Deep dive writeup on SmartRent ($SMRT)

For all subscribers

In addition to my Substack newsletter, I also run a Stocktwits room where I post my current holdings, buys & sells, investment models, technical analysis and market commentary for both my Investment Portfolio (long term, strong fundamentals, 20-30 holdings) and my Trading Portfolio (short term, strong technicals, 0-10 holdings). The two options are $15/month for the monthly plan [click here] or $150/year for the annual plan [click here].

You can now signup for my new Substack called Jonah’s Trading Charts which is focused exclusively on the technicals — every day (usually pre-market) I’ll send out an email with my favorite trading charts/setups. You’ll also have access to my trading portfolio with current positions/sizes, entry/exit prices, profits/losses and much more. I’m also doing live charting and live trading 3-4 times per week.

Company: SmartRent

Ticker: $SMRT

Website: SmartRent.com

IPO date via SPAC: August 25, 2021 [click here]

Price at time of deSPAC: $12.00

Current stock price: $5.80

Outstanding shares: 194 million

52 week high: $15.14 on September 7, 2021

52 week low: $6.29 on February 24, 2022

Market cap: $1.124 billion

Enterprise value: $655 million

Headquarters: Scottsdale, Arizona, USA

Number of employees: 580+

Average price target from analysts: $12.20

Investor Relations [click here]

SmartRent will report 2021 Q4 earnings on Thursday, March 24 [click here]

Q3 2021 Earnings Report [click here]

Q3 2021 Earnings Call Transcript [click here]

Investor Presentation, January 2022 [click here]

Deutsche Bank Virtual Tech Conference [click here]

Interview with the Co-Founder of SmartRent:

I worked on this $SMRT writeup with Dan, you can find him at @10baggerdan

INTRODUCTION:

I’ve never owned SmartRent in my portfolio but it’s definitely on my watchlist. To be honest I had never even heard of this company until a few weeks ago when someone brought it to my attention — but after doing some due diligence and this writeup I’m pretty excited about the future potential with this company.

Since the company is reporting earnings later this month (March 24th) I’m still undecided as to whether I will start a position in the next couple weeks. SmartRent could certainly go lower in the near term and the technicals look horrible (we’ll discuss later) but longer term I think this stock could be a big winner. Even though the company is not profitable yet and likely won’t be until next year (2023), the revenue growth is extremely impressive, valuation is very reasonable and gross margins should increase substantially over the next few years as those high-margin recurring revenues start to kick in — this is similar to $STEM’s business model where they have low margins in the early years because of the hardware component but as time goes on those software margins are in the 70-80% range and help drive some significant profitability.

If you look at the forward estimates from the 7 analysts that cover the stock, it appears there could be significant upside however there are also plenty of risks that $SMRT will need to overcome.

I hope you enjoy this writeup.

OUTLINE:

Company Background

Opportunity

Technology

Revenue Model

Customers

Competitive Advantages

Management

Culture

Financials

Key Metrics

Optionality

Risks

Ownership

Valuation

Analysts

Technicals

Conclusion

This video is a couple years old — SmartRent has a much stronger portfolio of products and services these days but it still gives you a rough idea of what they do:

COMPANY BACKGROUND:

SmartRent was founded in 2017 by two co-founders, Lucas Haldeman (current CEO) and Mitch Karren (current CPO). Haldeman has a strong background in the real estate industry. He was a CTO of one of the largest single-family rental companies, Colony Starwood Homes, when he decided to start SmartRent. It came out of frustration: for years, Heldman and his colleagues were looking for a solution that could connect hundreds of thousands of different smart devices deployed across more than 44,000 homes nationwide.

"The problem is that there are a lot of different smart devices. We all have some in our homes. But no one ever thought about enterprise management of these devices. How do we as an operator have hundreds of thousands, even millions, of these different devices and manage them from one place?" – Lucas Haldeman, co-founder and CEO of SmartRent.

Heldman experienced this pain firsthand and decided to accept the challenge to solve this problem even though there were already some companies trying to tackle it. That is how SmartRent was born. He assembled a small team and went on the mission to create an enterprise-grade operating system that could integrate hardware from any manufacturer. SmartRent is one of those rare companies founded by necessity and by people from the industry, not Silicon Valley.

The company first launched the platform for single-family rentals. After years of tests in over 25,000 homes spanning 15 states and hundreds of iterations, it was finally ready for the scale in 2020. The solution the company eventually launched was designed for any type of rental space: single home, multifamily, vacation, student housing, senior housing, new construction homes. SmartRent's open platform already supports hundreds of integrations with hardware manufacturers including Google Nest, Ring, Schlage, Kwikset, Resideo, Honeywell, Bosch, Inovelli and Lutron — and across many different smart products such as cameras, doorbells, hubs, plugs, sensors, switches, thermostats, and more.

In 2020, they acquired Zipato, a smart home manufacturing company from Croatia with international operations. Zipato manufactures certain devices for SmartRent under the Alloy brand. As per the management, this acquisition proved to be so successful for the company that it had paid off for itself within the first twelve months due to gross margin savings.

SmartRent doesn't just sell the hardware shipped in the box. They are also engaged in its installation since owners do not employ tech-savvy specialists who can deal with smart homes. Now the company employs teams around the country who deploy all these devices for the customers.

In just a few years, SmartRent technology transformed from a "nice to have" to a "need to have" as more and more people started to adopt gadgets to manage their homes.

No wonder why the company attracted huge interest from different investors, not only from top-tier, best-in-class venture investors like Bain Capital, Spark Capital, Fifth Wall, Energy Impact Partners, and RET Ventures but also from industry leaders like Amazon's Alexa Fund and influential real estate owners like Lennar (the largest US homebuilder), Essex Property Trust and UDR (two of the largest multifamily owners in the US). In total, the company raised just a little bit over $100 million [click here]. The latter also deployed the underlying product across their portfolios — this is why strategic investors can be extra valuable when scaling a business.

The new chapter for SmartRent began recently, in 2021, with an establishment of more deep relationships with Fifth Wall, the largest and most active venture capital investor in proptech (property technology). Fifth Wall ultimately took SmartRent public in August 2021 via SPAC. Fifth Wall also pioneered a unique approach: they bring together many of the largest real estate corporations into their fund as investors or strategic limited partners. Later these corporations become users of the technology in which Fifth Wall invests — but that's not all, Fifth Wall's goal is to make sure that SmartRent is the vendor of choice.

"With our introduction to the public market, we plan to accelerate our growth in the multifamily market, expand our reach into global markets, boost our best-in-class product suite and supercharge our M&A strategy. We can't imagine a better investment partner than Fifth Wall to help us take SmartRent to the next level." – Lucas Haldeman, co-founder and CEO of SmartRent.

OPPORTUNITY:

Digitization of homes and rental properties is just getting started. It got a heavy boost during the pandemic, accelerating the necessity of smart devices. For instance, self-guided tours at some point have been the only way to conduct business and have since become the norm in the industry. It allows prospective renters and homebuyers to search and safely tour the properties without an agent present.

In the past, in some states, Sunday was a no business day since agents were not allowed to work on this day. Now, with self-guided tours, Sundays are the busiest day of the week. And according to the research SmartRent has conducted with multiple multifamily operators, more than 60% of renters prefer self-guided tours versus tours with agents. Self-guided tours are only possible with the installation of smart home devices.

The pandemic is not the only reason why the digitization of real estate is accelerating. The infrastructure spending will further expand home digitization. Smart-building offerings will become commonplace in the new construction, as well as in the existing neighborhoods and communities that will be severely renovated and upgraded.

The infrastructure bill also includes $47 billion for helping to preserve properties that are affected by changes brought on by climate change. ESG is a massive part of SmartRent's story, which is in the early innings. The real estate industry must reduce its energy consumption and decarbonize. Various carbon neutrality laws for the real estate industry are being enacted throughout the US, and with the US's re-entry to the Paris Climate Agreement, US landlords will need to monitor, reduce, and report on energy consumption through technologies deployed across their portfolios.

The demand for smart home technology is rapidly increasing among residents, while smart home penetration in rental is still severely lagging. Entrata estimates that more than 75% of residents would pay more for an apartment equipped with smart home technology, and Schlage estimates Millennials would be willing to pay 20% more on average per month for rental units equipped with smart home technology. More owners and operators in both the multifamily residential and single-family rental home sectors evolve to meet this growing demand for integrated smart home solutions.

In addition, the same driving forces apply to other asset classes, for example, commercial real estate. We will see more properties in all asset classes transform from outdated to fully connected smart communities, meeting resident demand for digital amenities while improving profitability for owners and operators.

The opportunity does not end in the US, where SmartRent currently operates, and the company is looking to expand smart home solutions into other markets globally. Some pilot programs and developed partnerships are already in place in the United Kingdom, Canada, the Netherlands, and Ireland. More countries to come in the near future.

TECHNOLOGY:

SmartRent pioneered a hardware-agnostic, enterprise-grade operating system that allows owners and operators to holistically manage all smart devices across a residential asset or portfolio.

This approach has a strong value proposition for both owners/operators and consumers.

Owners and operators can:

Increase revenue (residents are ready to pay more for smart apartments);

Reduce costs (by limiting damage (for example, putting leak sensors to avoid water damage), by reducing energy expenses, and by automatic manual processes);

Reduce the complexity of running the properties (by bringing the entire smart ecosystem onto a single, user-intuitive platform for the property manager to control);

Consumers can have a modern living experience: create access codes for dog walkers or learn when the kids are coming home from school. Most importantly, it helps save money on utility bills – a strong proposition for any consumer. Potentially, it will retain tenants longer and reduce churn.

The company offers a variety of smart home products and solutions. You can learn more about them here – https://smartrent.com/products/.

At the core of everything is a SmartHub manufactured by Zipato and sold by SmartRent. It allows the user to control and manage a variety of third-party smart devices from various manufacturers. Using the on-wall touchscreen unit, users can run a scene, change the temperature, lock or unlock doors, let someone in the building, and more, all from one intuitive interface. Users can also download the companion app to control their devices and grant access remotely for guests, vendors, or delivery drivers.

The SmartHub connects to the Internet via built-in cellular connectivity. If hubs are not connected, users lose the ability to remotely manage the devices. One of the key solutions offered by SmartRent is a Community Wi-Fi that offers additional coverage if cellular connectivity is poor or not available.

The company offers a variety of smart devices that elevate the resident experience and provide multiple benefits to owners and operators. A typical SmartRent rental unit or single-family rental home is equipped with a SmartHub, smart locks, thermostat, and leak sensors. In addition, several other devices are supported: smart plugs and lighting (including light bulbs, switches, and dimmers), shades, garage door controllers, video doorbells, peephole cameras, video intercoms, contact and motion sensors, voice assistants, and more. And since the software is hardware agnostic, the customers can choose from a wide variety of device manufacturers, available at any price point and tailored to satisfy any needs.

After all smart devices are connected to the SmartHub, they become available to be managed remotely using the company's core smart home operating system, Community Manager. It is available both on the web and via mobile apps on iOS and Android.

Community Manager software integrates with many popular property management, customer relationship management, and other third-party software products, enabling owners and operators to manage all resident, prospect, access, and other actionable data from one platform. Managers can remove access codes from locks, create work orders for turn requests, and activate energy-saving modes.

What managers can also use now is a white-label resident app that they can brand for a specific property, which personalizes the resident experience while consolidating the control and functionality of all of the SmartRent devices being utilized in the community. It also allows for other online services or marketplace operators affiliated with that community. This app is an additional offering to SmartRent's legacy resident app that engages with approximately 570,000 resident users and the property staff app with around 17,000 users.

Since SmartRent does all the installations for the customers, it is very easy and fast to get started. With some solutions like Self-Guided Tours, the customer can receive a customized DIY tour package designed specifically for self-installation and self-implementation and begin offering self-guided tours in as little as 48 hours.

REVENUE MODEL:

SmartRent's revenue model is a combination of recurring fees for software (Hosted Services Revenue) and one-off payments for hardware (Hardware Revenue) and installation (Professional Services Revenue).

Hardware and installations are very low-margin (10-20%) revenue stream in the short term, while software offers a very high-margin (70-80%) revenue stream over the long term. At the moment, the company uses a “loss leader” strategy to sell and install the hardware at essentially no profit in order entice the customer to become a long-term subscriber. Usually, the company enters into the binding, recurring revenue contracts with customers that typically have terms of five to seven years, and most customers prepay their SaaS contract subscription fees. It allows the company to have highly predictable revenue.

This model should work at scale. With very sticky customers (as demonstrated by an incredible 0% churn since the company's inception), the company will be able to build a strong and increasing average revenue per user (ARR) which will also drive margin expansion over time (similar to $STEM).

The company's recurring revenues:

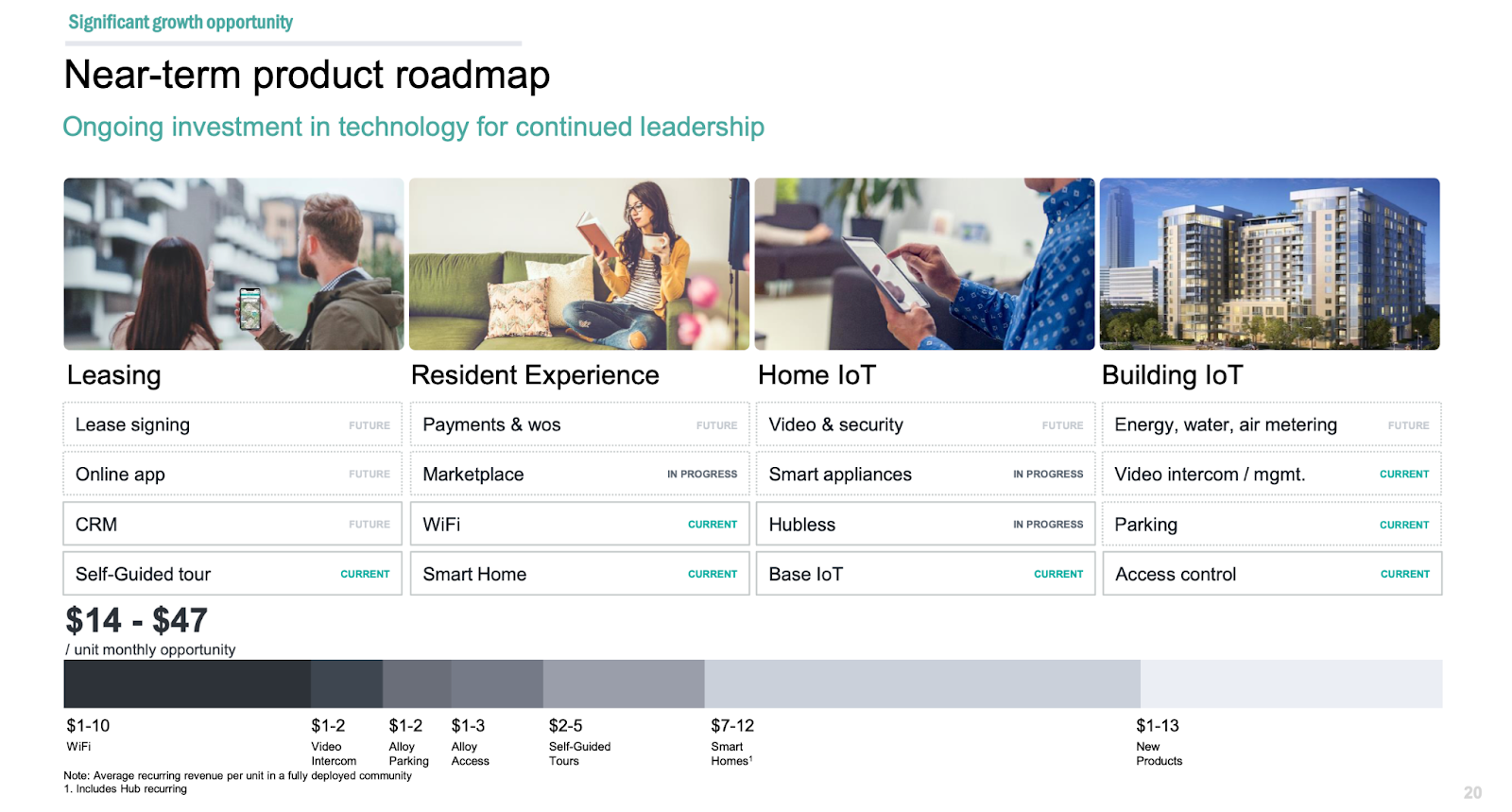

The recurring revenue from the Alloy Access solution ranges from $1 to $3 per rental unit per month.

The recurring revenue from the Alloy Parking solution ranges from $1 to $2 per rental unit per month.

The recurring revenue from our Self-Guided Tours solution ranges from $2 to $5 per rental unit per month.

The recurring revenue from our Community Wi-Fi solution ranges from $1 to $10 per rental unit per month.

The recurring revenue from our smart home automation solution ranges from $7 to $14 per rental unit per month, including recurring SmartHub fees.

SmartRent has a lot on the product map. More products and solutions are expected to be launched in the upcoming future, increasing the offering to the customers and opening new or expanding existing revenue streams.

In addition, the company uses a dynamic land-and-expand model, where every product can be an entry point. Once SmartRent has been deployed as the smart home operating system for the property manager around a single given need or pain-point, it has significant up-sell and cross-sell opportunities that all integrate onto the SmartRent platform.

CUSTOMERS:

SmartRent serves customers of all sizes and types: from single-family rental homes and new development properties to multifamily residential properties and other asset classes, such as senior and student housing.

The company has a history of strong growth in the multifamily segment due to robust relationships established with leading multifamily home owners and operators. Apart from multifamily, the company also targets single-family rental residences and new home builders / iBuyers that can easily incorporate the company's solutions and serve as an additional channel through which these solutions can be offered.

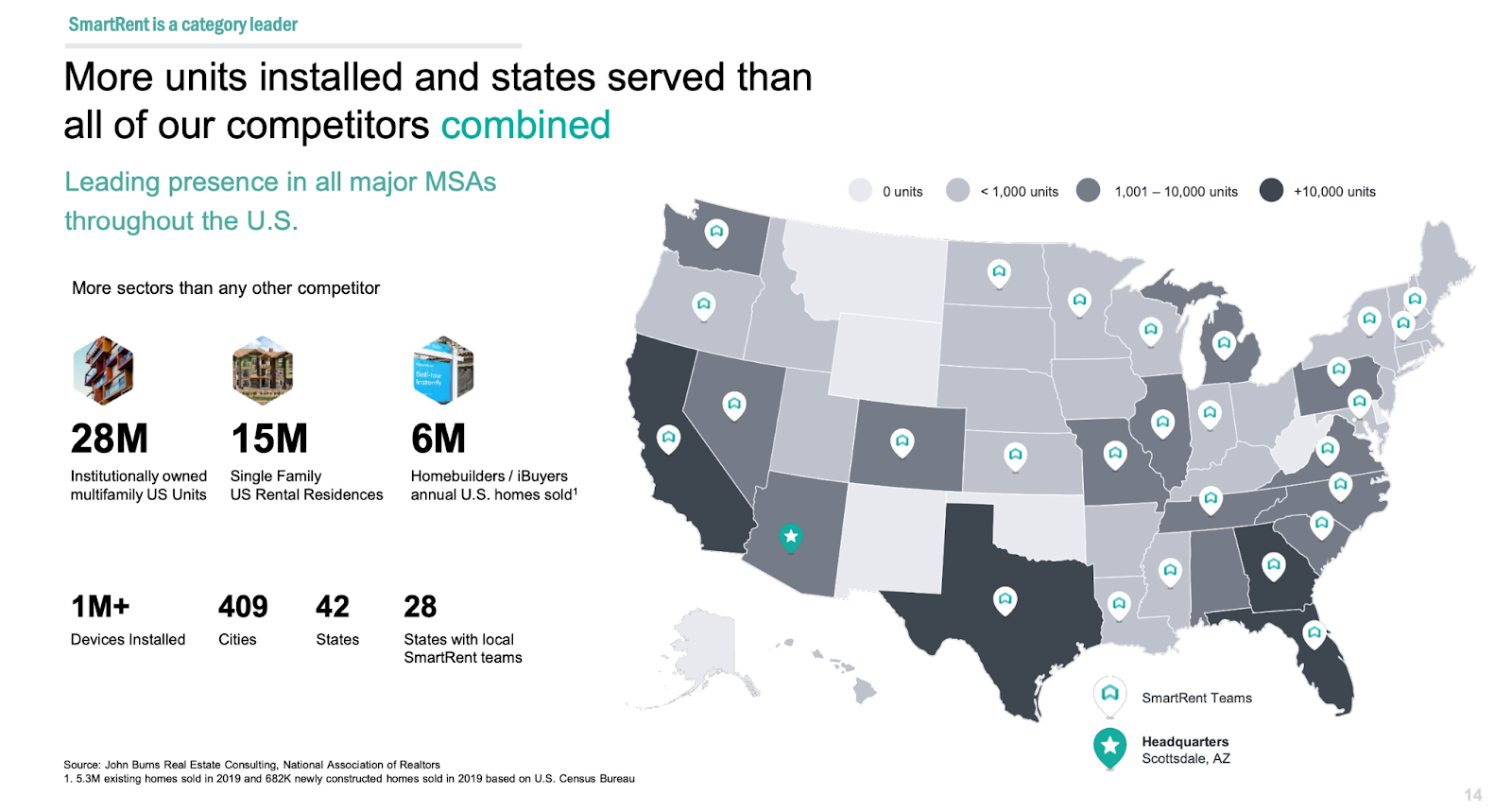

Today, in the US, there are 43 million institutionally owned residential units and 6 million newly constructed and existing properties that will become smart-enabled over the next 5 years. Less than 500,000 of those units have any kind of smart-enablement right now.

According to surveys with the largest multifamily owners made by Fifth Wall, the industry had overwhelmingly voted in favor of SmartRent as the industry-standard operating system.

This is evident by an outstanding 0% churn rate. No single unit was ever removed from the apartment. It creates very sticky relationships with customers. Once the company gets in, which is the hardest part, customers become true partners for SmartRent for many years ahead.

From existing customers alone, SmartRent sees an opportunity to generate up to $1.5 billion in annual revenues. The total opportunity for the residential market is $30 billion.

SmartRent is poised to expand rapidly into the largest residential real estate portfolios in the US and significantly dominate the market as a clear category leader.

But the domestic residential real estate market is just the beginning for the company. First, the company is looking to expand to other asset classes in the US, particularly the senior housing and student housing sectors, since they have many similarities with the core addressable market. The company already actively serves student housing. The market opportunity for other asset classes is estimated to be $80 billion.

And finally, the international expansion provides the biggest opportunity of them all, with over $200 billion in total potential revenue.

COMPETITIVE ADVANTAGES:

SmartRent has developed several strong competitive advantages that allow the company to significantly differentiate itself from its competitors.

To begin with, there is not a lot of competition at the moment in what SmartRent does. All competitors are either focused on creating solutions for new construction buildings, which represent only a fraction of the total market size, or have closed-architecture systems that do not allow integration with existing products or software systems that owners and operators have already installed.

One particular company, Latch (also now a public company and trades under the ticket $LTCH), is the closest competitor to SmartRent. Both companies are considered to be market leaders in enterprise smart home management. But unlike SmartRent, Latch focuses only on new developments and builds its own variety of smart home devices like smart locks, intercoms, cameras, etc. Some compare these two companies to Apple (Latch) and Android (SmartRent), where Latch focuses on premium products and has a more closed system (though they allow connecting certain third-party devices to its Latch OS) and SmartRent is totally opposite. Indeed, the main competitive advantage that SmartRent has over Latch and others is its hardware-agnostic, open-architecture, integrated nature. In addition, the revenue and earnings forecasts for $LTCH over the next several years are significantly lower than those for $SMRT.

SmartRent can readily target the vast majority of the overall residential real estate market, if not all of it, including the new developments. And the largest, institutional, national-footprint real estate organizations had already adopted and named SmartRent a market-standard solution. It demonstrates the brand reputation the company already has. 15 of the top 20 multifamily landlords are SmartRent customers. As a result, SmartRent has more units installed and states served than all the competitors combined. Most likely, they will only accelerate from this point.

Being an open and integrated platform does not require customers to build multiple relationships with different vendors and make sure all integrations are seamlessly working together. SmartRent handles everything and makes it work from one single place. It is useful both for owners and tenants: owners have enterprise-level controls from a single platform for all the units in their portfolio, and tenants don't need to have separate apps to control thermostats, shades, locks, parking control, etc.

Another competitive advantage comes from the high switching costs that occur in this business. The costs of hardware installation and replacement are making SmartRent almost bulletproof. Once they get in, they stay in business for years, demonstrating how their customer base is sticky.

The barriers to entry make another competitive advantage. Rolling out an integrated enterprise solution across a portfolio of rental units is not an easy task, which requires time and resources.

Nevertheless, the company expects competition to intensify in the near future as the market for smart home technology in the residential real estate industry continues to mature and will definitely attract new players who would want to grab their piece of this market.

MANAGEMENT:

SmartRent is a founder-led company with both founders at the head of the organization. The entire C-level is comprised of executives that have decades of experience in property management and developing innovative technologies within this sector.

What makes this management team stand out is how deeply they understand all the peculiarities of the real estate industry. The way how they 'won over' the most important firms in this industry proves the exceptionality of this group of people.

I also watched several interviews with top executives of multifamily owners and operators. Every single one of them said that they chose to do business with SmartRent because of Lucas Haldeman. Lucas comes from the real estate industry, specifically from a company that all LPs have huge respect for. He does not only have a deep understanding of the industry, but he also has a very strong technological background. When he decided to create SmartRent, he assembled a first-class team that is still around from day one.

Lucas Haldeman has served as the Chief Executive Officer and Chairman of the Board since the inception of the company in 2017. Mr. Haldeman has spent the last two decades innovating and developing property management technology for the real estate industry. Before founding SmartRent in 2017, Mr. Haldeman served as the chief technology and marketing officer of Colony Starwood Homes (now part of Invitation Homes Inc., a public company) from 2013 through 2016, where he and his team developed a platform that was instrumental in helping the business acquire, renovate, lease and manage more than 30,000 single-family homes. Previously, he served as the Chief Information and Technology Officer for Beazer Pre-Owned Rental Homes from 2012 through 2013 and was the founder and managing partner of Nexus Property Management, Inc. from 2006 through 2012. Mr. Haldeman earned his Bachelor of Specialized Studies degree in Economics and Business, English, and Computer Science from Cornell College.

Mitch Karren has served as the Chief Product Officer since the inception of the company in 2017. Mr. Karren oversees product management, partnerships and solution architects. Mr. Karren is responsible for managing the teams empathizing with SmartRent customers, solving problems and launching innovative tools. Prior to his role with SmartRent, he served as director of product at Colony Starwood Homes from 2013 to 2016, where he designed their custom end-to-end software platform and directed the first-ever large-scale deployment of 25,000 smart home systems in the rental industry. Mr. Karren earned a Bachelor of Science degree in Housing and Community Development from Arizona State University and is a licensed real estate broker in Arizona.

Demetrios Barnes has served as the Chief Operating Officer since the inception of the company in 2017. Mr. Barnes leads SmartRent’s support, field operations, and account services teams. With over a decade of experience in property management operations, Demetrios is passionate about helping owners and operators understand the innovations technology can produce while forging strong interpersonal relationships and participating in thought leadership discussions. Prior to SmartRent, he was vice president of technology for Colony Starwood Homes, director of property management and technology with Beazer Pre-Owned Rental Homes, and a regional manager for several multifamily companies. He holds a Bachelor of Science in Business Administration from Arizona State University.

Isaiah DeRose-Wilson has served as the Chief Technology Officer since the inception of the company in 2017. Mr. DeRose-Wilson is responsible for SmartRent’s design, hardware and firmware, mobile and web applications, quality assurance, and development operations divisions. As an integral member of the leadership team, Isaiah oversees the stability, security, and growth of SmartRent's software and hardware offerings. Before SmartRent, Mr. DeRose-Wilson spent 10 years working on projects ranging from low- to high-level programming languages, networking, hardware, IoT integrations, product and risk management, and compliance. His merits include leading a team that built a software platform responsible for facilitating operational workflows and communication surrounding Colony Starwood Homes' acquisition, accounting, maintenance, logistics, support, and ops teams to maintain and grow a portfolio of more than 40,000 single-family homes. He is currently focusing on leveraging emerging technologies to keep SmartRent as one of the nation's largest and most successful enterprise IoT solution providers.

CJ Edmonds has served as our Chief Revenue Officer since January 2020. Mr. Edmonds leads the business's revenue growth through new customer acquisition, customer expansion, and customer retention. Mr. Edmonds has more than 12 years of executive-level management experience in the SaaS and wireless industries. Prior to joining SmartRent, he ran the sales organization at G5 Search Marketing, Inc. from 2010 to 2019, delivering digital marketing solutions to the real estate sector. He was integral in growing the company from $4.0 million to $40.0 million in annual recurring revenue. Mr. Edmonds earned a Bachelor of Science degree in Business Administration and Economics from Saint Mary’s College of California.

Compensation for executive officers has three primary components: base salary, an annual cash incentive bonus, and long-term compensation in the form of equity grants. The company also provides additional employee benefit plans, including health insurance, disability insurance, life insurance, and 401(k) plans. According to SimplyWallSt, Lucas Haldeman's total compensation is below average for companies of similar size in the US market.

The company's board of directors is composed of 7 people, including Lucas Haldeman. Other notable members of the board of directors:

Frederick Tuomi, the lead independent director, served as President, Chief Executive Officer and director of Invitation Homes Inc. (NYSE: INVH), the nation’s largest single-family rental company, from 2017 until his retirement in 2019. Prior to its merger with Invitation Homes, Mr. Tuomi served as Chief Executive Officer and director of Starwood Waypoint Homes from 2016 until 2017. Prior to its merger with Starwood Waypoint Homes, he served as Co-President and Chief Operating Officer of Colony American Homes, Inc. from 2013 until 2016. Mr. Tuomi was Executive Vice President and President—Property Management for Equity Residential (NYSE:EQR), one of the nation’s largest multifamily REITs, from 1994 until his retirement in 2013. He led the development of Equity Residential’s property management group through years of rapid growth and expansion while helping to pioneer its leading operational platform. He has served on numerous real estate industry boards and executive committees throughout his career.

Robert Best is the founder, Chairman, and President of Westar Associates, a private real estate development company established in 1980. As President, Mr. Best has developed over 70 projects exceeding $2.0 billion across various commercial and residential product types throughout Southern California. Prior to founding Westar, Mr. Best was a partner with Carver Companies, where he was responsible for the acquisition, entitlement, leasing, finance, management, and disposition of shopping center development projects. Mr. Best also served as an Independent Trustee of Colony Starwood Homes from January 2016 to June 2017.

Bruce Strohm previously served as the Executive Vice-President, General Counsel and Corporate Secretary of Equity Residential (NYSE:EQR), an S&P 500 public company, from 1995 until January 2018. Equity Residential is one of the largest apartment companies in the United States, owning over 300 properties, with 80,000 units, with a market capitalization in excess of $30 billion. From 2018 to2019, Mr. Strohm was Chief Legal Officer of Equity International, a private equity company focusing on investing in real estate outside the United States.

All board members are owner-oriented, as they all hold shares of the company directly or through their firms. Robert Best, for example, holds 2% of the entire company and is the second-largest insider in the company.

CULTURE:

SmartRent's mission is "to bring smart home automation to property managers and renters." This statement does not sound like SmartRent is a mission-driven company, though it does not stop the company from building a great culture around what they do.

The company's culture is mainly built around making communities better. The company seeks to foster a welcoming, inclusive work environment where employees can be themselves and do meaningful work that positively impacts the communities. The culture is supportive, engaging, and fast-paced and facilitates partnerships among coworkers with diverse backgrounds and experiences. Employees are involved in resource groups and give back to the community not only through work itself but through various programs.

What makes SmartRent a great place to work is how they put employees first. The company offers comprehensive benefits that help employees thrive, including 100% employer-paid benefits for employees and their dependents (medical, dental, vision), life insurance, flexible time off, paid parental leave, a 401(k) plan with a company match, and stock purchase plans.

The company won numerous employee rewards: 2021 Best Places To Work In Multifamily and Azcentral Top Companies To Work For In Arizona 2020. The company also received several other rewards: The Next Billion-Dollar Startup 2020 from Forbes, UpStart 100 in 2019 from CNBC, and Fastest Growing Company from Growjo.

The company has a 4.4 / 5 score on Comparably with an A- overall culture score based on 449 ratings. SmartRent's CEO, Lucas Haldeman, has 22 employee ratings and a score of 87/100.

Currently, the company employs over 580 full-time employees worldwide (dedicated teams in Canada and the UK). Most of the employees are engaged in engineering, software and product development, sales, and related functions. They also hire consultants and contractors to supplement the permanent workforce. As per management comments in the latest conference call, the company does not experience any problems with hiring the necessary talent.

FINANCIALS:

All information below is based on the financial performance of SmartRent in the most recent quarter (Q3 2021) reported on November 10, 2021.

Income Statement

Revenue

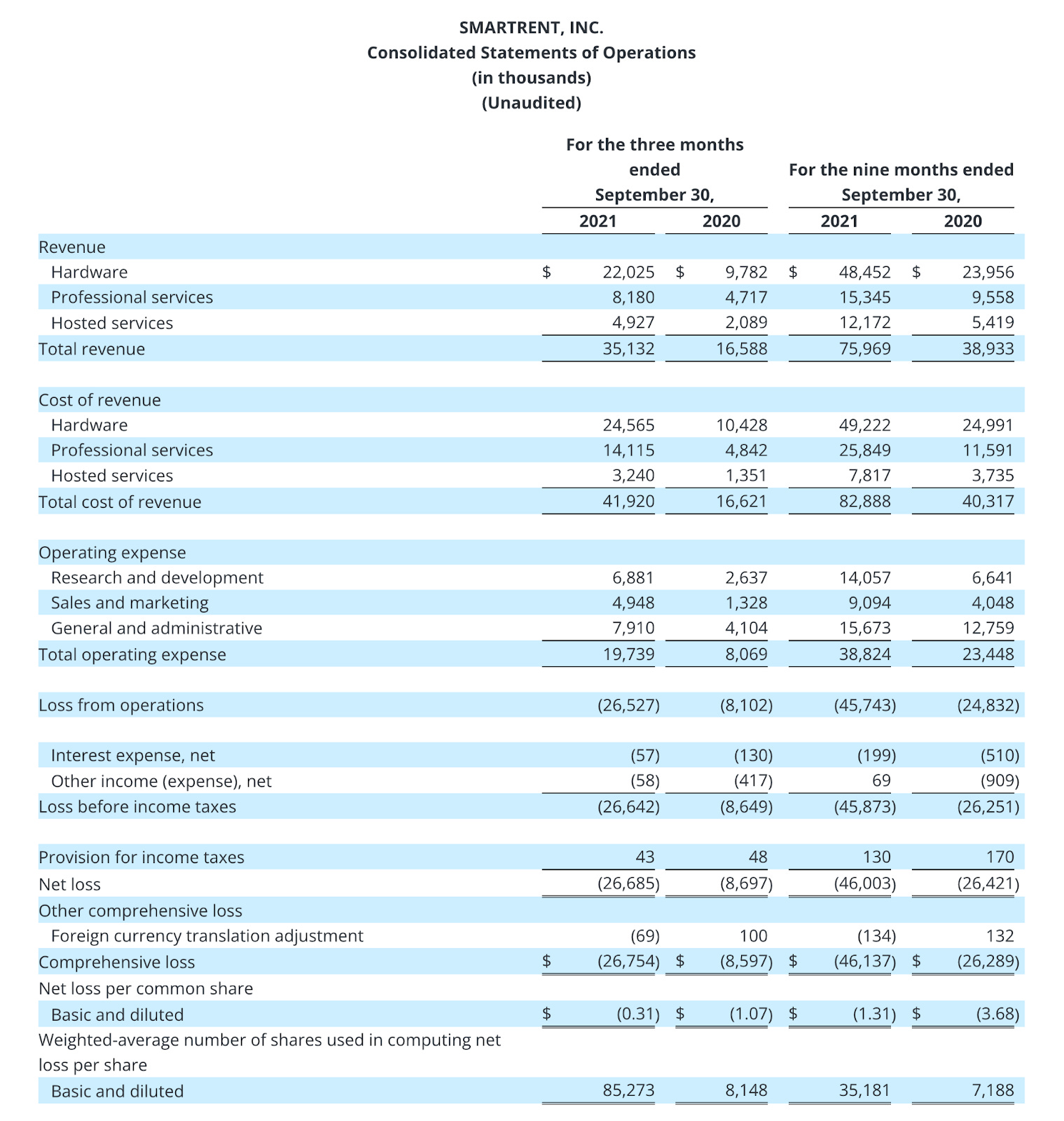

SmartRent reported a record quarter, with total revenues of $35.1 million compared to $16.6 million in Q3 2020, representing a staggering 112% year-over-year and 62% quarter-on-quarter growth.

The success in this quarter was primarily driven by numerous revenue and operational milestones driven by growing customer demand and accelerated execution by the field installation teams.

The strong growth had been seen in the hosted services (recurring subscriptions) that saw 136% growth year-over-year. Hosted services represent 14% of total revenue, a slight increase from 12.6% a year ago but a decrease from 19% in Q2 2021.

Gross Margin

The total gross margin for the third quarter was negative 19.43%, compared to negative 0.39% in Q3 2020 and positive 1.41% in Q2 2021. This increased negative gross margin was due to the hardware gross profit that was reduced by $5.7 million of warranty provision related to deficient batteries in some of our smart hub units.

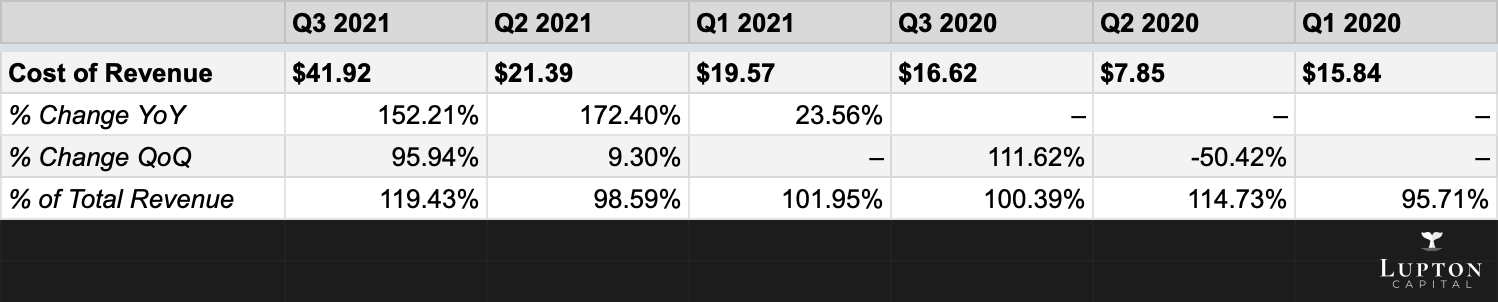

Cost of Revenue

The cost of revenue in this quarter increased 152% year-over-year and almost doubled from Q2 2021. It represents 120% of total revenue, indicating that the company currently works at a loss.

Operating Expenses

Research and development (R&D) expenses were $6.8 million, an increase of 161% from $2.64 million in Q3 2020 and 68.5% from $4.08 million in Q2 2021. R&D expenses remained at a healthy 19% range of total revenue, indicating a continuous investment in innovation.

Sales and marketing (S&M) expenses were $4.95 million, an increase of 272.5% from $1.33 million in Q3 2020 and 106.8% from $2.39 million in Q2 2021. However, S&M expenses accounted for only 14% of total revenue, indicating the lower customer acquisition costs (CAC) and effective marketing and sales efforts.

General and administrative (G&A) expenses were $7.9 million, an increase of 93% from $4.1 million in Q3 2020 and 108% from $3.81 million in Q2 2021. G&A expenses accounted for 22.5% of total revenue, a slight decrease from the year-ago.

Operating expenses in the third quarter increased by 145% to $19.7 million from $8.1 million last year, reflecting several factors, including an increase of $3.4 million in personnel expense due to the increased headcount as the company ramps the workforce to meet the growing demand. Other drivers of expense in this quarter included company-related public expenditures, such as insurance, professional fees, and non-cash stock-based compensation of approximately $4.3 million.

Guidance

The company remains on track to deliver approximately 161,000 deployed units in 2021, but refining the revenue projections to a range of $100 million to $105 million from $119 million expected previously. This revision reflects ongoing supply chain constraints, which have created a backlog in the deployment of the Fusion Hub and the Alloy Access product.

The company also anticipates that hardware revenue will be the primary revenue driver in 2021, reflecting the thousands of units they are currently deploying.

The company did not provide any guidance for 2022 on the conference call. However, on January 11, 2022, the company provided a business update. For the full year 2021, the company expects to report total revenue in the range of $106-$109M, beating the previously provided revenue range of $100-$105M. They managed to deploy additional 6,000 units in Q4.

“We closed the year on a strong note exceeding both our 161,000 Units Deployed target as well as our revised revenue guidance.” – Lucas Haldeman, CEO of SmartRent.

Balance Sheet

The company ended the third quarter with $472.5 million and $3.6 million of outstanding term debt. $445 million came from the business combination with Fifth Wall Acquisition Corp. The balance sheet looks very strong and will help the company further expand the workforce, develop products on the road map, and select external growth opportunities.

Profitability

The company is currently unprofitable. They reported an operating loss of $26.5 million in Q3 2021, and EBITDA came at a negative $26.45 million. Net loss was $26.69 million compared to $8.7 million a year ago, reflecting primarily the gross profit decline and increased operating expenses.

The company projects to become EBITDA positive and show net income in 2023.

Cash Flow

Cash flow from operations for the third quarter of 2021 came in at a negative $23.06 million.

Cash flow from investing for the third quarter of 2021 came in as an outflow of $2.51 million, mainly attributable to loan repayment.

Cash flow from financing for the third quarter of 2021 came in as an inflow of $444.57 million from proceeds raised through a SPAC sponsor and PIPE investors.

The company keeps burning cash and, as a result, has a negative free cash flow of $22.5 million for the third quarter of 2021. The company will continue burning cash throughout 2022 until they plan to become cash flow positive in 2023.

KEY METRICS:

The company regularly monitors a number of operating and financial metrics to evaluate the operating performance, identify trends affecting the business, formulate business plans, measure the progress and make strategic decisions.

Units Deployed and New Units Deployed

The company defines “Units Deployed” as the aggregate number of SmartHubs that have been installed as of a stated measurement date (i.e., for all the time up to this moment). The New Units Deployed are defined as the aggregate number of SmartHubs that were installed during a stated measurement period (i.e., between Q2 and Q3 2021).

The company uses these operating metrics to assess the general health and trajectory of the business and growth.

Committed Units

The company defines “Committed Units” as the aggregate number of SmartHub units that are subject to binding orders from customers plus units that existing customers (who are parties to a SmartRent master services agreement) have informed us (on a non-binding basis) that they intend to order in the future for deployment within two years of the measurement date.

The company uses this operating metric to assess the general health and trajectory of the business and to assist in the longer-term resource analysis.

Units Booked

The company defines “Units Booked” as the aggregate number of SmartHub units associated with binding orders executed during a stated measurement period.

The company utilizes the concept of Units Booked to measure estimated near-term resource demand and the resulting approximate range of post-delivery revenue that we will earn and record.

Units Booked represent binding orders only and are a subset of Committed Units.

Annual Recurring Revenue

The company defines Annual Recurring Revenue (“ARR”) as the annualized value of the recurring SaaS services revenue earned in the current quarter. It does not contemplate revenue that could be attributed to Committed Units.

The company monitors ARR to assess the general health and trajectory of our hosted services business, which is long-term, should become the main driver for the company's profitability.

EBITDA and Adjusted EBITDA

The company defines “EBITDA” as net income or loss computed according to GAAP before the following items: interest expense, income tax expense, depreciation, and amortization.

The company defines "Adjusted EBITDA" as EBITDA before the following items: stock-based compensation expense, non-employee warrant expense, loss on extinguishment of debt, change in fair value of derivatives, unrealized gains and losses in currency exchange rates, and other income and expenses.

Management uses EBITDA and Adjusted EBITDA to identify controllable expenses and make decisions designed to help the company meet the current financial goals and optimize the financial performance while neutralizing the impact of expenses included in the operating results, which could otherwise mask underlying trends in the business.

Revenue

The company generates revenue primarily from sales of systems that consist of hardware devices, professional installation services, and hosted services.

The revenue is recorded as earned when control of these products and services are transferred to the customer in an amount that reflects the consideration expected to collect for those products and services.

Hardware Revenue

The company generates revenue from the direct sale to customers of hardware smart home devices, which devices currently consist of door-locks, thermostats, sensors, and light switches. The sale of SmartHub is not included in hardware revenue.

Professional Services Revenue

The company generates professional services revenue from installing smart home hardware devices. Installations can be performed by the company's employees, or can be contracted out to a third party with the company's employees managing the engagement, or can be performed by the customer with the company's employees managing the engagement. Professional services contracts are generally performed on a fixed-price basis.

Hosted Services Revenue

Hosted services include recurring monthly subscription revenue earned from the fees collected from customers to provide access to one or more of the software applications, including access controls, asset monitoring, WiFi, and other related services. These subscription arrangements have contractual terms typically ranging from one month to seven years and include recurring fixed plan subscription fees.

The company sells the hardware SmartHub device, which only functions with the subscription to the proprietary software applications and related hosting services. They consider the SmartHub device and hosting services subscription as a single performance obligation.

OPTIONALITY:

SmartRent does not have any visible optionality at this moment. The company is too young to explore other revenue options beyond residential real estate. There is plenty to gain in this particular market.

The only optionality, if it could be classified as such, comes from other asset classes that SmartRent can target in the near future, specifically commercial real estate. This market is large enough to create almost identical business for the company as residential real estate right now.

With large enough cash on the balance sheet and access to public capital, the company will likely be aggressive on the M&A side. Newly acquired businesses could add additional revenue streams for the company, but knowing the nature of its land-to-expand model, with a high probability the company will integrate new technologies into the core of its platform, rather than looking for something that will be outside of its ecosystem.

RISKS:

The company believes that its future success will be dependent on many factors. The future operating results and cash flows are dependent upon a number of opportunities, challenges, and other factors, including the company's ability to grow the customer base cost-effectively, expand the hardware and hosted service offerings to generate increased revenue per Unit Deployed, provide high-quality hardware products and hosted service applications to maximize revenue and improve the leverage of the business model.

While these areas represent opportunities for the company, they also represent challenges and risks that they must successfully address to operate the business.

Investing in Research and Development

The company's performance is significantly dependent on the investments made in research and development, including attracting and retaining highly-skilled research and development personnel.

The company must continually develop and introduce innovative new software services and hardware products, integrate with third-party products and services, mobile applications, and other new offerings. If they fail to innovate and enhance the brand and products, the market position and revenue will likely be adversely affected.

Active Supply Chain Management

The company is highly focused on successfully navigating global supply chain disruptions. The increased demand for electronics as a result of the

COVID-19 pandemic, the US trade relations with China, and certain other factors have led to a global shortage of semiconductors, including

Z-wave chips, which are a central component of the SmartHubs.

Due to this shortage, the company has experienced SmartHub production delays. The company believes these supply chain disruptions may continue throughout 2022 and beyond. This will have an operational impact to some degree.

New Products, Features and Functionality

The company needs to spend additional resources to continue introducing new products, features, and functionality to enhance the value of its smart home operating system.

The company continuously introduces product enhancements and features. The most recent are Building Access Control, Video Intercom, WiFi, and Parking Management solutions.

In the future, the company intends to continue to release new products and solutions and enhance the existing products and solutions, which as a result will impact the operating results.

Category Adoption and Market Growth

The future growth depends partly on the continued consumer adoption of hardware and software products which improve resident experience and the development of this market.

The company needs to deliver solutions that enhance the resident experience and deliver value to the customers, rental property owners, and operators, as well as homebuilders and developers, by providing products and solutions designed to enhance visibility and control over assets while providing additional revenue opportunities.

In addition, the long-term growth depends partly on the ability to expand into international markets in the future.

OWNERSHIP:

SmartRent's ownership breakdown as of Q3 2021:

According to SimplyWallSt, VC/PE firms (specifically RET Ventures, Bain Capital Venture Investors, Spark Capital Partners, Fifth Wall) hold the most significant part of the company – almost 40%. Next comes institutions (including BlackRock, The Vanguard Group, Luxor Capital Group, and others) that hold approximately 27% of the company. In the third position is the general public, which owns about 14%. Individual insiders own around 8% (including Lucas Haldeman, who owns almost 5.6%), and the SPAC sponsor, Fifth Wall, holds about 5%. The remaining (around 6%) belongs to one of the largest real estate operators and owners, Lennar.

Like most SPACs and IPOs, there is always going to be some selling pressure from insiders and early investors in the first 18 months. Eventually many of the largest shareholders in $SMRT will need to sell down their positions in order to return capital to their own investors. Sometimes this selling pressure has no impact on the stock price but sometimes it does. Either way it’s something to keep an eye on.

All insider shareholders were subject to 180 days lockup that should have expired on February 25, 2021. No recent 13G forms showed that insiders sold any shares. On the contrary, insiders have been purchasing more shares in the past 6 months, including Lucas Haldeman, who bought additional 10,500 shares in late 2021.

VALUATION:

Even though SmartRent is still unprofitable there are lots of reasons to consider owning this stock and valuation is one of them. Since the company is expected to lose ~$60M in 2021 and another ~$57M in 2022 it’s probably best to look at 2024 numbers and try to figure out where $SMRT could be trading “if” they hit these numbers below.

The analysts that cover this company are looking for explosive revenue growth over the next 3 years — not the kind of numbers you usually see from a hardware/software company but it reflects the growth potential in their industry which they seem well positioned to capitalize on.

Trying to value $SMRT on 2022 numbers is very difficult, we can use price/sales but it’s such a horrible metric these days. I prefer to look out a few years and try to use reasonable estimates to come up with a potential price target based on those numbers.

If SmartRent can get to $1B+ in revenues in 2024 with net income margins in the 10% range, then here are the numbers:

2024: $1 billion in revs x 10% NIMs = $100M of net income

$100M of net income x 40 multiple (this is probably low considering what the earnings rate would likely be in 2024) = $4.0B

$4.0B + $400M of cash (could be slightly more than this) = $4.5 enterprise value

$4.5B projected EV / current EV of $655M = 6.8x potential return through 2024

6.8x over the next 3 years would be a CAGR of almost 90%

PS: I didn’t include any share dilution however there’s likely to be some as they dish out stock options to retain talent

I’m certainly not going to predict that SmartRent turns into an 8-bagger over the next 3-4 years however if $SMRT hits the numbers I outlined above on both top and bottom line and assuming a 40x multiple on net income (very reasonable) then SmartRent shareholders could see some sizable gains.

ANALYSTS:

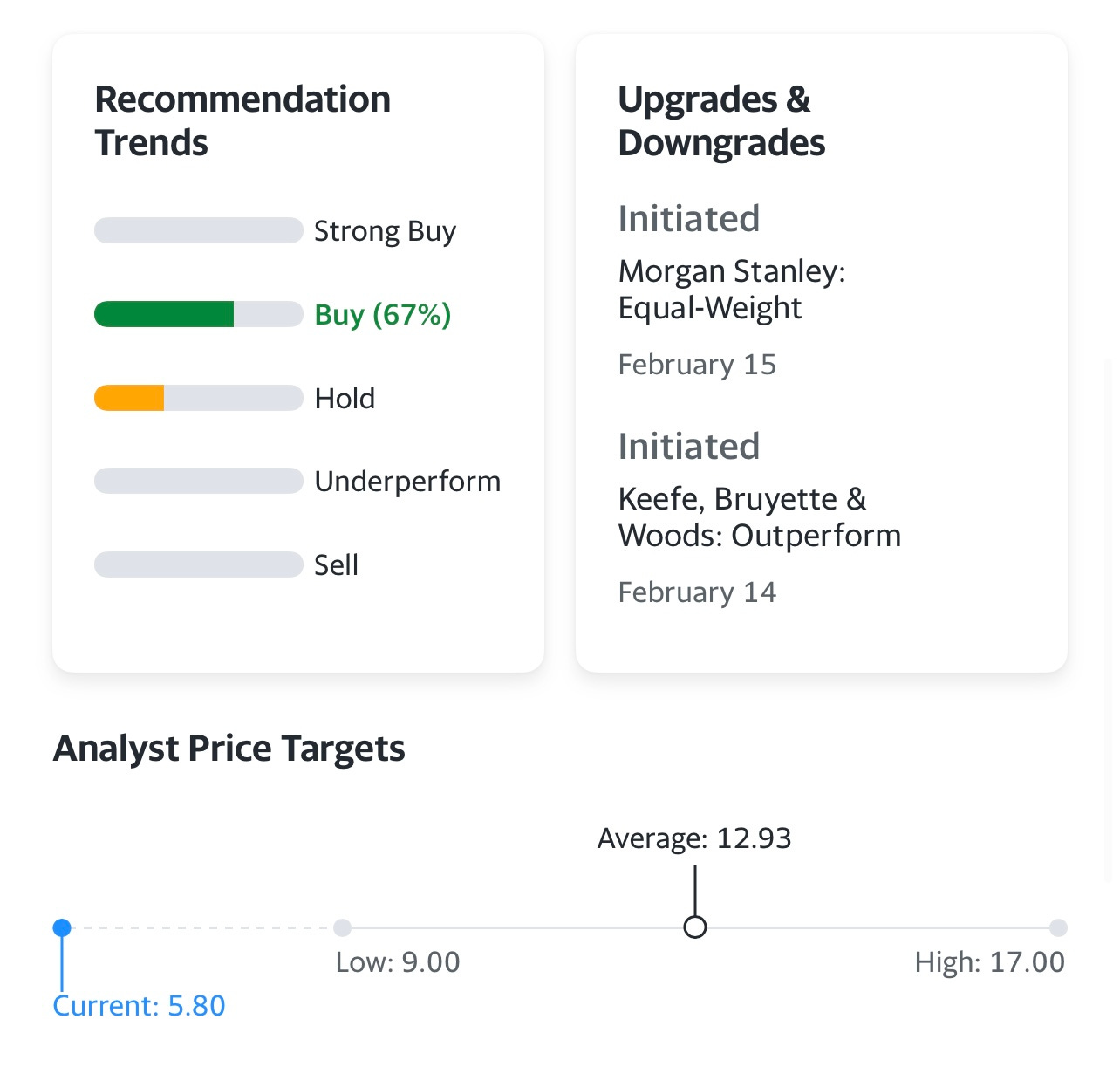

According to my research there are now 7 firms/analysts that cover SmartRent, with 5 having BUY ratings and 2 having HOLD ratings.

BUY: Keefe Bruyette, Colliers, DA Davidson, Deutsche Bank, Goldman Sachs

HOLD: Cantor Fitzgerald, Morgan Stanley

The average price target between all the analysts is $12.93 which is 123% upside from the current stock price of $5.80

Here is what some analysts say about SmartRent:

February 15th: Morgan Stanley analyst Erik Woodring initiated coverage of SmartRent with an Equal Weight rating and $9 price target. The company is a "first mover in the early days of disrupting" a $30B real estate internet of things market where technology is becoming more important in driving operating efficiencies, Woodring tells investors in a research note. He believes SmartRent's enterprise smart building technology is poised to benefit from the fast growing adoption of smart and connected home solutions in the U.S. residential rental market. However, Woodring sees limited upside from current valuation levels.

February 14th: Keefe Bruyette analyst Ryan Tomasello initiated coverage of SmartRent with an Outperform rating and $13 price target. The expanding landscape of public real estate technology companies offers exposure to "various secular themes tethered to the digitization of real estate - the world's largest asset class," Tomasello tells investors in a research note. The analyst is bullish on technology adoption across the anachronistic industry, but says "idiosyncratic risks coupled with an unforgiving macro backdrop for high-growth, low-profitability stories warrant a selective approach." He favors companies with "defensible competitive moats" where he has "strong conviction" in profitability and management execution.

The upcoming Q4 earnings report on March 24, 2022 might bring the attention of more analysts, and those that already cover the company will probably reiterate their ratings and update the price targets. Perhaps if the numbers are strong enough the two firms with HOLD ratings will upgrade to BUY.

TECHNICALS:

As I stated in the introduction section, the technicals are pretty ugly, $SMRT has clearly been in a downtrend since November. As you can see from the bottom line of this channel, the stock has bounced off this support multiple times which makes me think we might be destined to bounce off it again in the $5.00 range before earnings on the 24th of this month.

If $SMRT continues to go lower but bounces off this bottom line in the next week it’s very possible that I start a small position. If $SMRT continues to go lower and fails to bounce off this trendline then I’m definitely not starting a position.

As long as $SMRT beats the Q4 estimates of $31.4M and gives 2022 guidance of $300M+ then the stock is probably close to a bottom at these prices.

$SMRT is below all of the moving averages so any trader would tell you to stay away until there’s a base or uptrend, however I’m still a long term investor that doesn’t mind buying beaten down stocks that could still provide meaningful returns over the next few years. I’m not sure if I would have had interest in SmartRent at $14 in November but now that the stock has fallen 60% in the past 3-4 months, it’s certainly got me intrigued.

CONCLUSION:

If you believe the current estimates from the analysts, it means SmartRent is only trading at 6x 2024 net income yet over this same time frame they are expected to grow revenues by 10x.

SmartRent is one of those companies that is losing money now (which is not ideal in this macro environment with rates going higher) but if you can be patient for a couple years and believe in the growth story going forward then it’s very possible you’ll be rewarded for accumulating shares under $6.00 which is probably what I’ll end up doing very soon.

I also find SmartRent very compelling because of their investor base which becomes very strategic in the world of real estate technology. If you’re trying to sell hardware and software solutions to companies that are also your largest shareholders, those deals become much easier to get done.

For anyone that has lived in apartment/condo buildings for the past 5+ years, you’ve witnessed first hand how these buildings have been upgrading everything from their door locks to temperature control systems to building/amenity access and everything else in between.

When I was looking at apartment buildings in Boston a few months ago, during my tours each one of the leasing agents put significant emphasis on the technology upgrades they had made over the past year to make the residents life easier and more seamless. It’s impressive how many things can now be done from our smart phones with the click of a few buttons.

Even though I’ve been focusing on slightly larger companies in my recent writeups ($5-20 billion market caps) — I simply found SmartRent too interesting to ignore. I will continue to follow this company closely and perhaps even start a position in the next couple weeks. It’s very possible the stock has gotten hammered lately because it’s just another “unprofitable” SPAC however that might present a great opportunity for long term investors.

I will do my best to setup an interview with the CEO (Lucas) in the coming weeks, probably after they report earnings so he’ll be able to speak more freely with me.

I hope you enjoyed this writeup, as always if you have any thoughts or comments feel free to reach out. SmartRent is still a new company for me and I’m trying to learn as much as I can about them in order to determine if this is a stock I want to own.

Regards,

Jonah Lupton

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.