Update on $CELH (Celsius Holdings)

In full disclosure $CELH (aka Celsius Holdings) is still one of my largest positions as I remain extremely bullish on the company after they reported outstanding 2021 Q1 earnings this past Thursday morning (May 13th).

Website: Celsius.com

2021 Q1 earnings report [click here]

2021 Q1 earnings call [click here]

2021 Q1 earnings call transcript [click here]

My writeup on $CELH from mid-March when the stock was $46.00 https://jonahlupton.substack.com/p/celh-celsius

My mid-March interview with John Fieldly, CEO of $CELH

OVERVIEW:

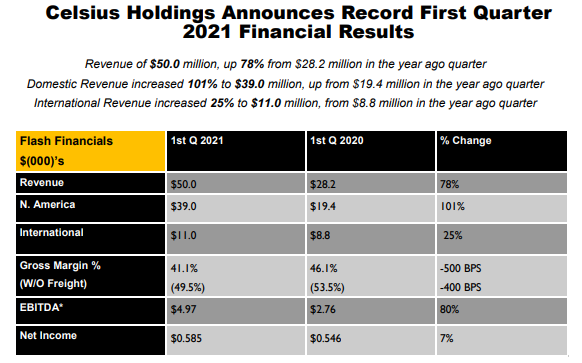

$CELH reported Q1 revenues of $50.0 million which was up 78.2% YoY from 2020 Q1 (aka year over year) and up 40% QoQ from 2020 Q4 (aka quarter over quarter).

US revenues were up 101% YoY while International revenues were up 25% YoY.

Revenue growth in the brick & mortar channel was up 137% YoY (this is where the company is currently focused most heavily so I fully expected to see YoY growth stay very strong for the foreseeable future.

$CELH announced that they have increased their retail authorization count from 82,000 locations at the end of 2020 to 92,000 locations at the end of 2021 Q1. John Fieldly (CEO of $CELH) said he fully expects to surpass 100,000 locations by end of 2021.

$CELH announced that DSD partners have increased from 150 as of 2020 Q4 to 180 as of 2021 Q1. If you remember from my writeup in mid-March I explained that $CELH was in the middle of transitioning from DTR (direct to retailer) to DSD (direct store delivery). DTR means $CELH is shipping product to the retailers warehouses or distribution centers, then it gets shipped from there to the stores and then the employees have to stock the shelves (this is riddled with problems, delays, mistakes and inefficiencies). DSD means $CELH is using well established regional distribution partners to deliver product directly to the stores and stock the shelves, make sure pricing is correct, make sure displays are correct, make sure nothing is out of stock. $CELH is now big enough where DSD partners want to work with them because there’s strong demand in the market and sales velocity is increasing. This is how the DSD partners make money too.

MARKETING:

$CELH continues to roll out thousands of branded coolers into prime retail locations which is mostly your “grab & go” customer. These locations would include convenience stores, gas stations, drug stores, grocery stores, gyms, etc. — more than 50% of energy drink sales come through these types of brick and mortar locations and typically customers want them cold, not off a shelf, which means branded coolers add significant branding and sales velocity.

BRANDING:

$CELH continues to bring on my influencers and ambassadors in both sports, lifestyle and fitness…

FINANCIALS:

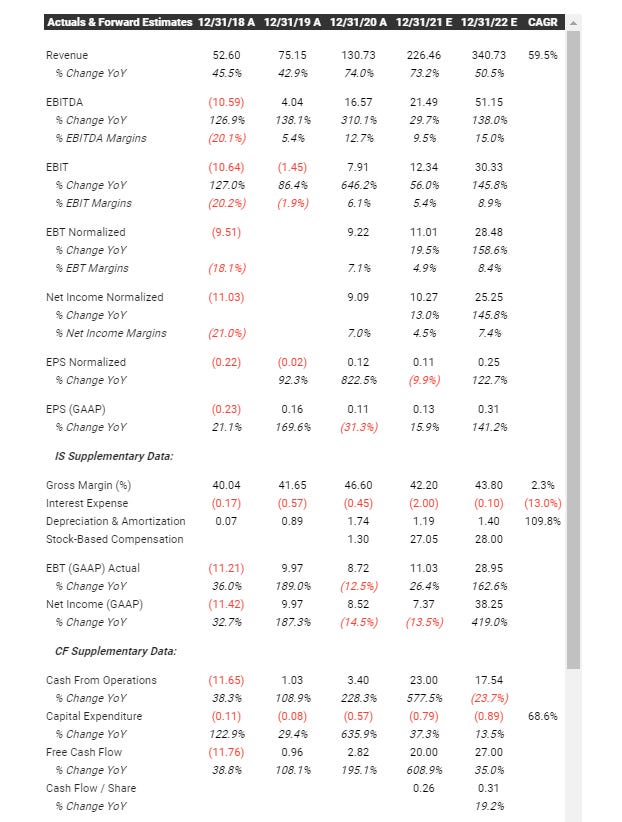

$CELH didn’t give any full year 2021 guidance for us to work with so we’re on our own to come up with some numbers.

We already know that $CELH grew revenues 40% QoQ (from 2020 Q4 to 2021 Q1) so it’s possible they do that again although I’ll be a little more conservative. TBH there are plenty of reasons to believe that $CELH could post 40% QoQ growth again because we’re now going into the warmer months when energy drink sales start increasing and we know that $CELH is now authorized in 92,000+ stores with 180+ DSD partners. However the chart below shows that full year 2021 revenue numbers would like like if we assuming QoQ growth from 10% up to 30%.

Currently the analysts that cover $CELH have 2021 revenues at $226 million (although Yahoo Finance is still showing $206 million). I’m pretty sure my 4 year old niece could figure out that $206 million for 2021 is a joke and even $226 million is probably way too low. Looking at the chart below, seeing how the business accelerated over the past 3 months, knowing how many retail stores are now adding $CELH to their spring planograms, etc makes me think there’s no way $CELH does less than $250 million in 2021 and I think $268+ million is very likely. If we see strong contributions from international channels/partners then $300 million could be possible. Either way it’s going to be a fun year for $CELH shareholders as we watch this story continue to unfold.

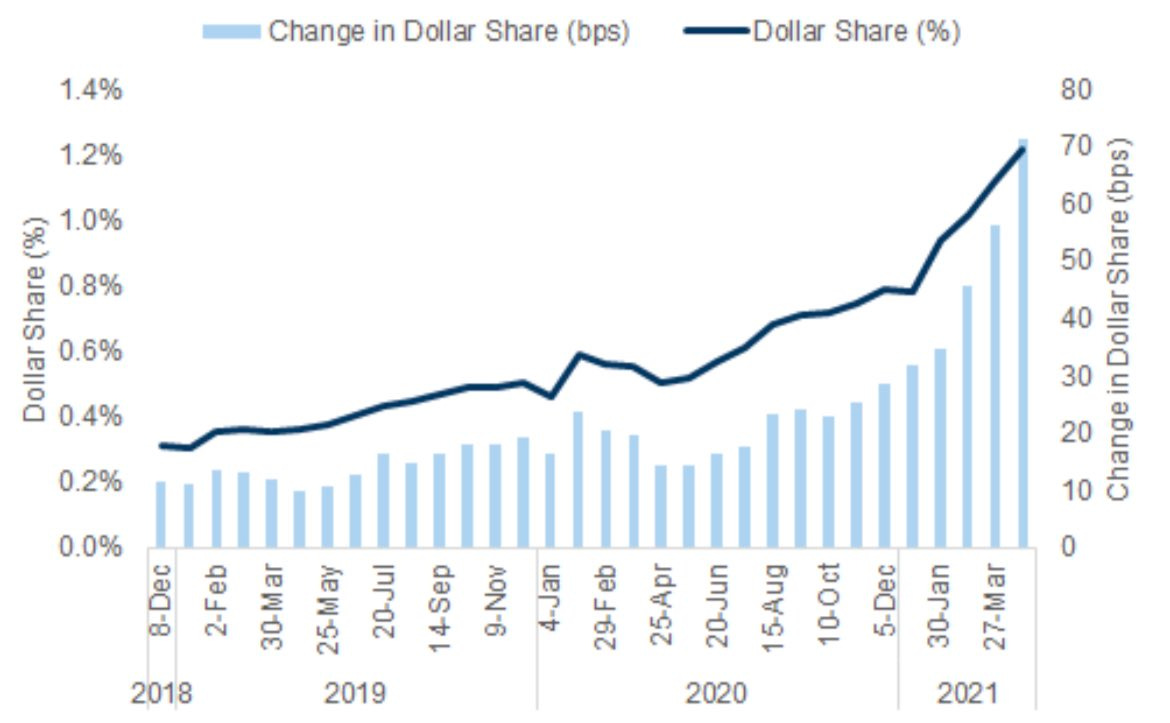

MARKET SHARE:

$CELH now has 1.2% market share which is way behind other brands like Monster, Red Bull and BANG however it shows how much opportunity is still in front of them. Don’t forget the energy drink market is valued at $60+ billion per year and growing at 8-10% annually. I think there’s a chance that $CELH can get to 3-4% in 5 -6 years when the global market is expected to surpass $100+ billion per year.

John Fieldly also shared with us on the earnings call that $CELH is still the #2 best selling energy drink brand on Amazon (behind Monster but ahead of Red Bull). It’s pretty incredible that Red Bull will probably do $6-7 billion in revenues this year yet $CELH is outselling them on Amazon. It’s possible we see online sales begin to tick down as the company expands into more retail locations but I’m fine with that.

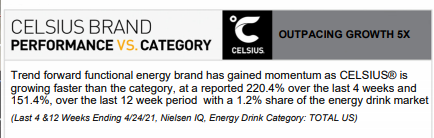

If there’s only one data point you remember from this writeup it’s the image below that talks about the recent Nielsen scan data.

Over the past 4 weeks ending April 24th (which is part of Q2 numbers), $CELH can scans are up 220.4% — this is freaking wild. There’s no way this data doesn’t carry over into strong Q2 earnings so when I said that 40% QoQ growth was always possible, this is what makes me think that. TBH when you see 220% scan data it makes me think $60+ million for Q2 should be a slam dunk and we could be looking at something closer to $65-70 million.

I’ve listened to the Q1 earnings call three times and the only negative comments are around the can shortages which are plaguing the entire industry. $CELH is not the only company dealing with this issue. John Fieldly sounds to be on top of the problem and doing a great job of managing through this short term supply constraint but it’s still something to be mindful of and whether or not it could impact Q2 numbers.

CHARTS:

$CELH is now trading above all three of the 50 day moving averages

ANALYSTS:

The analyst from B.Riley that covers $CELH reiterated their BUY rating and raised their price target from $74 to $92

SHORT INTEREST:

$CELH still has short interest in the 8-10% range so it’s very possible they’ll want to start covering those short positions as $CELH moves higher on the back of this very strong Q1 earnings report due to obvious acceleration in the business.

CONCLUSION:

Like I said above, the only problem from 2021 Q1 for $CELH is the aluminum can shortage, otherwise the company is crushing it and executing extremely well. 40% QoQ growth is incredible and knowing the recent Nielsen scan data plus 92,000+ locations plus 180+ DSD partners plus better growth from international markets = a growth story that is very much alive and still in the early innings.

It’s hard to come up with a fair valuation for $CELH, partly because the company has not issued any 2021 guidance (I don’t blame them) and partly because they are growing 7-8x faster than Red Bull and Monster which makes it hard to come up with some valuation comps.

Before I wrap up, let me compare $MNST valuation to $CELH valuation:

$MNST current enterprise value (EV) is $46.5 billion with projected revenues of $5.3 billion means $MST is trading at 8.8x EV/Sales with 16% YoY revenue growth

$CELH current enterprise value (EV) is $3.8 billion with projected revenues of $268 million (assuming 20% QoQ growth) means $CELH is trading at 14x EV/Sales with 106% YoY growth (because they did $130 million in 2020)

I know a lot of the naysayers argue that $CELH is expensive but I’m pretty sure my last bullet point contradicts that argument. Obviously there’s no guarantee that $CELH does $268 million in revenues this year but even if they only do $250 million the stock is still trading at just 15x EV/Sales with 92% YoY revenue growth and a $60+ billion TAM that is dominated by two major players of which are losing market share to $CELH.

Looking at both valuations, I would still argue that $CELH is undervalued while $MNST is overvalued. I wonder at what point some of those $MNST shareholders realize the growth days are in the past and decide to jump on the $CELH bandwagon where the growth still has a long ways to go.

I hope this update was helpful. I’m planning to send out my $DMTK update later today and my $ATER (formerly $MWK) update tomorrow morning.

Please enjoy the rest of your weekend.