] where they not only provided preliminary 2022 Q4 earnings but gave guidance for 2023 through 2027.

For 2023 they are forecasting $11.3 billion to $12.9 billion of revenues, if we use the midpoint that would be 65% revenue growth over 2022 revenues assuming they report $7.32 billion which was the midpoint for preliminary 2022 revenue guidance they announced a couple weeks ago. They report earnings this coming week so we’ll know the exact numbers soon enough.

If we look at EPS (earnings per share), they are expected to report $21.65 to $22.05 for 2022 but then said 2023 EPS will be $26 to 33 per share. If we use the midpoints for both it means EPS in 2023 will increase 35% YoY.

EPS growth this year isn’t expected to be as impressive as the revenue growth because of margin contractions however ALB is only trading at 9.25x 2023 earnings (using the midpoint) which is extremely cheap for a company growing EPS by 35% (or more).

To be fair, nobody expects ALB to continue growing revenues and earnings at these rates but this is an extremely profitable company that will continue to benefit from the tailwinds of the EV industry which has created enormous demand for lithium which is the majority of ALB’s current business.

Sticking with forward guidance, ALB is forecasting $17.6 billion to $19.3 billion of revenues by 2027 along with $7.2 billion to $8.4 billion of EBITDA and $6.6 billion to $7.1 billion of operating cash flow. If we use the midpoint of their 2023 guidance ($12.1 billion) then revenues would need to increase at an average annual rate of 11% in order to hit the midpoint of their 2027 guidance.

If we assume margins stay relatively flat over the next several years then EPS growth should also be in the low double digits. If we include the growth expected this year, ALB should be trading with a forward P/E in the mid teens (14-16x) not 9x, especially when we consider all the cash/profits they’ll be generating over the next few years which can be used for stock buybacks, dividend increases or more E&P (exploration & production).

Based on my estimates ALB could generate $25 billion of profits (net income) between 2023 and 2027 which is quite impressive considering the current enterprise value is just under $34 billion. Based on their EBITDA guidance through 2027, they’re expecting EBITDA margins to stay in the low-40% range so there’s no reason to think that net income margins can’t stay in the low -30% range.

In addition to the strong fundamentals (growth + earnings) and compelling valuation, the other main reason I like ALB is because of what I mentioned earlier which is lithium demand coming from the EV industry. We all know that Tesla is the current leader when it comes to EVs (electric vehicles) but we also know they are going to face increasing competition going forward from Ford, General Motors, Toyota, Audi, Volkswagen, Porsche, Mercedes, BMW and so on. Even if we assume that Tesla will remain the leader it’s impossible to guess who will be the other top players. The fact is that all of them will be increasing volumes as the world continues to move to EVs whereas it’s probably 5% of all volumes right now but could be 30-40% of all volumes by 2030. A more competitive industry might be bad for the individual auto companies but it’s good for companies like ALB that supply the raw materials needed to power the batteries in EVs.

Since ALB gave their strategic business update a couple weeks ago we’ve seen most of the analysts increase their 2023 estimates and price targets however if you look at the current estimates for 2026 (btw, 2027 is not available yet) they are nowhere near where ALB is guiding to which means the analysts aren’t convinced yet that ALB can hit those numbers or they’re just way behind the ball and will have to play catchup.

In my opinion if EV adoption across the planet stays strong over the next 5 years it will be very hard for ALB to disappoint shareholders because the biggest risk for ALB is lithium prices dropping by a substantial amount but I just don’t see that happening if demand for EVs remains strong and it should with many US states and countries planning to ban the sale of ICE (internal combustion engine) vehicles after 2030.

In part 2 of this writeup which should be out tomorrow or Monday I’ll go into more detail on why I like ALB but for now I think it’s one of the most undervalued stocks I’ve found in quite some time. Not too many companies growing revenues by 65% and earnings by 35% while only trading at 9x earnings. We talk about lots of large cap stocks trading at PEG ratios above 1.0 with some trading at PEG ratios above 2.0 or even 3.0 yet ALB is trading at a forward PEG ratio of .25x which is unheard of. Unless there’s a complete collapse in lithium prices, it’s hard to come up with a legitimate bear case for ALB what would case the stock to underperform the major indexes and personally I think there’s a decent chance that ALB is one of my top portfolio performers over the next 12-18 months.

Hope you enjoy this writeup and feel free to share your thoughts with me after you’ve had a chance to read part 1 and part 2.