Part 2: Deep dive on Mobileye ($MBLY)

In addition to my Substack newsletter, I also run a Stocktwits room where I post my current holdings, buys & sells, investment models, technical analysis and market commentary for both my Investment Portfolio (long term, strong fundamentals, 20-30 holdings) and my Trading Portfolio (short term, strong technicals, 0-10 holdings). The two options are $15/month for the monthly plan [click here] or $150/year for the annual plan [click here].

You can now signup for my new Substack called Jonah’s Trading Charts which is focused exclusively on the technicals — every day (usually pre-market) I’ll send out an email with my favorite trading charts/setups. You’ll also have access to my trading portfolio with current positions/sizes, entry/exit prices, profits/losses and much more. I’m also doing live charting and live trading 3-4 times per week.

I’ve also relaunched my podcast Investing with the Whales (interviews with CEOs) — you can subscribe on YouTube, Spotify, Apple Podcasts and Google Podcasts.

Here is part 2 of the Mobileye deep dive writeup, to be honest I’m not sure how I feel about splitting up these writeups into 2 parts, feel free to share your feedback with me. Personally I think it just flows much better as one long writeup.

Company: Mobileye

Ticker: (MBLY)

Website: Mobileye.com

IPO date: October 26, 2022

IPO price: $21.00

Current stock price: $31.62

Outstanding shares: 801.9 million

52 week high: $37.31 on December 14, 2022

52 week low: $24.85 on November 03, 2022

Market cap: $25.4 billion

Enterprise value: $24.5 billion

Headquarters: Jerusalem, Israel

Number of employees: 3,900+

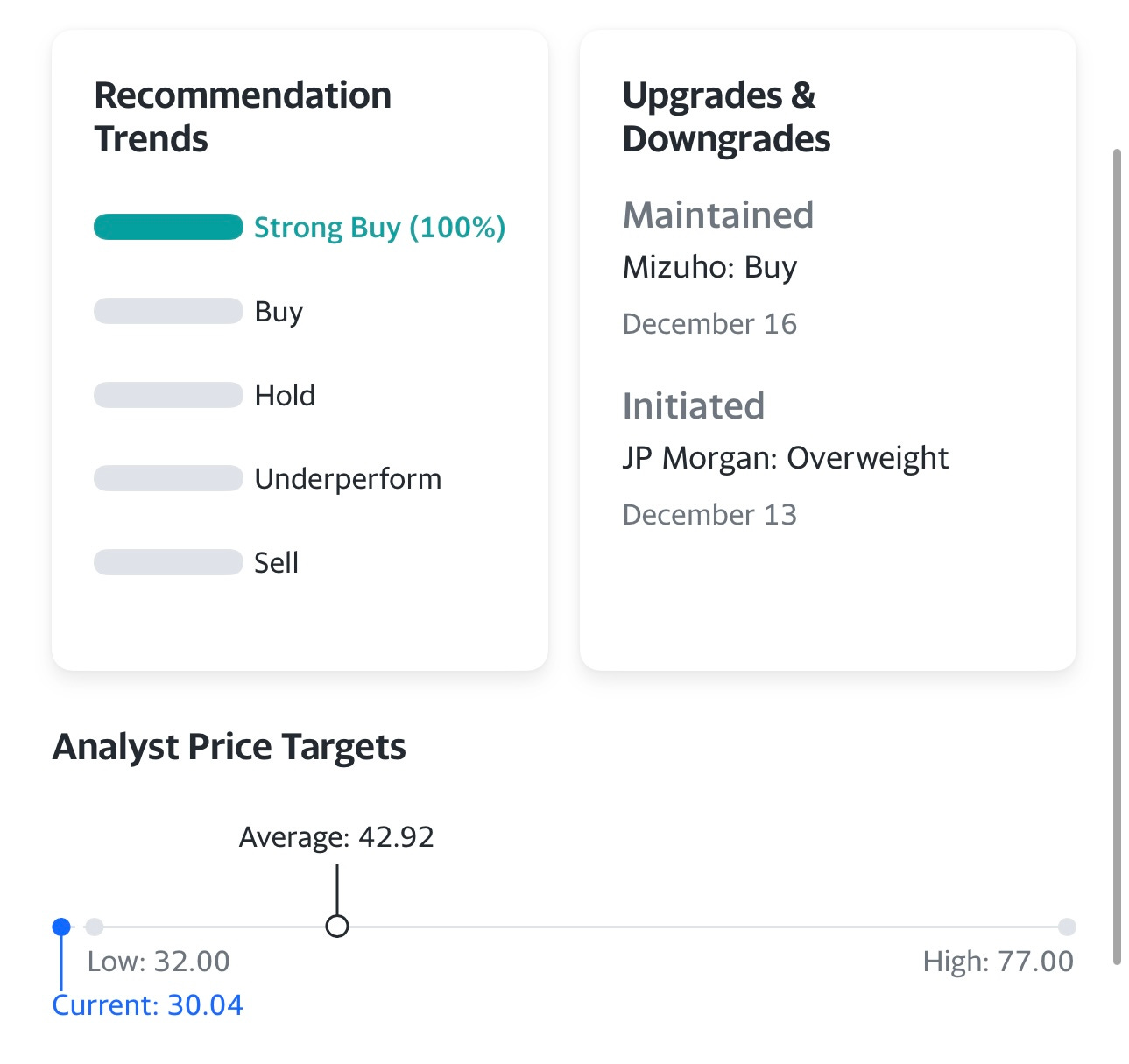

Average price target from analysts: $42.92

Investor Relations [click here]

Q3 2022 Earnings Report [click here]

CES 2022 [click here]

Outline

**Part 2 should be out in the next couple days

Introduction

Company Background — was in part 1

Opportunity — was in part 1

Technology — was in part 1

Business Model — was in part 1

Customers — was in part 1

Competitive Advantages — was in part 1

Management — was in part 1

Culture — was in part 1

Financials — was in part 1

Risks — was in part 1

Ownership — was in part 1

Valuation

Investment Model

Analysts

Technicals

Conclusion

Introduction

**Disclosure: I do not have a position in Mobileye (MBLY)

I remember looking into Mobileye (MBLY) back in 2014 or 2015, after their first IPO but then I stopped following the company when they got acquired by Intel in 2017 for $15.3 billion. Since I wasn’t interested in owning Intel (INTC) it made little sense for me to stay up-to-date on what MBLY was doing but now that INTC has spun them off into a new publicly traded company I felt it would be valuable for my subscribers if we did a deep dive on the company especially since I haven’t really seen anyone else talking about MBLY.

Last year (2022) was a historically bad year for IPOs (that’s what happens in a bear market) and when INTC first floated the idea of taking MBLY public the valuation was rumored to be in the $50+ billion range so now I’m even more interested in the company knowing the shares might already be trading at a discount to their fair value.

MBLY has strong fundamentals (38% YoY growth in Q3) and they’re already profitable (non-GAAP) with 70-75% gross margins and 30-35% EBITDA margins. I like that revenue growth is expected to accelerate in the next few years with some analysts looking for 40-50% YoY growth in 2025 and 2026. There aren’t too many $25 billion public companies still growing at 38% with the potential for even higher growth rates in 3-4 years (although 2023 might be a slower growth year compared to 2024-2026).

It’s pretty rare to see a mature company begin to accelerate their revenues but this can happen when they’re able to develop and launch new technologies which is the case with MBLY.

If MBLY is able to hit those high expectations (in 2026) not only will the stock trade at a nice premium to the rest of the market (because they’ll be growing much faster than the average tech stock) but the stock price will be much higher.

At least one analyst is already suggesting MBLY could be trading at $300 per share in the next 7 years which is almost 10x higher from here. I’m certainly not ready to go there yet because that would make MBLY at $250 billion company but overall the analyst community is very bullish on this company with 70% of them having a buy/overweight rating.

MBLY is the Godfather of driver assist technology (ADAS = advanced driver assist systems), currently in 120+ million cars around the world including hundreds of car models so this part of their business will remain their “cash cow” but the future success of this company depends on their SuperVision technology and their autonomous vehicle (AV) technology. There are lots of companies going after this market with different technologies — to understand how Mobileye is different and which technologies they are using compared to their competitors (including Tesla) please refer to part 1 of the MBLY writeup.

TBH, I’m so impressed with the technology from companies like MBLY and how they are going to change/shape the future of transportation and mobility. It’s very possible within 3-5 years many of our cars have some form of self-driving mode and that most ridesharing companies offer an autonomous driver option at a cheaper price because now they don’t have to share 70% of the revenues with their human drivers. However this pivot means higher capex because now they have to own their fleets which changes the business model quite drastically. As an UBER shareholder I’m curious to see how this story unfolds and how these companies either combine forces or become competitors. Cruise [click here], which is owned by General Motors (GM) is another company racing down the AV/ridesharing path.

If you have a few minutes, here’s a 40 minute video from Mobileye showing their AV technology in action