Paid subscribers to Jonah’s Growth Stock Deep Dives receive:

2-3 deep dives per month (8,000+ words)

1-2 mini deep dives per month (2,500+ words)

15-20 quarterly earnings writeups (2,000+ words)

Investment models for 20+ holdings (updated quarterly)

Investment portfolio spreadsheet with all of my core holdings, non-core holdings, swing trades and hedges

Investment portfolio spreadsheet also contains real-time activity (buys, sells, adds, trims) plus real-time notes/commentary/charts throughout the day

My investment portfolio is up +224.4% in 2024, after being up +134.7% in 2023, now up more than 3,000% since January 2020 when I got back into investing full-time.

Here’s my investment strategy which focuses on high-quality growth stocks… I own 15-20 core holdings (great fundamentals, compelling valuation) plus another 5-10 non-core holdings (good fundamentals, reasonable valuation) plus another 5-10 swing trades (good fundamentals, reasonable valuation, compelling technicals).

As long as the fundamentals remain strong and valuation remains compelling/reasonable, then I’ll add on pullbacks.

I only want to own stocks that have at least 50% upside within the next 1-2 years and at least 100% upside within the next 3-4 years.

My objective is to maximize the upside in good markets and minimize the downside in bad markets. I accomplish this by being very selective with my stock picking and disciplined on valuations while using a variety of hedging strategies to protect my gains in market downturns.

Hosting my next webinar with TrendSpider on Monday, August 26th at 4:30pm EST: https://us06web.zoom.us/webinar/register/WN_CD5-LhCOQRePVsbOs_n-Ow#/registration

When I’m looking for the best swing trading setups, there are 7 specific setups that I’m focused on:

breakouts

consolidation / pre-breakouts

gap ups

retests after breakout

reclaim 50d

reclaim 200d

reclaim AVWAP from 52 week high

We’ll go through 5, 6 and 7 in this webinar. I’ll also talk about which stocks I’m focused on after earnings season and where we could see some big multiple expansion over then next few weeks.

Register at: https://us06web.zoom.us/webinar/register/WN_CD5-LhCOQRePVsbOs_n-Ow#/registration

TTD Q2 earnings report: https://investors.thetradedesk.com/news-events/news-details/2024/The-Trade-Desk-Reports-Second-Quarter-2024-Financial-Results/default.aspx

TTD Q2 earnings webcast: https://events.q4inc.com/attendee/914853387

TTD Q2 earnings transcript: https://s29.q4cdn.com/168520777/files/doc_earnings/2024/q2/transcript/The-Trade-Desk-Second-Quarter-2024-Conference-Call-Prepared-Remarks.pdf

TTD Q2 earnings presentation: https://s29.q4cdn.com/168520777/files/doc_earnings/2024/q2/presentation/TheTradeDesk_Q224_Investor_Presentation.pdf

TTD Q2 10-Q: https://s29.q4cdn.com/168520777/files/doc_financials/2024/q2/c0e57635-94c8-4559-98b6-97a70d27aff4.pdf

Introduction

The Trade Desk is a leading Demand-Side Platform (DSP) for digital programmatic advertising (adtech). The company partners with various content owners, particularly those with premium content, who want to monetize their content.

The Trade Desk is not a destination (sell-side), meaning those content owners do not sell their ad inventory through the Trade Desk platform. Instead, the Trade Desk is on the buy side, buying ads on behalf of the biggest brands in the world, who are its customers.

The Trade Desk has long advocated for the Open Internet, an alternative to large, so-called walled gardens like Google and Meta. These walled gardens have built fantastic advertising businesses in the last two decades by keeping most internet users within their closed walls and having first-party data on them.

However, there has been a massive shift in recent years in where consumers spend their time online. Prior to the pandemic, more than 60% of the time was spent within walled gardens (e.g., YouTube and Facebook/Instagram) with the other 40% spent on the Open Internet. That has completely reversed since then, largely because of the shift to emerging premium Open Internet channels such as Connected TV (CTV) and digital audio. Companies like Disney, Netflix, Roku, FOX, NBC (with the Olympics content), Spotify, and many others are increasingly taking market share of time spent consuming content either online, through smart TVs and streaming devices.

At the same time, more and more people ditch linear TV in favor of streaming TV, which has been reshaping the TV advertising space. According to industry research, CTV ads will outgrow linear TV ads by 2030 in the US.

This massive $230+ billion opportunity is rapidly moving online and TTD has already built the largest CTV inventory marketplace, giving advertisers unmatched access to premium content across major networks and ad-supported streaming services worldwide.

Apart from CTV, the company also operates in the retail media space, providing advertisers with a link between ad spend and customer purchases, particularly in brick-and-mortar. The world's leading retailers and commerce data companies are partnering with TTD.

The Trade Desk platform recently underwent a major upgrade with the introduction of Kokai, which allows advertisers to deploy their first-party data about their most loyal customers and then use that data as a seed to find new audiences across the many thousands of destinations that TTD partners with. Kokai uses AI to analyze roughly 15 million ad opportunities every second and the hundreds of variables associated with each one of them.

Those campaigns that have moved from the previous version of the platform, Solimar, have seen incremental reach go up more than 70%, while cost per acquisition has improved by about 27%. Kokai will lead the next growth for the Trade Desk.

Out of the 20+ core and non-core holdings in my investment portfolio, I think it’s possible that TTD has the least upside over the next few years because the valuation is already slightly rich however they are the leader in their industry, they have a great management team and they also have tremendous tailwinds from everything mentioned above plus they’ve recently partnered with Netflix and Disney+ to help monetize their ad-supported tiers. I’m not adding to my TTD position at these prices but I would in the $80s.

The most significant risk to TTD over the next 12-18 months would be a severe recession where companies cut back on their ad buying/spending. This will be something to watch closely.

As you can see from this chart below, TTD dropped -65% from the 2021 highs to the 2022 lows but has since bounced +170% and now sits less than 10% away from all time highs.

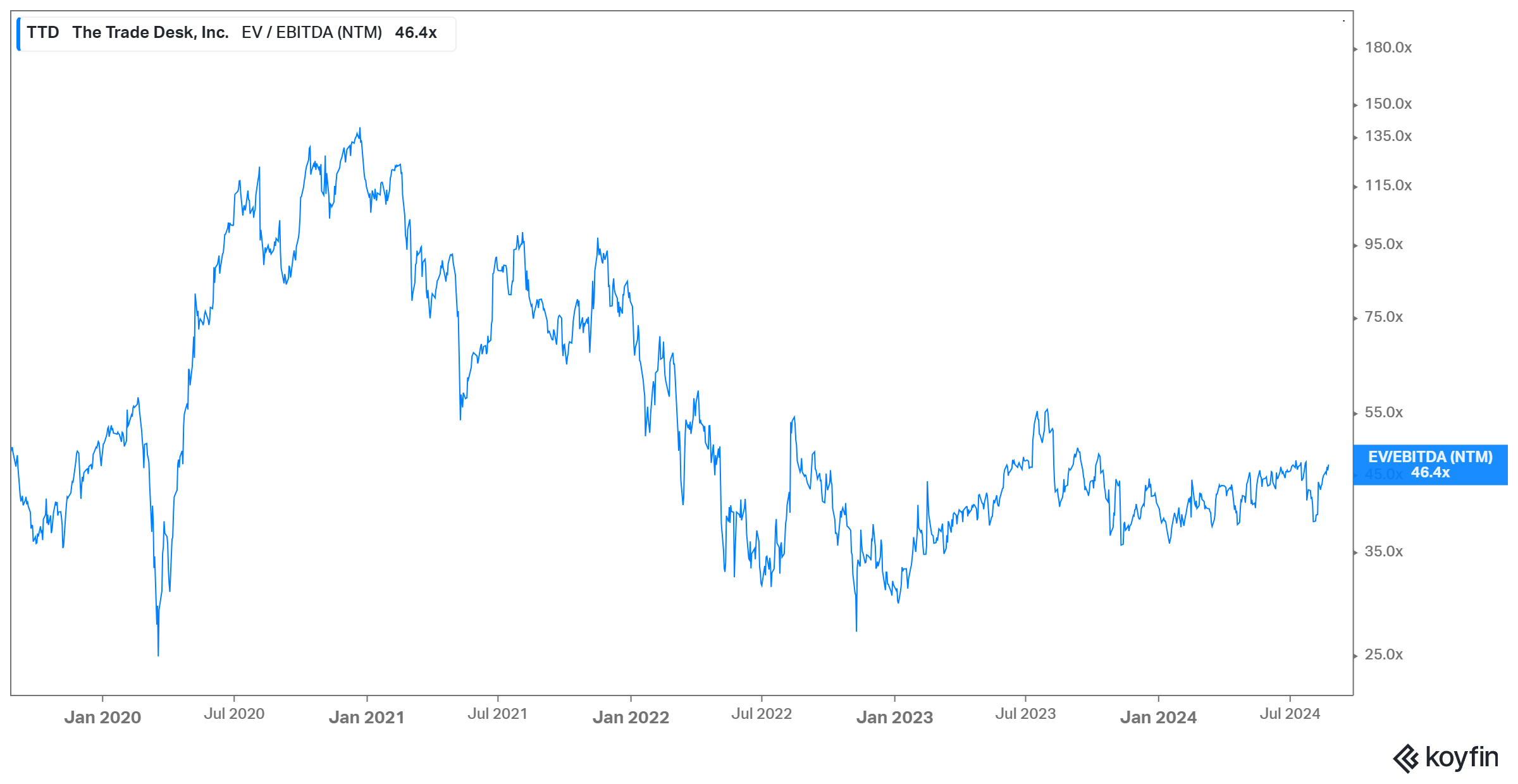

In terms of valuation, TTD is still trading at approx 46x NTM EV/EBITDA and 38x NTM EV/EBITDA which certainly looks cheaper than a few years ago but still quite rich when you consider that EBITDA might only grow at 25-30% for the next few years. This is why I think TTD has the least amount of upside over the next few years of all my core and non-core holdings. TTD is a great company but valuation is not very compelling at these prices.