$UPST - Upstart

Follow my current portfolio at [click here]

Signup for the launch of Fintrics [click here]

Signup for the launch of Adding Alpha TV [click here]

Signup for my Stocktwits room at [click here]

Follow me on Twitter [click here]

$UPST - Upstart

Website: http://Upstart.com

Current stock price: $38.50

Market cap: $2.8 billion

2017 revenues: $57 million

2018 revenues: $99 million

2019 revenues: $164 million

2020 revenues (through Q3): $146 million

LTM revenues: $215 million

2021 revenues: N/A

# of employees: 500+

$UPST’s S-1 for Dec 2020 IPO at $20 per share [click here]

$UPST CEO testifies to Congress about benefits of AI in underwriting [click here]

$UPST CEO does interview with First Round Capital [read here] or [listen here]

$UPST’s intro video:

Upstart, or $UPST, was founded in 2012 by David Girouard (formerly with Google and Apple), Anna Couselman (Google), and Paul Gu (Thiel Fellowship). The original business model for Upstart was creating income sharing agreements [read about them here] but due to a lack of significant traction they decided to pivot into the current business model which is an AI-powered lending and underwriting platform.

Prior to going public $UPST raised $144 million over 6 rounds. Their latest funding in April valued the company at $750 million [Crunchbase]. Some of their VC investors include First Round Capital, Khosla Ventures, Third Point Ventures, Rakuten and Progressive Insurance.

Upstart is the leading AI-powered lending platform, using machine learning models with 1,600+ data points and 15 billion cells of data to accurately identify and measure credit risks. Some of the variables in the AI model include credit experience, employment history, educational background, banking transactions, cost of living and loan application interactions. This data will be a competitive advantage for $UPST going forward.

Almost all personal lending and underwriting is done using outdated credit score models, like FICO, which has been around for 30 years and has not evolved. AI models like the one from Upstart have the ability to learn and improve on it’s own over time as more loans are made, as more payments are made, as more data is gathered. AI models are the future of the credit industry and Upstart has an opportunity to lead this charge. In many ways $UPST reminds me of Lemonade ($LMND) in the way that they are disrupting the insurance industry with their AI-powered insurance products.

$UPST started with consumer loans for things like personal needs, credit card consolidation, debt consolidation, home improvement loans, medical loans, wedding loans, moving loans, etc. but has since expanded into auto loans (first auto loan was approved in 2020 Q3). Over the past few months $UPST has hinted that their AI-models could be extremely effective in other massive lending/credit markets such as mortgages, student loans, business loans and credit cards. The global credit market is more than $100 trillion which is obviously diced up into dozens of different segments but it’s very possible over the next decade that AI-powered models become the standard underwriting solution in each of them.

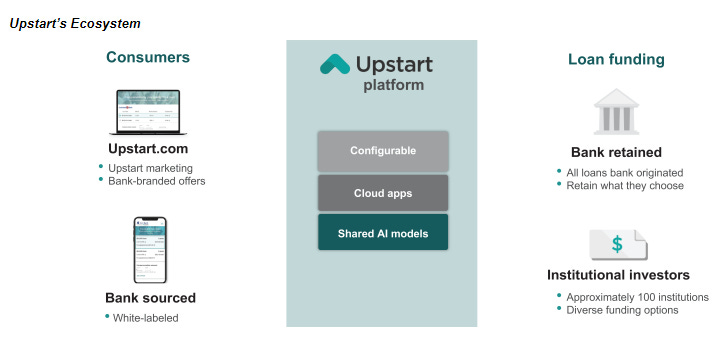

Currently $UPST has 10 bank partners and through them they make loans of $1,000 to $50,000 with interest rates ranging from 8% to 36%. $UPST provides their bank partners with a consumer facing cloud application that streamlines the end to end process of originating and servicing a loan.

Upstart’s cloud application integrates seamlessly into the bank’s existing systems. This highly customizable and scalable platform allows each bank partner to define their own credit policies and lending parameters. Since Upstart is analyzing data across all of their bank partners, it allows each of them to benefit from the sharing of information. Loans issued through Upstart’s bank partners can either be retained by the originating bank or sold to any of the 100+ institutional partners that invest in Upstart-powered loans. These 100+ institutional investors include Goldman Sachs, Jefferies, PIMCO, Western Asset Management, Morgan Stanley and JP Morgan. When $UPST first rolled out their AI-powered lending product, only 2-3% of their bank partners were keeping the loans but now that number is approaching 25% which means the other 75% are sold and distributed to their 100+ institutional investors.

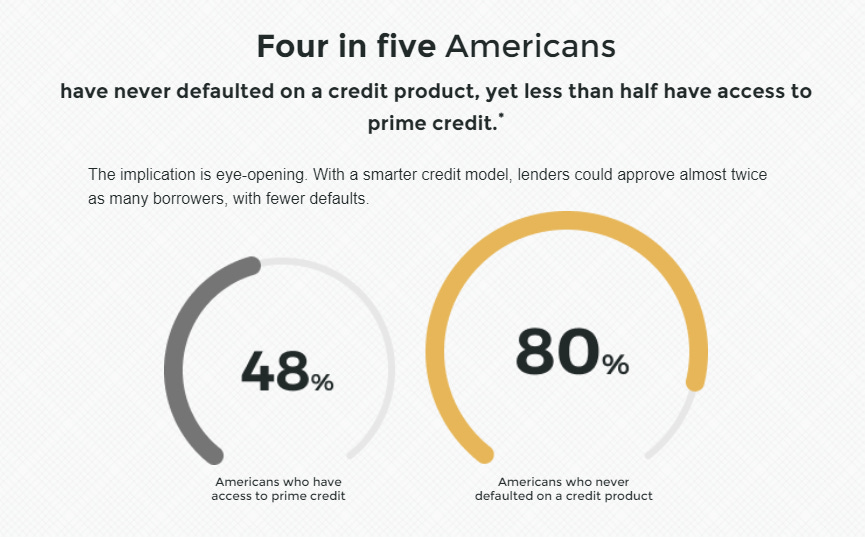

Given that $UPST’s mission statement is to enable effortless credit based on real risks, let’s dig into the numbers. In 2019, a study done by the Consumer Financial Protection Bureau found that Upstart’s AI model approves 27% more borrowers than the traditional models with a 16% lower average APR.

Additionally, in studies with several large banks, through back testing their AI-model, $UPST would have allowed those banks to approve 173% more loans without increasing the loan loss rate

Through my research I learned that 80% of American’s have never defaulted on a loan yet only 48% of American’s have access to prime credit rates. With smarter AI-powered models banks and lenders can approve 2x more loans with fewer defaults which means more revenues for bank partners with less loan losses and write-offs.

Think about this...most consumers (good borrowers) pay too much interest because they are subsidizing the losses from bad borrowers. Every loan that doesn’t default was priced too high. Every loan that does default was priced too low or should not have been approved in the first place. Lending is the perfect use case for AI because millions of credit based decisions are being made every day so the model just keeps getting smarter and smarter.

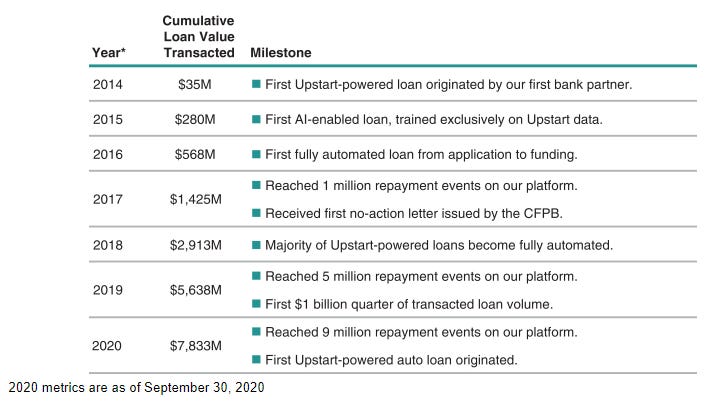

Since $UPST pivoted to this AI lending model they have transacted more than 620,000 loans that generated more than 9 million repayment events. Through the first 9 months of 2020, Upstart has facilitated 176,983 loans compared to 136,468 loans in the first 9 months of 2019. This was a 30% increase despite the drop off in consumer lending because of Covid. When the pandemic struck in Q2, banks stopped lending so Upstart’s revenues dropped 47% thanks to a 71% drop in loan originations. However their business has bounced back nicely as the credit markets began functioning properly.

Revenues for Upstart through the first 9 months of 2020 were $146.7 million which was up from $101.6 million in the first 9 months of 2019 or a 44% increase. Upstart was even profitable ($5 million) through the first 9 months of 2020. As you can see from the chart below $UPST’s revenues have increased nicely over the past few years. They definitely saw an interruption in that growth this year but I expect them to have a very strong 2021 and 2022 as the economy returns to some normalcy with trillions of dollars slushing through the financial system looking for somewhere to go.

One of the numbers that really stands out to me are the 86% gross margins which will lead to strong operating leverage in the future. In terms of how they make money off their bank partners this chart below should provide some clarity.

Another sign of the strength of $UPST’s AI-model is that despite the financial struggles that millions of Americans faced due to the pandemic, Upstart customers have proven to be more resilient with only 5.6% missed payments versus the industry average of 11.4% -- this is because Upstart is 5x more accurate at predicting financial hardships by borrowers than traditional credit score models.

Upstart gives smaller banks, community banks, regional banks and credit unions a cost effective lending solution for competing with their much larger competitors. The Net Promoter Score for Upstart’s bank partners’ lending programs is 79, well above the industry average. Upstart is also appealing to a younger demographic, the average age of an Upstart loan applicant was 28 years old. Personally I’ve been navigating the website for several days, testing out different features and everything is very easy and intuitive.

The 4 largest US banks spend an estimated $38 billion annually on technology and innovation. These banks may try to build their own AI lending models however outside of the largest 4 banks there are 5,200+ FDIC insured institutions that would be at risk of falling behind. These 5,200+ institutions hold more than $8 trillion in deposits and have outdated technology and lending solutions. It makes much more sense for these 5,200+ banks and financial institutions to just partner with $UPST rather than have to build and maintain their own AI-powered solution.

Upstart provides their bank partners a highly-automated digital experience and fully customized lending program that is especially attractive to tech-savvy borrowers. Not only does Upstart approve 27% more loans than traditional models but most borrowers are approved instantly with 99% of loans being funded within 1 business day. In addition to that, 50% of applicants are applying for these loans on their mobile phone.

Due to how quick and easy the application process is through Upstart and their bank partners, $UPST has a tremendous rating on Trustpilot. reviews. Out of 6,665 reviews $UPST has received 4.9 out of 5 stars [read here]

You can see in the chart below that 69% of loans are fully automated which means approved without the applicant needing to submit any additional paperwork or jump on the phone with anyone. I believe this number is up to 70% now as mentioned in their S-1. As you can see this number has increased dramatically since 2017 which is saving their bank partners a significant amount of money by reducing the number of “humans” needed to review and approve loans.

This chart also shows that the conversion rate from the top of the funnel to approved loan has also increased over the past few years from 8.1% to 14%. Every year US banks originate more than $3 trillion of consumer credit so just think about how much faster, easier and cheaper that process could be if AI did more of the workload.

As $UPST continues to improve their AI model and as more institutional investors want to buy these loans and as the credit rating agencies gain confidence in Upstart’s loan performance then it will lead to even cheaper and more efficient funding for all types of credit. $UPST says for every 1% reduction in the loan rate...the conversion rate from the top of their funnel to loan approval and origination will increase by 15%. This is why AI will be so important for underwriting in the future, it will keep money flowing faster and more efficiently through the system to the right borrowers while reducing risk and loan losses to the lenders.

Even though I’m excited about what $UPST is doing already in the consumer lending space with just 10 bank partners, I’m even more excited about the opportunities ahead which includes bringing on more bank partners, more affiliate partners (like Credit Karma) but most importantly is expanding into new lending markets. Even though consumer credit is very large, it’s worth noting that auto loans are 5x bigger than consumer loans but mortgages are exponentially bigger than both of them at $16+ trillion. Knowing that AI models can be 4-8x more accurate than traditional underwriting models it stands to reason that $UPST could disrupt a lot more than just consumer lending over the coming years.

The CEO of $UPST has stated when it comes to recruiting talent, they are competing against companies like Google and Uber, not the big banks. This just goes to show that the larger financial institutions are not building these types of advanced AI models and ML solutions in-house so they’ll eventually need to partner with companies like $UPST or risk falling behind like they did in the digital payments industry to companies like Square, Visa, Mastercard and Paypal. I suspect one of the challenges for large banks to being integrating solutions like $UPST is worrying about how many humans AI will replace. After doing all my research the past few days I’ve come to the conclusion that AI-powered lending and underwriting is much better than the old way of doing it however by making the switch to AI you are essentially eliminating hundreds or thousands of jobs along the way. At some point bank CEOs and Boards will just need to bite the bullet and take the heat from employees because this is the future. $UPST is focused on building one of the best AI and ML teams in the financial industry stacked with PhD’s in mathematics, statistics and computer science. The current management team appears very strong and I love that all three co-founders are still actively involved in the business.

Upstart’s marketing strategy is still being perfected but currently it includes online marketing affiliates (like Credit Karma), direct mail, organic search traffic, email marketing, online advertising and podcast advertising. I suspect some of the funds raised in the recent IPO will go into these existing sales & marketing channels to not only drive more traffic to their website and into the funnel but also to establish more bank partnerships. I would also love to see $UPST do something with the leading consumer FinTech companies like Square and PayPal.

In terms of risks with $UPST, there are several worth pointing out:

1) $UPST has significant customer concentration risk. I would like to see them expand their bank partners so no single bank partner is accounting for more than 25% of their revenues.

2) If the economy takes another tumble and the credit markets freeze up again, then revenues for companies like $UPST would also take a significant hit. In order for $UPST to make money they need their bank partners to originate the loans they are approving through their AI-model.

3) Since the IPO, $UPST rallied from the low $20s all the way up to $51 before pulling back and dropping into the low $40s. Today the stock is down 10-12%, trading between $38-39 which I believe provides an attractive entry point.

In full disclosure I began adding $UPST last week when I started doing my due diligence and have since added to that position. $UPST represents a 3% position in my portfolio.

After spending more than 12 hours this past weekend reading up on $UPST and the long term impact and benefits of AI across multiple industries I’m very bullish about the long-term prospects of $UPST assuming they can continue to gain traction in the lending industry then use their AI models to go after bigger markets like mortgages, auto loans (already doing it), student loans, credit cards and even business loans.

I almost didn’t finish this writeup on $UPST simply because I was unable to find any revenue or earnings estimates for 2021 or 2022 from the company or analysts however after doing all the due diligence and getting to understand this company and the markets they are tackling I simply thought the opportunity was too big to pass up.

I expect some choppy days ahead especially as the company looks to form a base after an IPO then works through the 6-month lockup expirations but even with those market risks I wanted all of my subscribers to be aware of this company, understand the business model, learn about the opportunities ahead and then decide for themselves whether they thought $UPST belonged in their portfolio going into 2021.

To wrap up, below are the first two pages of Upstart’s S-1 filing which I thought were very powerful in portraying the company’s mission and reasons for trying to improve the credit and lending industry.

I hope you enjoyed this write-up. My goal is to provide two in-depth write-ups per week of stocks that I find interesting and poised to deliver strong returns for investors.

Best regards,

Jonah Lupton

Disclaimer: The stocks mentioned in my newsletters are not intended to be a list of buy recommendations but rather some ideas for your watchlist. Perhaps they end up in your own portfolio after you conduct your own research and due diligence. Some of the stocks mentioned in my newsletters have smaller market capitalizations and therefore can be more volatile. I always encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizing in accordance with your own risk tolerance and investment objectives.