Update on $DM (Desktop Metal)

Update on $DM (Desktop Metal)

INTRODUCTION:

$DM has become one of my favorite companies and largest positions — the more time I spend researching 3D printing and additive manufacturing the more bullish I become on where this market is headed. There will be multiple winners in this industry but I expect $DM to be the leader.

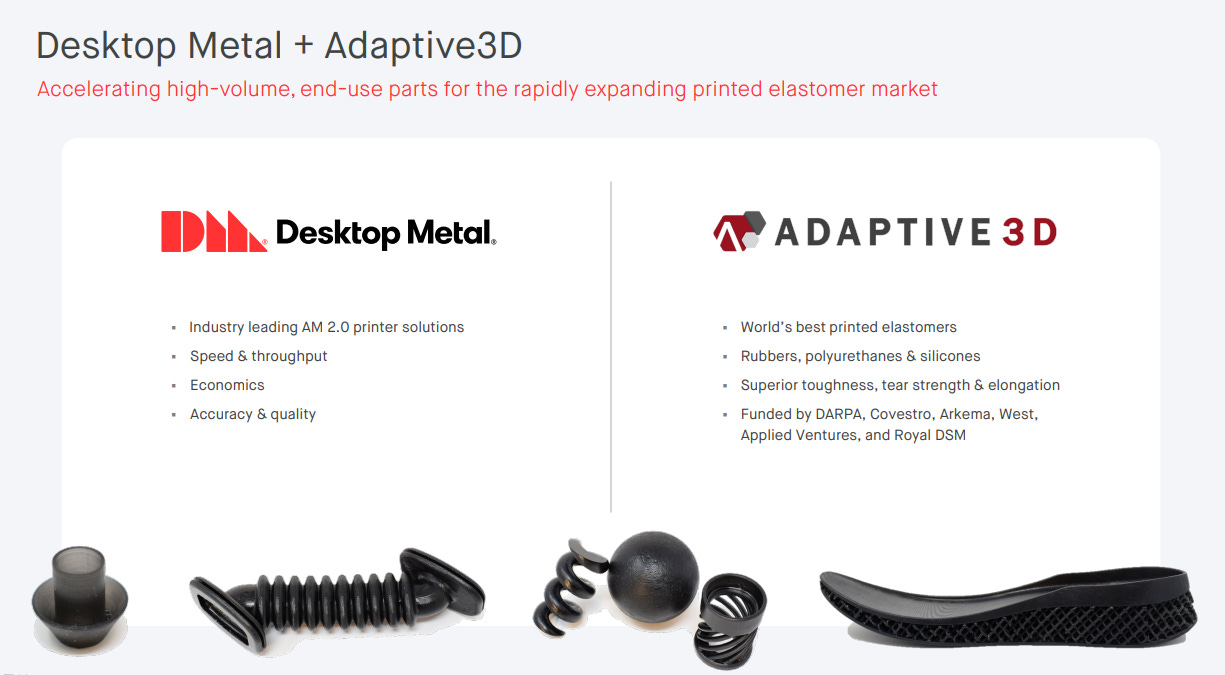

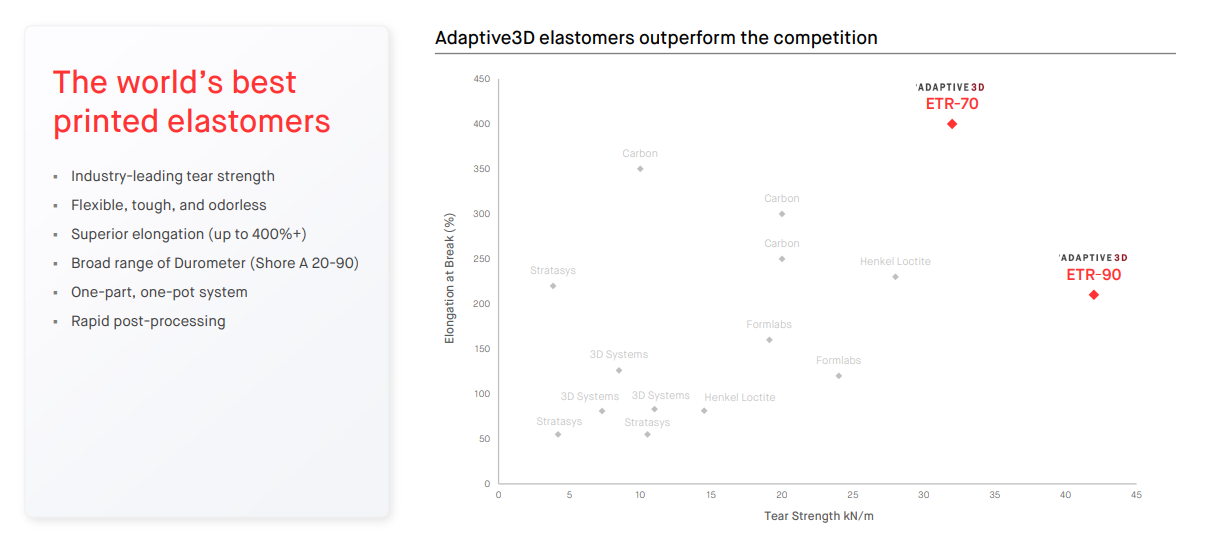

As we saw with yesterday’s Q1 earnings release (which looked fine), $DM did another acquisition — this time acquiring a company called Adaptive3D, a leading provider of elastomeric solutions for additive manufacturing [click here].

This acqusition comes just a few months after acquiring EnvisionTEC, a leading provider of polymer solutions for additive manufacturing [click here].

As I posted on Twitter last night, $DM is building the foundation for what will become a massive company by the end of this decade. I still believe $DM has the potential to reach a $70-80 billion market cap by 2030 which would be approximately 25x higher from current prices.

In full disclosure, I increased my $DM position yesterday after hours and again this morning pre-market by a total of 25% at $12.00 per share (stock was down 11-12%). As I began writing this update the markets opened and $DM began to recover. The stock traded as high as $13.65 this morning and is now around $13.25 as I’m sending this out.

I have no problem continuing to build my position at these prices. Some of the smartest investors on the planet believe that additive manufacturing will be a $146+ billion industry by the end of this decade and there’s no reason why $DM can’t own 10% of this market.

Stock price: $12.15 (as of pre-market trading on May 18th)

Website: DesktopMetal.com

Here’s my $DM writeup from May 4th: https://jonahlupton.substack.com/p/dm-desktop-metal

2021 Q1 Earnings Report [click here]

2021 Q1 Earnings Call [click here]

2021 Q1 Earnings Call Investor Presentation [click here]

$DM acquires Adaptive3D [click here]

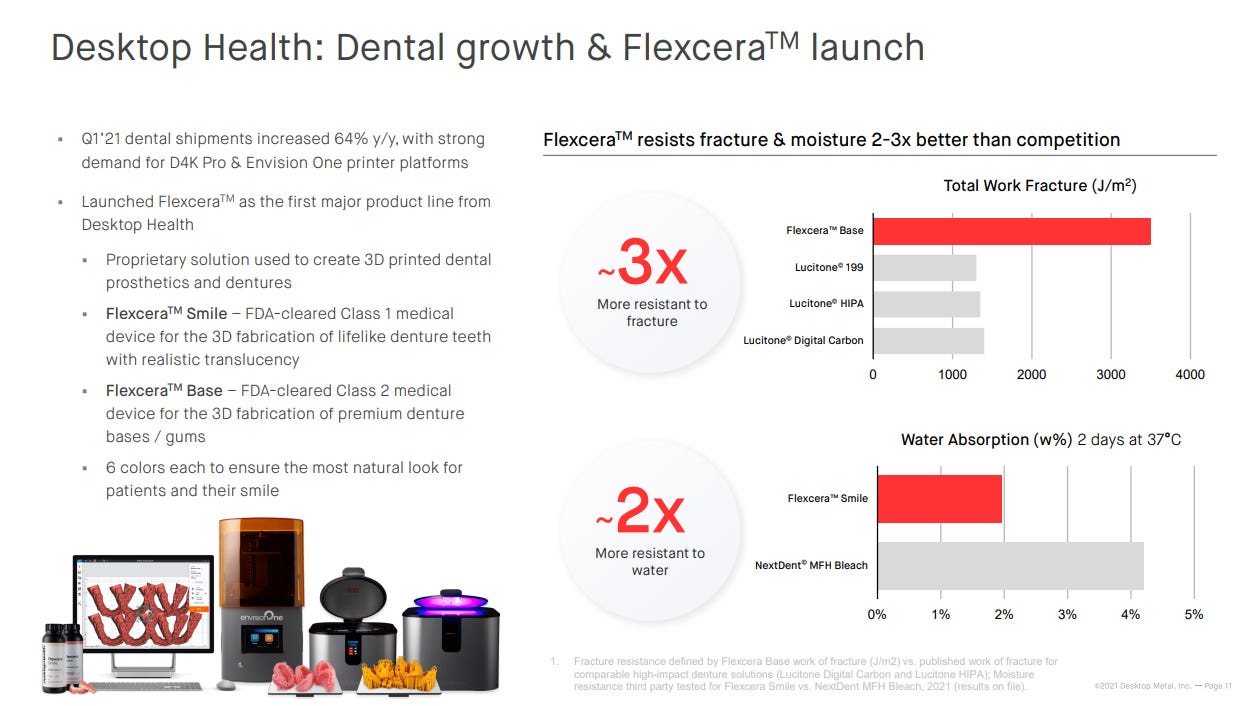

$DM receives FDA clearance for Flexcera [click here]

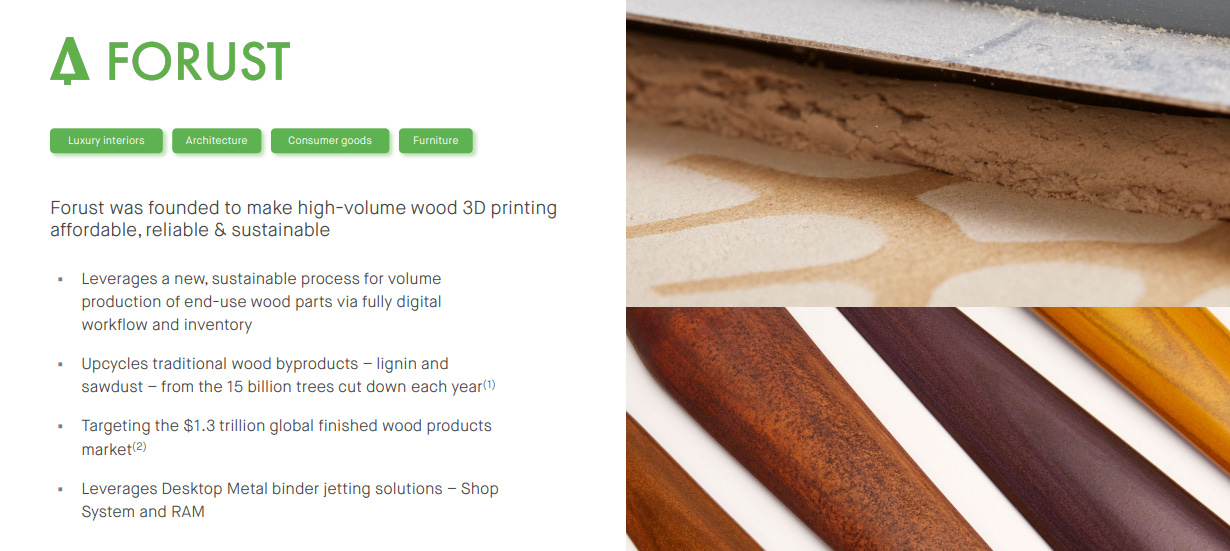

$DM launches Forust for 3D printed wood [click here]

$DM launches Desktop Health [click here]

Form 10-Q, filed May 17th [click here]

Q1 EARNINGS:

$DM reported yesterday after the close that Q1 revenues came in at $11.3 million which was ahead of estimates and represents 35% QoQ growth (from 2020 Q4) and 234% YoY growth (from 2020 Q1).

$DM reported -$19.4 million of EBITDA which doesn’t concern me. This company is in the early days of hypergrowth so I fully expect them to lose money for the next few years as they are accelerating revenues, building the team, making acquisitions, spending on sales & marketing, spending on research & development, and so forth. $DM currently has $572.2 million of cash on the balance sheet so there’s definitely no liquidity concerns. This is why it made so much sense for $DM to come public last year via SPAC with the $275 million PIPE — it gave them the runway to grow this company into a beast without having to worry about short term losses.

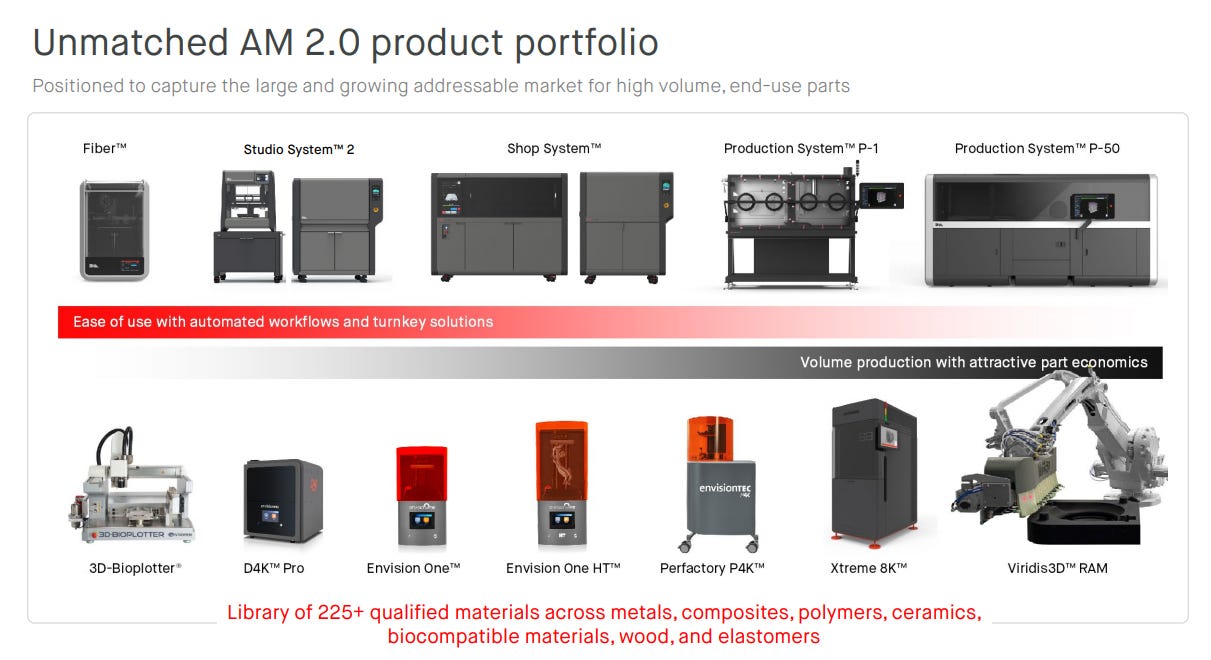

The most exciting part of the Q1 earnings report is that $DM has expanded their materials portfolio to 225 materials across metals, composites, polymers, ceramics, biocompatible materials, wood and now elastomers.

In case you missed it, $DM announced a couple weeks ago the launch of Forust, which is 3D printed wood [click here]. I highly suggest you check out the Forust website to learn more because they are literally creating 3D printed wood parts and products out of sawdust.

The last few months have been busy for $DM in terms of deals, announcements, launches and approvals.

They closed the deal with EnvisionTEC for 3D printing polymers.

$DM launched Flexcera for 3D printing dentures [watch here]

$DM launched Forust for 3D printing wood parts/products.

$DM acquired Adaptive3D for 3D printing elastomers and rubber materials.

$DM employee count has increased from 180 people in May 2020 to 470 employees as of today.

$DM reiterated their 2021 revenue guidance of $100+ million. Considering they only did $11.3 million in Q1 we should expect to see a massive acceleration in revenues over the next three quarters as you can see below.

$DM also said on the Q1 earnings call they added more customers in 2021 Q1 than all of 2020.

In my opinion, $DM should do at least $200 million in revenues next year (2022) with a shot at $250 million given these recent acquisitions of EnvisionTEC and Adaptive3D plus the launches of Flexcera and Forust which means $DM might only be trading at 10-12x 2022 EV/Sales which is way too cheap for a company with this much hypergrowth potential.

I’m convinced the investors that were selling post-earnings don’t truly understand this company, the industry or the massive upcoming transition to additive manufacturing from some of the largest manufacturers on the planet. I understand that many investors are not as patient as me and aren’t willing to think longer term but that’s just fine because I’m happy to ignore the short term noise and stay bullish given where I think $DM could be trading in 4-5 years.

Given that my original writeup on $DM was just a few weeks ago there’s no reason for me to regurgitate everything I already said so I would suggest you go back and read it again in order to fully understand what $DM does and why I’m so bullish.

I don’t deny that 3D printing is becoming a competitive market however $DM has:

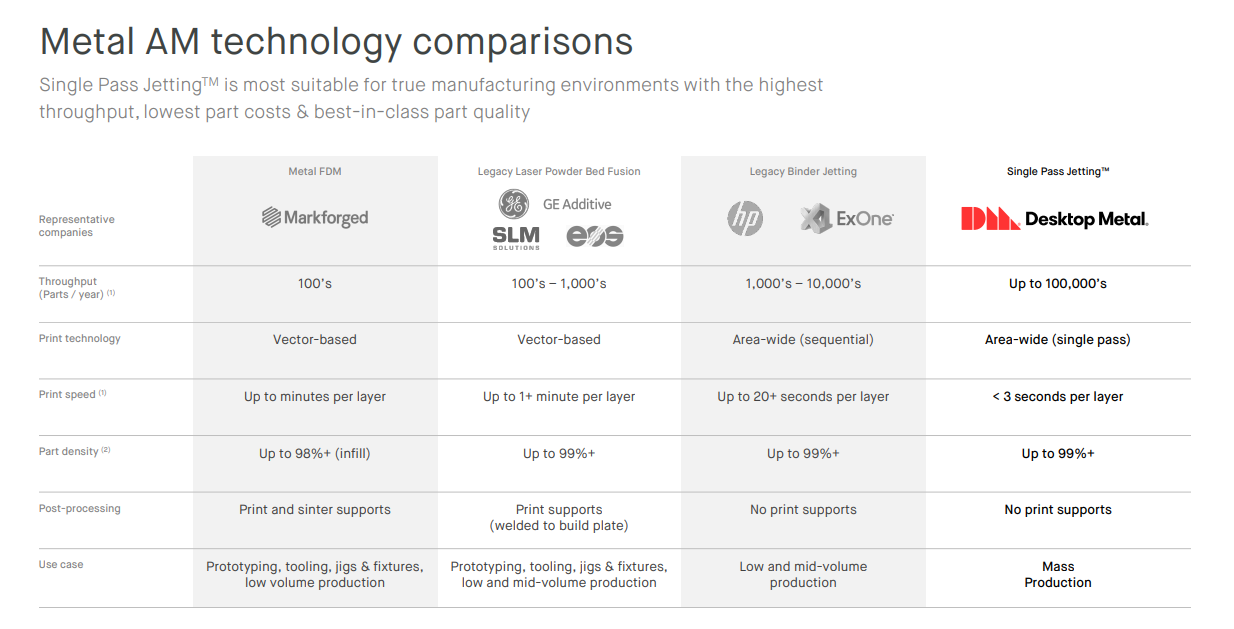

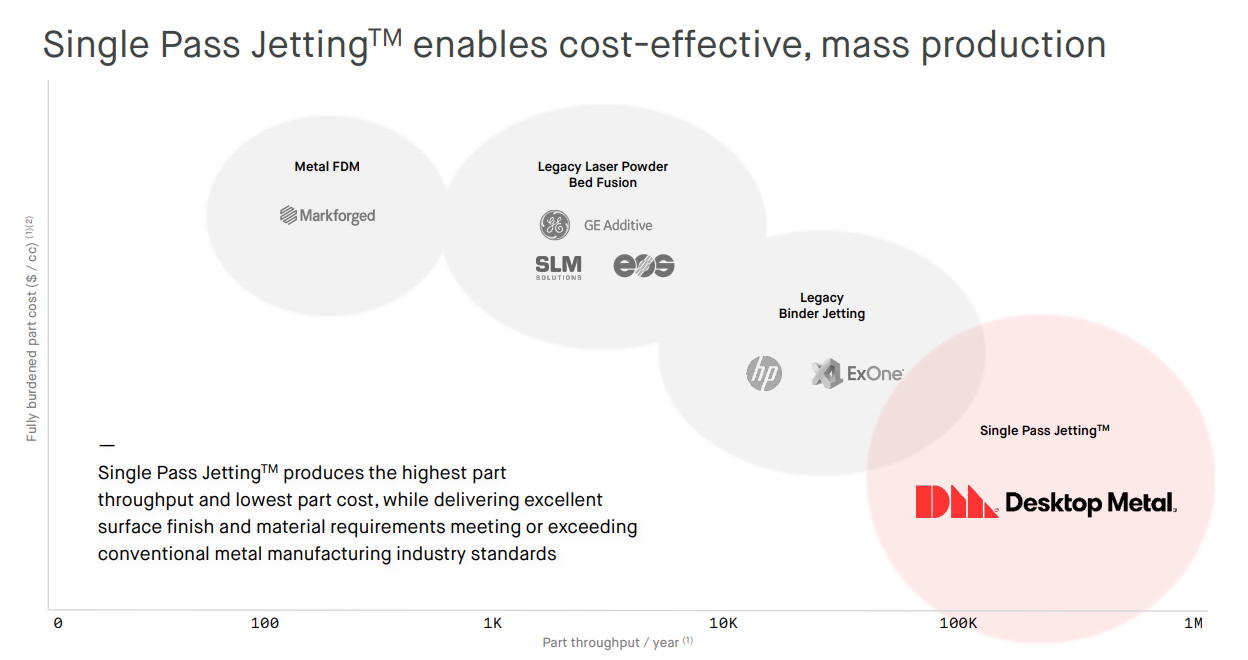

The best high-volume DLP (digital light processing) printers and the most diverse portfolio of materials (225+ and counting)…

The best and fastest high-volume printers on the planet…

The strongest IP portfolio of issued and pending patents… [click here]

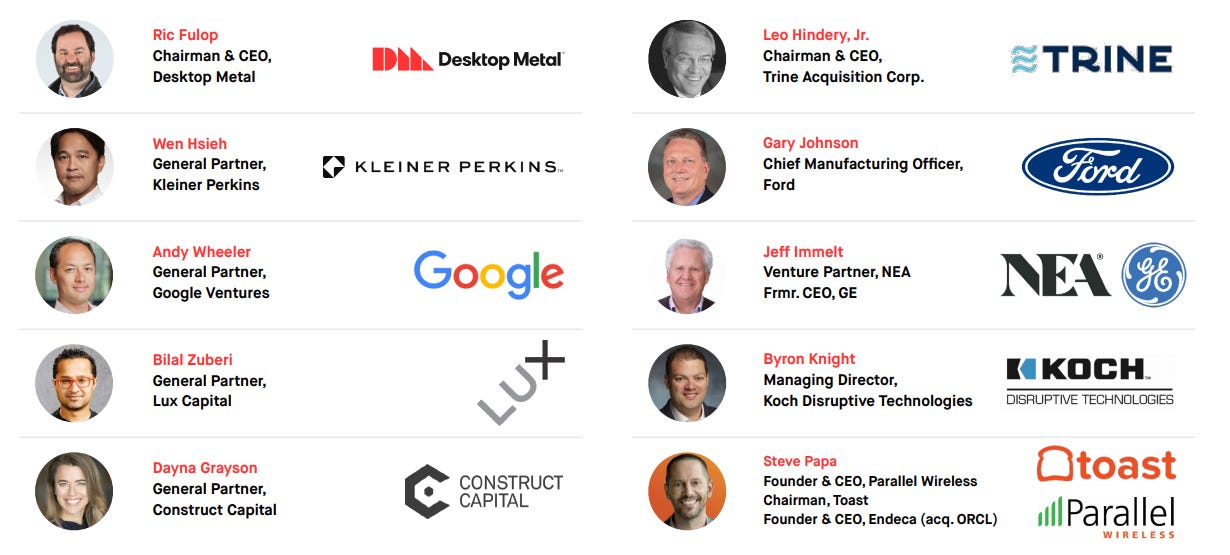

The best management team and dozens of the best early investors, strategic investors and PIPE investors…

Growing list of global manufacturing customers…

CONCLUSION:

I remain bullish on $DM in the short term but more importantly the long term. In order to have conviction in companies like $DM you need to have an investment thesis about the industry and be able to justify why you think your company has a chance to be the leader in that industry. For all the reasons I mentioned above, I believe $DM will be the eventual winner in additive manufacturing over the next decade. They are building a robust product/printer portfolio, materials portfolio and patent portfolio. These three factors put them in the strongest position to deliver the best financial metrics and thus shareholder returns.

High-volume, cost-effective, energy-efficient additive manufacturing just makes too much sense in my mind for this industry not to expand exponentially. Why would large companies like Ford, General Motors, Boeing, Koch, General Electric, BMW and so forth want to keep using vendors to make their parts when they can bring that process in-house, lower costs, lower lead times, reduce freight costs, be more green and finally have the ability to tweak/improve designs as often as they want.

I would have been happy owning $DM if they had just stuck to metals, steel, composites, etc because I think that market opportunity is big enough but now that they’ve expanded into polymers, elastomers, dental products and wood I’m even more excited to see what the future holds for this company.

I hope you enjoyed this update on $DM — like I mentioned above, there wasn’t any reason for me to go overboard on this update since my original writeup was earlier this month. Please go back and read it and please listen to the most recent Q1 earnings call [click here] — both are packed with valuable details about $DM and their growth strategy moving forward.

The first thing that Ric Fulop (CEO of $DM) says on the call is “we’re building Desktop Metal for the long term” and that’s the mindset I have right now. I’m a long term believer in additive manufacturing and $DM so I have no intention to sell my shares anytime soon.

As always, if you have any questions about $DM please don’t hesitate to reach out.

Best regards,

Jonah Lupton