Deep dive on Tesla ($TSLA)

In addition to my Substack newsletter, I also run a Stocktwits room where I post my current holdings, buys & sells, investment models, technical analysis and market commentary for both my Investment Portfolio (long term, strong fundamentals, 20-30 holdings) and my Trading Portfolio (short term, strong technicals, 0-10 holdings). The two options are $15/month for the monthly plan [click here] or $150/year for the annual plan [click here].

You can now signup for my new Substack called Jonah’s Trading Charts which is focused exclusively on the technicals — every day (usually pre-market) I’ll send out an email with my favorite trading charts/setups. You’ll also have access to my trading portfolio with current positions/sizes, entry/exit prices, profits/losses and much more. I’m also doing live charting and live trading 3-4 times per week.

Company: Tesla

Ticker: (TSLA)

Website: Tesla.com

IPO date: June 29, 2010

IPO price: $17.00

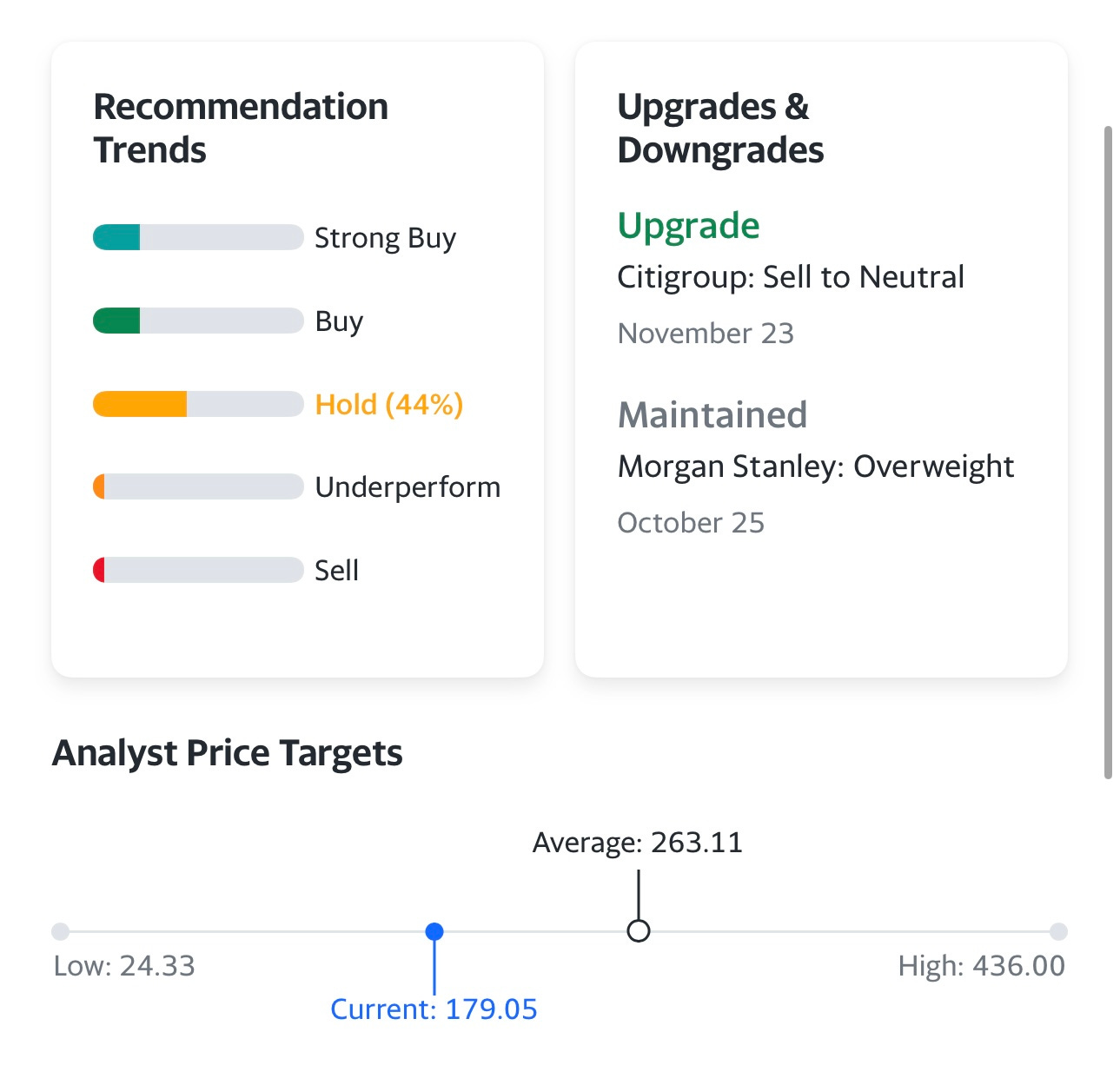

Current stock price: $179.05

Outstanding shares: 3.16 billion

52 week high: $402.67 on January 04, 2022

52 week low: $166.18 on November 22, 2022

Market cap: $565 billion

Enterprise value: $551 billion

Headquarters: Austin, Texas, United States

Number of employees: 100,000+

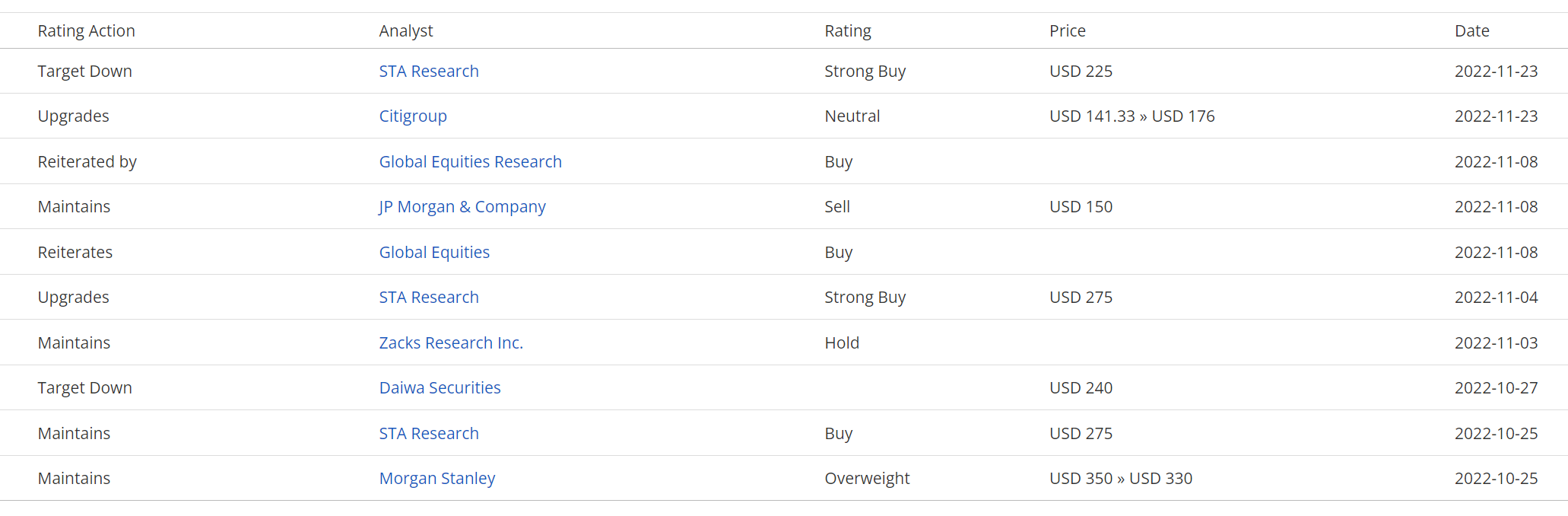

Average price target from analysts: $263.11

Investor Relations [click here]

Q3 2022 Earnings Report [click here]

Q3 2022 Earnings Call Transcript [click here]

Q3 2022 Earnings Call Presentation [click here]

Outline

Introduction

Company Background

Opportunity

Technology

Business Model

Competitive Advantages

Management

Culture

Financials

Key Metrics

Risks

Ownership

Valuation

Investment Model

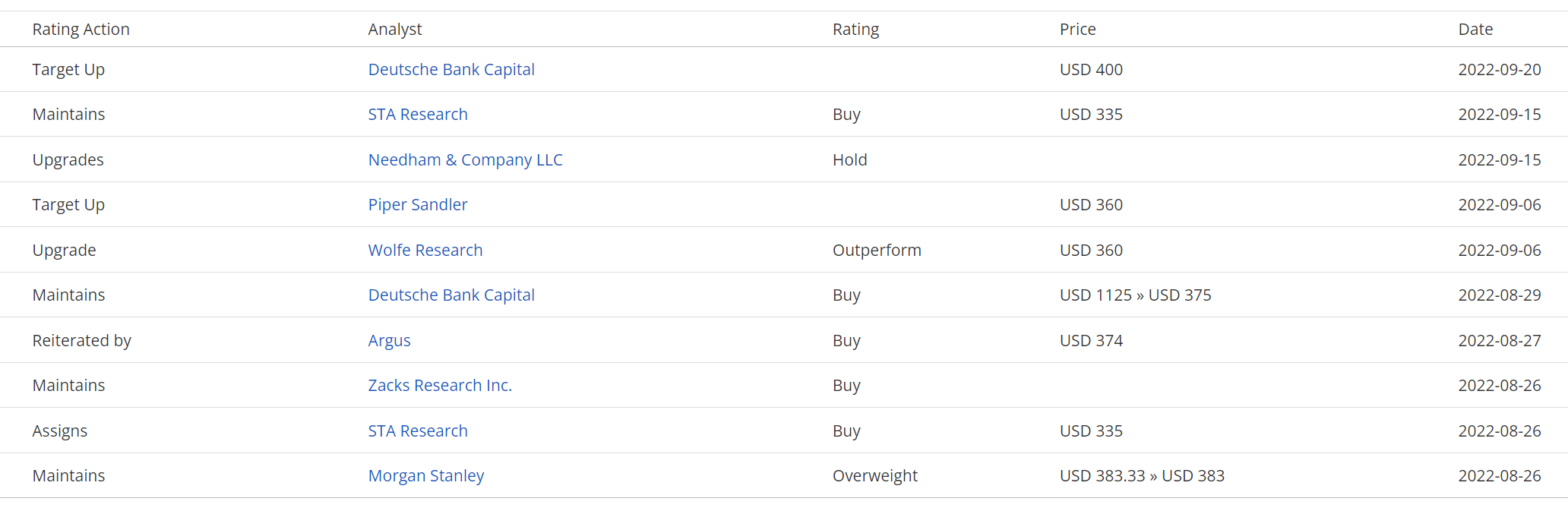

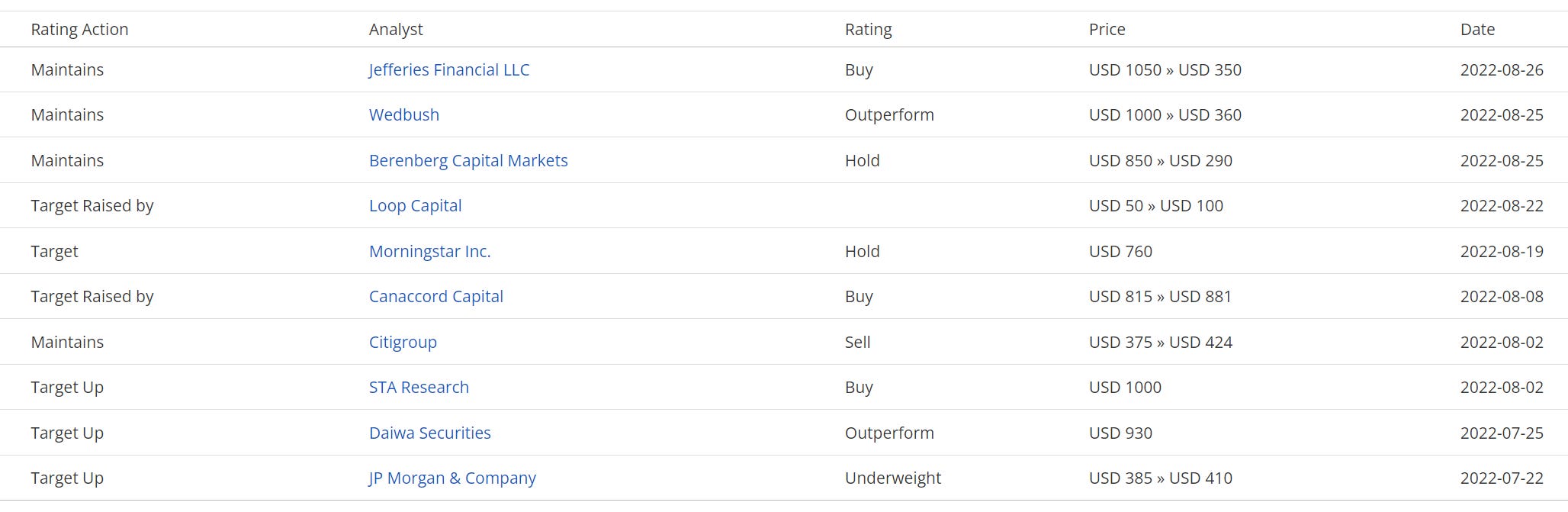

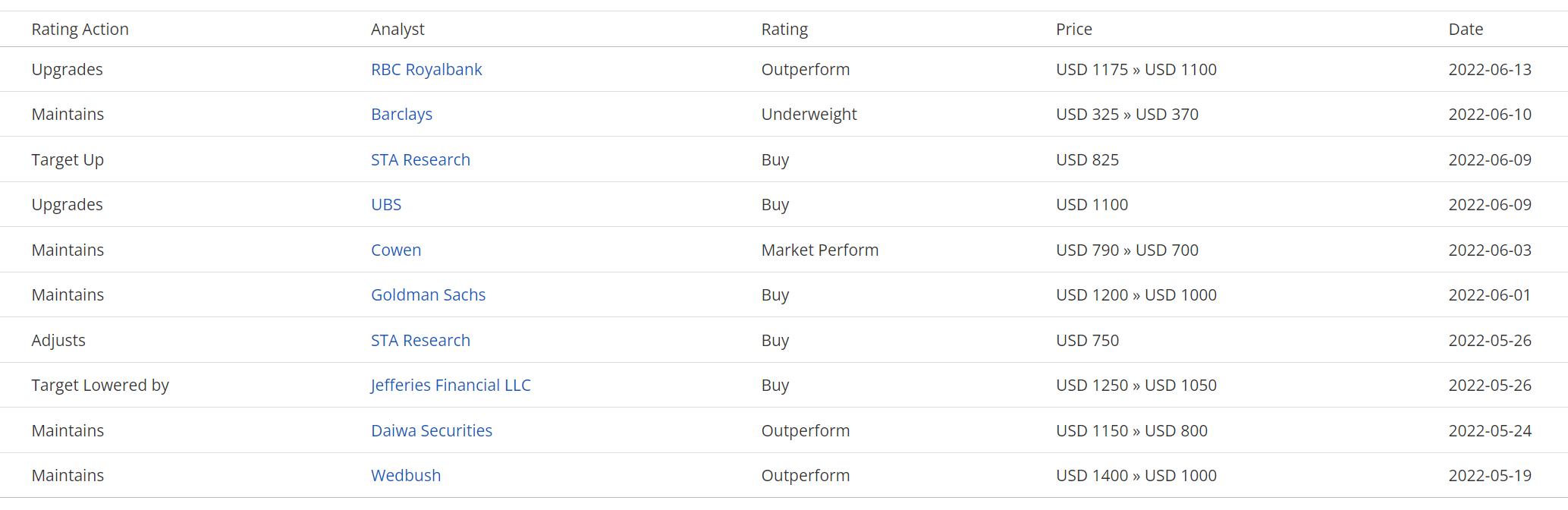

Analysts

Technicals

Conclusion

Introduction

This deep dive writeup on Tesla (TSLA) is going to be our longest writeup thus far, surpassing the UBER writeup that we did in June when the stock was trading in the low $20s. You can read the UBER writeup by clicking on the link below… FWIW, I remain bullish on UBER especially if they can grow revenues by 15-20% per year while growing grow free cash flow (FCF) much faster.

Now back to TSLA, to start things off I need to disclose that I currently have a TSLA position in my “investment portfolio” and I’m close to starting a TSLA position in my “trading portfolio” — the investment portfolio is 20-30 stocks that I hope to own for 12+ months (maybe longer) and consist of companies with strong fundamentals at reasonable valuations. My trading portfolio is 0-15 stocks based solely on the charts/technicals although trading stocks with strong fundamentals and potential earnings beats is a big plus.

My TSLA position is currently at 3.25% and I’ll continue adding if the stock goes lower from here. I bought TSLA for the first time ever in 2020 at ~$40 (split adjusted) and sold my entire position on the last trading day of 2020 at ~$238 (split adjusted). TSLA was one of the main reasons my investment portfolio was up more than 200% in 2020. I did try to get back into TSLA earlier this year after it dropped 30% from the ATH last year but I got stopped out pretty quickly. I then waited until recently when TSLA got down to $200, that seemed like a nice spot to start a new long-term (LT) position, knowing full well the stock could have another 20-30% downside depending on macro and the broad markets.

When I got back into TSLA, based on the charts, there were 5 areas of support that I was looking at for a potential bottom in the stock.

200week EMA

VWAP from March 2020 lows

VWAP from pre-pandemic highs (166.74)

200week SMA (163.18)

VWAP from the 2019 lows (134.66)

So for TSLA has blown through #1 and #2 but it bounced off #3 (VWAP from pre-pandemic highs) a couple weeks ago and so far that VWAP is still holding up. In case you’re not familiar with VWAPs, it stands for volume weighted average price and it’s one of my favorite technical indicators for where stocks are likely to find support and/or resistance.

I have no idea if the VWAP from the pre-pandemic highs holds up however if I was looking to start a trading position in TSLA I’d certainly love the risk/reward at these prices because I could use the VWAP and/or 200w SMA for my risk management (ie stop losses). Since they are so close together (only 2.1% apart), I’d just set my stop loss below the 200w SMA in my trading portfolio however in my investment portfolio I’m planning to DCA (dollar cost average) because I believe the TSLA valuation has gotten very compelling at these prices and I like the upside in TSLA over the next decade (although no promises I hold it that long).

In terms of the TSLA valuation, this is the cheapest the stock has ever traded with a NTM (next twelve month) P/E of 32.8x which is similar to the P/E for all of 2023 based on current EPS estimates (non-GAAP) from the analysts. They’re currently looking for $5.71 per share in 2023 ($179.04 / $5.71 = 31.3x) although it’s possible these numbers come down if the odds of a US recession continue to increase — even though I’m not convinced we’re going to have one, or at least not a bad one.

There are dozens of reasons to like TSLA and be bullish on the stock (which we’ll certainly talk about in this writeup) but there are also lots of reasons to be concerned about TLSA and wonder if the long-term investment thesis will come to fruition. Not that I’m trying to throw cold water on TSLA (because I believe there’s huge potential over the next decade) but here are 10 reasons/concerns that I think about most often:

Now that Elon Musk has acquired Twitter, how distracted will he be (not to mention this involved with SpaceX, The Boring Company, OpenAi and Neurolink) and will the energy and effort he should he putting into TSLA be sucked up elsewhere. Granted that Elon has phenomenal teams running all of these companies/ventures but this is still a lot for one person to balance.

Elon Musk is willing to shake this up at Twitter and rattle some cages however his recent comments about politics have the potential alienate potential Tesla customers, not just in the US but around the world.

If you’re a TSLA bull you are probably excited about the potential in China/Asia however there’s no guarantee that TSLA is going to dominate that market given how many China-based EV companies are already operating there. China is an ongoing geopolitical risk and will the CCP even allow TSLA to succeed and out-sell their own EV companies? There were rumors last week that TSLA is cutting back on production at their Shanghai facility however I believe the company denied those reports so it’s hard to know what’s true when it comes to China.

TSLA recently unveiled the SemiTruck (unveiled last week, I’ve also seen it written as just the Tesla Semi) when they delivered the first batch to Pepsi however it’s still very unclear what the demand is going to be for these EV trucks. We believe the pricing is $150,000 to $200,000 but the details on everything else is very limited. The TSLA SemiTruck has the potential to be a major revenue/profit contributor for TSLA but will that happen in the next few years?

The CyberTruck which is supposed to start production in 2023 could be delayed, very hard to know. Musk has already said there are 1+ million pre-paid reservations (ie tiny down-payment) and that they’re sold out through 2025 but things can change and the problems could arise. I think the hardcore TSLA fans love the CyberTruck because it’s so unique (looks like it belongs on Mars) but is there a big enough market for a niche truck/SUV like the CyberTruck or would TSLA have been better off coming out with a more classic looking pickup truck or 4-door SUV (like the X5 or Range Rover).

What will demand look like over the next 5-10 years for TSLA vehicles as the other auto makers start to catch up and the TSLA supercharger network isn’t quite the same advantage that it once was. TSLA is the clear leader in the EV market and I believe they still will be a decade from now but maybe Ford, GM, Toyota, Mercedes, Audi or someone else will surprise us.

Many states and countries have already announced their bans on ICE (internal combustion engine) vehicles starting as early as 2030, although most seem to be targeting 2035, however will they be able to stick with this or will these proposed dates get pushed back.

Most industry experts are calling for massive adoption in EVs over the next decade however can our current electrical grid support it? What level of electrical utility infrastructure upgrades need to happen over the next decade to support 50-100x more EVs on the road. According to this recent article [click here], approximately 5.2% of car registrations through the first 9 months of 2022 were EVs or BEVs (battery electric vehicles) which is up from 2.8% the previous year. It’s expected there will be ~16 millions cars sold this year in the US which means 800,000 to 900,000 EVs this year. If we assume that US car sales will continue to increase at 2% per year for the next decade (lots of factors will influence this) that would take US car sales to ~20 million over the next decade. If the % of EVs being sold goes from 5% of total cars in 2022 to 60% of total cars in 2023 (could be higher) than that means ~12 million EVs sold in 2033 but more important in terms of the electrical grid would be the 70+ million EVs on the road (yes I understand that some of the EVs sold over the next few years will no longer be driving in a decade).

As competition continues to heat up for TSLA from the legacy auto makers (Ford, GM, etc) what does that do to TSLA pricing power? does it drive up raw material costs like lithium? how do these factors and others impact their gross/profit margins? Right now TSLA is crushing the legacy OEMs in the margin category, for example in 2022 Q3, TSLA reported gross margins (GMs) of 25.1% while Ford (F) reported GMs of 7.6% (below their historical average) and General Motors (GM) reported GMs of 12.9% — there’s no doubt that TSLA is not only more vertically integrated than F and GM but they’re also the clear leader in technology, automation and robotics which leads to higher efficiency and better output/productivity. Simply put, TSLA can build their EVs much faster and cheaper than F or GM which gives them a clear competitive advantage however will this still be the case in 5 or 10 years? Personally, until proven otherwise I believe TSLA will continue to dominate in this area but I have no idea where margins will be in 5 or 10 years and I don’t think anyone else does either. Even if we could accurately project GMs on their current auto lineup, we have no idea what GMs will look like over the next decade for the SemiTruck, CyberTruck, Tesla bot and anything else the come up with … like a potential self-driving fleet of cars to compete with UBER 😯

TSLA currently has giga-factories in the US, Germany and China but how many will they have in 5-10 years. If you’re a TSLA bear you might be saying less and if you’re a TSLA bull you’re definitely saying more. I’ve read recent reports that TSLA is already looking at France, India and South Korea for new gigafactories so I’ll take the over however more countries means more geopolitical risks and more capital investments off the TSLA balance sheet. TBH, I’m not too worried about this one, I think global expansion is 10x the opportunity as it is a risk. Just like I did the math earlier on what EV sales in the US could look like in a decade, the opportunity in Europe and Asia could be gigantic although I suspect TSLA’s market share in those continents will never be as big as it is in the US or North America.

I’m sure I could come up with many more risks/headwinds for TSLA the company as well as TSLA the stock but we’ll stop it there. Even though I listed out these 10 risks, it’s still way too early to know which ones will be the biggest threat to TSLA’s growth over the next decade. Say what you want about Elon Musk, he’s certainly pissed off alot of people over the past few months, but this guy and his team get shit done. This is not a person I would bet against. I know he’s made lots of wildly optimistic announcements over the years and didn’t hit the timelines on many of them but he’s also done the impossible, not just as TSLA but also at SpaceX.

Even though I think Elon is presents lots of headline risks/liabilities to TSLA, he’s also the company’s biggest asset especially considering TSLA doesn’t spend any money on marketing because they have Elon and all the attention he gets from the media and across the internet.

As a proponent of free speech I want Elon to be himself and say whatever he wants however as a TSLA shareholder I want Elon to be a little less political and outspoken on certain topics because I do worry he’s harming the TSLA brand and driving away potential customers. I can’t imagine being in the spotlight every second of the day like Elon, so overall I think he’s done a remarkable job but now that he owns Twitter and he’s trying to grow TSLA into a global brand I think he needs to be a little more careful about what he does and says because it impacts TSLA whether he likes it or not.

I’ve been waiting over a year to do a TSLA writeup, I wanted to wait until the valuation was quite compelling and I’m excited that I finally get that chance. Hope you enjoy it.

Company Background

Tesla Motors was originally founded back in 2003 as an electric carmaker by two Silicon Valley engineers, Martin Eberhard (on the right) and Marc Tarpenning (on the left). The duo first met in the 1980s, and in 1997, they invented the first-ever eBook reader, The Rocket eBook.

The idea of Tesla came a few years later from Eberhard's love for sports cars. He actually had just gotten divorced at that time and found some distraction from it in sports cars, owning a number of them.

But back then, sports cars were 'thirsty,' consuming petrol heavily, yet pretty slow. With rising oil prices and the conversations about global warming getting more real, Eberhard decided to switch to an electric vehicle. However, the one generally available on the market, General Motors' EV1, was pulled off by the company shortly after the US government introduced the zero-emission mandate.

So Eberhard began searching for a company that could make an electric car for him. He wanted his car to "be better, quicker, and more fun to drive than a gasoline car."

In early 2000, Eberhard stumbled upon a small Californian company, AC Propulsion, that previously hand-made three electric sports cars, tzero, mainly to demonstrate them to larger car manufacturers.

He contacted AC Propulsion only to find out that the company was going out of business because of that zero-emission mandate. He eventually saved the company with his own money and paid to build a car for himself. That car was a lead–acid battery car, which was extremely dangerous to drive due to a possible explosion of such batteries and had other flaws.

A while later, with the help of Tarpenning, Eberhard came up with the idea of using lithium-ion batteries, which they had a lot of experience with while building consumer products. Eberhard further financed AC Propulsion to convert his car with lead–acid batteries to lithium-ion. That was essentially the proof of concept of the first modern electric car.

Eberhard and Tarpenning eventually decided to go after making their own car. But creating batteries for this car was just one part of the challenge. Building an actual car around it was a totally different task. Up to these days, for any small company looking to build a vehicle (Fisker, for example), the only way to do it is to outsource the manufacturing to larger OEMs (like Magna). That is precisely what the duo did in the beginning.

In late 2002, they flew to Los Angeles to attend the LA Auto Show, where they met executives from Lotus, a British automotive company that manufactures sports cars and racing cars. After a later meeting in England, Lotus agreed to build a vehicle for Eberhard and Tarpenning but only if they secured enough funding. In the summer of 2003, Tesla Motors was incorporated, and the duo began looking for outside capital. That is exactly when Elon Musk came on the radar.

Eberhard and Tarpenning actually encountered Elon Musk two years prior at a Mars Society talk at Stanford University. The duo were members of the Mars Society and met Musk at one of the conferences. Two years later, Musk ended up investing in Tesla Motors but as a result of totally different circumstances.

At the same time, as Tesla was pitching its vehicle to various VC investors in Silicon Valley, the AC Propulsion team was already in negotiations with Elon Musk. Ultimately, that investment fell apart, but because Eberhard had great relationships with the AC Propulsion team, they kindly agreed to introduce him to Musk. The rest is history.

"When we were pitching to VCs, they were all saying that we are crazy, trying to make an electric sports car. And then we pitched someone who is trying to make the rocket ships [Musk], and he said let's do it." – Marc Tarpenning, co-founder of Tesla Motors, in an interview with CNBC.

Musk led the first round of investment in Tesla Motors in 2004. He invested $6.35 million of Tesla's $6.5 million Series A funding to get the company off the ground. He also became the chairman of the board.

In 2006, Tesla unveiled the first-ever prototype of its sports car, Tesla Roadster. The Roadster got tremendous attention immediately, even before the car was for public sale.

The company took thousands of reservations, which no other car manufacturing company ever did, and the best part was that they came without spending a dime on marketing. Word-of-mouth attracted early adopters from all around the world who wanted to be a part of this electric revolution. And it was indeed the beginning of something big.

But when Tesla was starting out, literally everyone in the automobile industry was saying that an electric sports car won't work. "It won't drive even 100 miles," they said. What Musk did later changed the automobile industry forever, and perhaps, some other industries (i.e., energy) too.

However, the road to success was extremely bumpy for Musk. The company constantly needed capital, and by 2007, it had taken over $100 million in investments, mostly in debt financing. Musk has participated in all rounds alongside a group of prominent entrepreneurs (including Google co-founders Sergey Brin and Larry Page, former eBay President Jeff Skoll, and Hyatt heir Nick Pritzker) and VC firms, but the company kept running out of money.

As a result of cash burning going out of control, Martin Eberhard stepped down as CEO in August 2007. Tesla Motors had two more CEOs before Elon Musk took over the company in October 2008. At that moment, Tesla was on the verge of bankruptcy, laying off 25% of personnel as soon as Musk's reign began. He had to take another debt financing round ($40 million) to save the company.

In 2009, Tesla finally delivered its first Roadster to a customer and unveiled the prototype of its next car – Model S, but the need for capital was higher than ever. That year, Daimler AG, maker of Mercedes-Benz, acquired nearly 10% of the company, reportedly for $50 million. Musk recalls that investment to be the saver of Tesla.

Getting private funds got harder and harder, and eventually, Tesla filed for an IPO in January 2010 in the hopes of gaining access to public money. On June 29, 2010, Tesla became the first US automaker to go public since Ford Motors in 1956. Tesla began trading at $17 per share, which was above the $14 to $16 expected IPO range. The company raised approximately $226 million during its IPO.

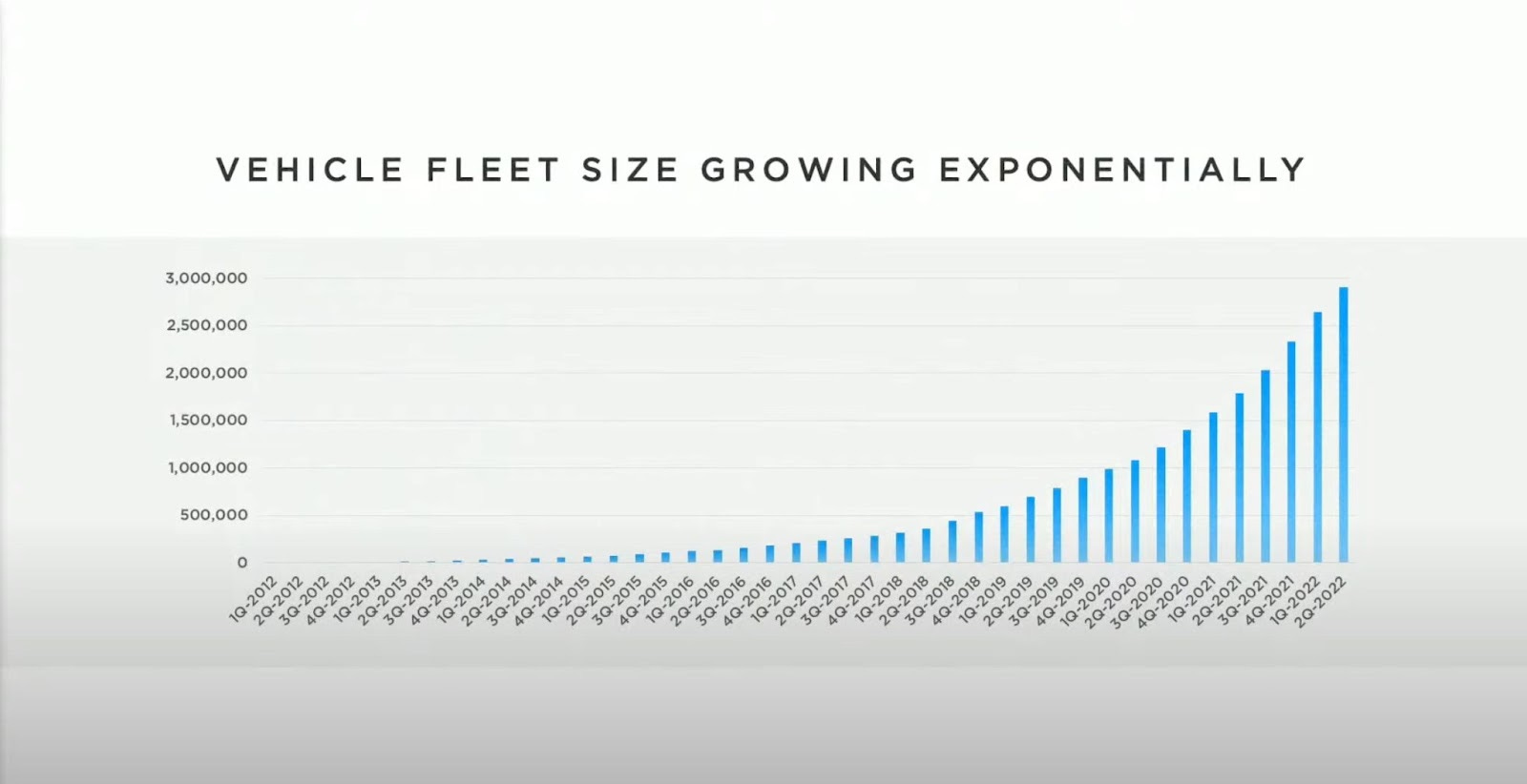

The first Model S was delivered in 2012, and by the end of that year, Tesla sold around 3,000 cars. Fast forward to today, the company is on the way to delivering more than 3 million cars in 2022, an incredible result for a company that was a tiny startup just ten years ago.

Throughout these years, Tesla went from several more bankruptcy crises and even a called-off sale of the company to Google for $11 billion in 2013 to building several state-of-the-art own factories and having a wide range of car models. The latter is the key to Tesla's incredible success.

From the very beginning, Musk followed a strategy to create affordable mass-market electric vehicles by starting with a premium sports car aimed at early adopters and then moving into more mainstream vehicles, including sedans and affordable compacts. This strategy played out exceptionally well for Tesla, so that many new entrants, like Lucid (LCID), are trying to copy it.

“Our goal when we created Tesla a decade ago was the same as it is today: to drive the world’s transition to electric mobility by bringing a full range of increasingly affordable electric cars to market” – Elon Musk.

Today, Tesla is not only the most valuable car manufacturer in the world, selling more cars than any other car company, but also on the way to becoming one of the largest solar panel and clean energy storage manufacturers and operators. In 2021, Tesla deployed 322 MW of solar panels and 4.3 GWh (over 15% of gigawatt hours globally) of clean energy storage.

From a highly cash-burning company selling just a sports car, Tesla became a company with multiple revenue streams that generate billions in free cash flow. Furthermore, Tesla has been profitable on a GAAP basis since 2020, and in Musk's words, "it will only go up from there."

Tesla is undoubtedly a technology company (many still mistakenly think it is only a car manufacturer), and it is just getting started. The opportunity further is one of a kind, and it is what makes Tesla a special company, a company that one day may become the most valuable company among all companies, not just car manufacturers.

Opportunity

Tesla, without any doubt, has started an electric vehicle revolution. Without Tesla, we would most likely continue driving internal combustion engine (ICE) vehicles in masses, further causing irreparable damage to our planet. Electric cars are not only the biggest change to the automobile industry, perhaps, it has ever seen, but also one of the most significant changes for humanity in the last several decades at least.

Though it is still very early days of the transition to a gas-free world, EVs are already taking share from ICEs and at a rapid pace. By now, every major car automaker, from manufacturers of passenger cars to trucks and buses, has committed to electrification.

According to Global Electric Vehicle Outlook, EV sales doubled in 2021 from the previous year to a new record of 6.6 million. In 2021, the number of vehicles sold in just one week was the same as the total number of all electric cars sold in the entire of 2012 (120 000 vehicles sold worldwide).

There are a number of reasons why EV sales are on the rise. To begin with, there is an increasing number of federal, state, and utility programs across the world that offer subsidies and incentives for EVs. Public spending on them almost doubled in 2021 to nearly $30 billion.

Tesla alone has benefited immensely due to such programs and incentives, the biggest ones being in California state, where the company was based until last year (it moved to Austin, Texas, in December 2021). Californian public policy and funding not only paved the way for electric passenger cars' adoption and rise but significantly contributed to Tesla's success. As a reminder, other automakers had to buy credits from Tesla if they didn’t sell enough electric vehicles. This way, Tesla received nearly $1 billion from 2012 to 2017. And that's not to mention the different tax incentives, economic benefits, land use rights (in China, specifically), and more.

Indeed, governments all around the world are trying to incentivize EV purchasing as a pledge to reduce or eliminate combustion engine vehicles by a certain year. Most developed countries were initially projected to reach net zero CO2 emissions by 2050, but all of them are now falling behind.

Nevertheless, with high certainty, we will see a dramatic increase in the number of EVs in the coming years. In its New Energy Finance Electric Vehicle Outlook, Bloomberg projects that almost 50% of all new vehicles sold in the US and Europe by 2030 will be EVs, which will be more than 200 million vehicles, 11x more than the current amount.

And Tesla is best positioned to grab a piece of that enormous market. Actually, the company projects to sell a whopping 20 million electric vehicles per annum by 2030. Just to put it in context, since its inception to this date, Tesla has sold 3.2 million cars cumulatively. Whether the company will reach this number or not, Tesla follows a certain strategy that has already proved to be highly successful and should serve as a blueprint as it advances further.

“We are still a very small percentage of the total vehicles on the road. Of the 2 billion cars and trucks on the road, we only have about 3.5 million. So, we’ve got a long way to go to even reach 1% of the global fleet.” – Elon Musk at Q3 2002 earnings call.

This strategy starts with the car model lineup. As of 2022, the company sells four vehicles in two price categories: luxury and more affordable.

Model S – a four-door, full-size luxury sedan that starts from $95,000 (from $50,000 for a used car). It is Tesla's flagship car with the highest performance characteristics and longest ranges the company offers. In 2021, Tesla launched new versions of the Model S (Model S Plaid), offering higher performance and range.

Model X – a mid-size luxury SUV with seating for up to seven adults that starts from $105,000 (from $50,000 for a used car). It is another company's flagship vehicle with the same characteristics and ranges as the Model S. Tesla now also has the Plaid version of this model.

Model 3 – a four-door, mid-size sedan designed for the mass market with a base price starting at $45,000 (from $30,000 for a used car). It is the most affordable Tesla to date and one of the best-selling cars in the world (in the top 10).

Model Y – a compact SUV built on the Model 3 platform with seating for up to seven adults that starts from $60,000 (from $57,000 for a used car). It is on the way to becoming one of the best-selling cars in the world.

All car prices do not include potential incentives and gas savings that vary by location.

Having a car model lineup for almost every budget makes Tesla a serious contender in the market that gets increasingly competitive every day. But there is something else that puts Tesla in the front seat: the production costs keep going down. Tesla's costs of goods sold per vehicle fell to about $36,000 in 2021, while they were 2x higher in 2017. The average selling price in 2021 was $49,000, and as the company ramp-ups the Berlin and Austin factories, as well as continues to scale and improve its vehicle platform and batteries, the average selling price should further go lower, making Tesla cars more affordable, especially the mass-market ones, Model 3 and Model Y. ARK expects the average selling price to reach $38,000 by 2026, and in the best case scenario – $30,000.

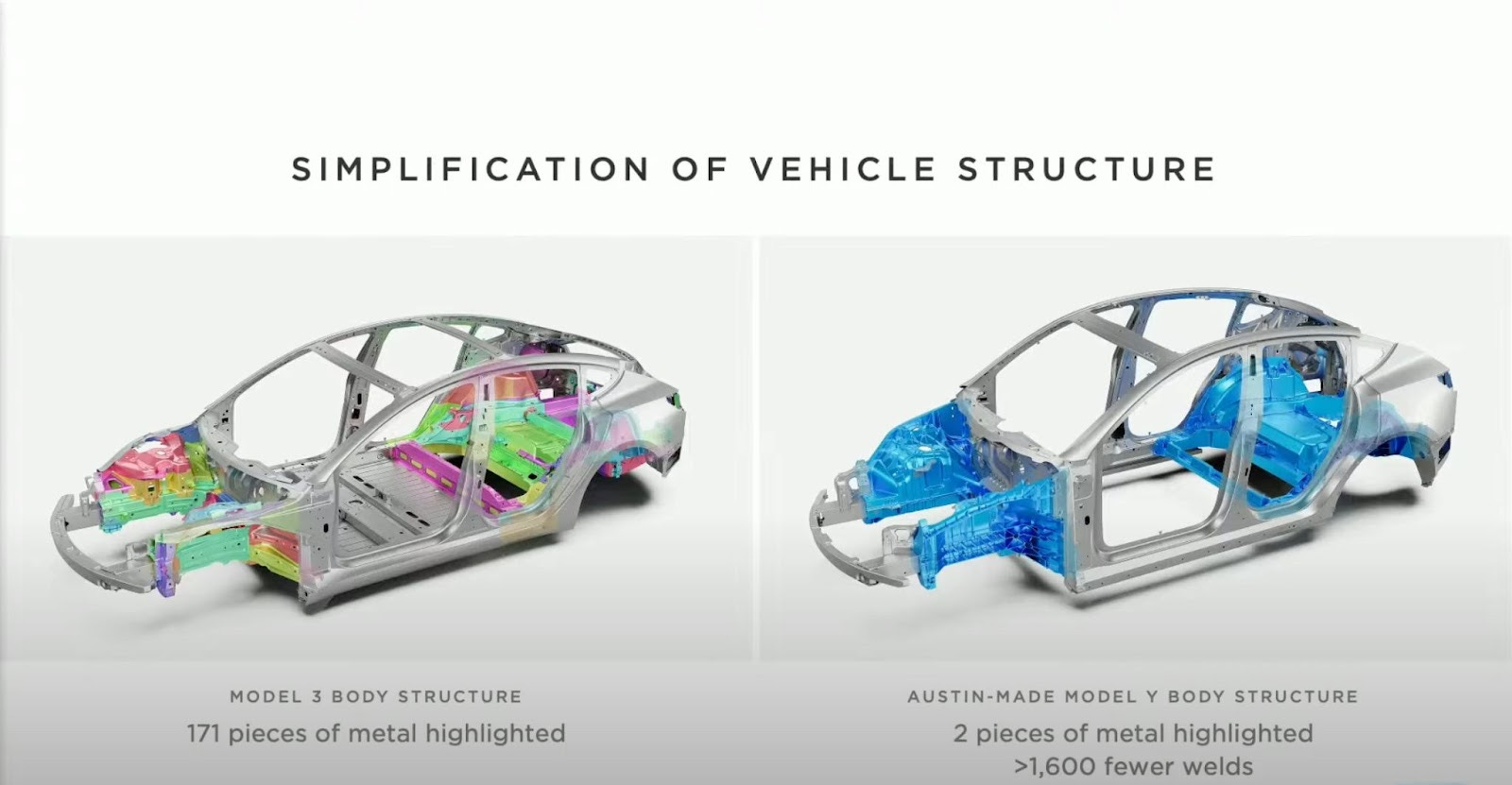

Tesla does a phenomenal job on the cost-cutting front. The move from Tesla’s first platform with S and X to the second platform with 3 and Y, led to a 50% reduction in the cost of goods sold. Here is one bright example of further optimization: in Model 3 production, the company managed to get 171 metal pieces into just 2 pieces, making it lighter and stiffer in the process. These sorts of manufacturing optimizations are what drive the price of cars down while improving the margins for the company.

In 2017, Tesla announced Tesla Semi, a fully electric Class 8 semi-truck, as a further expansion to other automobile segments. The heavy-duty trucks market is $204 billion and expects to reach $314 billion by 2027 (CAGR of 7.4% during 2022–2027), according to Mordor Intelligence research. The demand for new and advanced trucks (hybrid and electric) should significantly increase due to rising regulations on vehicle emissions, advancement in vehicle safety, and rapidly growing logistics, retail, and e-commerce sectors all across the world. Eventually, all trucks will become electric.

Currently, the Class 8 market is dominated by Freightliner (owned by Daimler), with a market share of almost 40% (in the US) as of 2021. Volvo (owned by Mack Trucks) dominates more in Europe. A lot is going on in this industry segment, from installing a high-performance public charging network for battery electric, heavy-duty long-haul trucks to growing government regulations that push electric truck adoption. And now Tesla is part of it.

After more than five years since the unveiling, Tesla finally delivered its first production version of the heavy-duty Semi to its first customer, PepsiCo, on December 1, 2022.

However, the company has yet to announce the pricing, production plans, or how much cargo it will be able to carry. Tesla did say briefly that Semi will have 500 miles of range on a single charge, which can be achieved by hauling a max payload of 82,000 lbs of freight. It will also be charged by newly developed megawatt class chargers and cables, coming to Tesla charging sites within 2023.

More information about the vehicle is yet to be revealed, but the Tesla Semi launch is definitely a big thing not only for the company but for the entire industry. Hundreds of articles and analyses have been written on how Tesla Semi will change the industry. To summarize them all, it will deliver some extreme savings when it comes to operation (up to $200,000 over 3 years according to Tesla’s estimates) and for a price that no other truck manufacturer can match (the initial price announced in 2017 was $180,000, without the impact of the Inflation Reduction Act, which ads $40,000 in incentives for every clean energy commercial vehicle).

Musk expects the company to produce 50,000 units per year by 2024 in the industry segment where the total number of vehicles sold yearly is roughly 250,000. This is a very ambitious goal, but if executed well, it could add an additional $9 billion in revenue per year.

What else will certainly add to revenue is the upcoming launch of Tesla Cybertruck. First unveiled in 2019 and postponed in production several times, it is also finally expected to go into final production in the forthcoming months (mid-2023).

The pickup truck market is another large segment of the automotive industry. According to Fortune Business Insights, the global pickup truck market was $186.6 billion in 2021 and is expected to grow to $256.5 billion by 2028 (CAGR of 4.65%). The market growth is propelled by the same trends as the growth of the heavy-duty trucks market.

Unlike heavy-duty trucks, pickup trucks are light-duty vehicles primarily used to transport products and freight by commercial companies. But in some countries, like the US and Mexico, pickup trucks are heavily used for passenger cars.

Since the prototype was shown in 2019, Cybertruck went significant changes, according to several insiders. We are yet to hear more from Tesla, but as of the end of 2022, the company received more than 1.5 million reservations for Cybertruck. The demand is certainly there, which will result in billions of revenue in the coming years. Suppose Tesla sells all pre-orders, depending on the final cost of the vehicle (insiders suggest the average selling price will be between $50,000 and $80,000). In that case, it is an additional, absolutely enormous $75 billion in potential revenue on the lower end.

But, perhaps, the real big thing for Tesla is self-driving cars with robots, also called the RoboTaxi business. In its recent event of delivering Tesla Semi, the company has put a slide (below) with a mock-up of the future car covered under a tarp with the word 'robotaxi.'

RoboTaxi is a long-waited autonomous ride-hailing service by Tesla that may change not only the entire business for the company but also the entire transportation industry, making companies like Uber and Lyft obsolete.

To begin with, the gross margins on the autonomous car will be similar to those of SaaS companies. Then, the total addressable market for autonomous ride-hailing is estimated to be $11-12 trillion. Yes, T-trillion.

If the company accomplishes self-driving, Tesla will be the most valuable company in the world by a mile and for a long time. ARK Investment, the biggest bull of Tesla, believes it is the question of when not if. They predict it will happen in 2026, and the robotaxi business line will be the company's key driver, contributing 60% of the expected value and more than half of the expected EBITDA in 2026.

Even if Tesla isn't able to deliver the robotaxis or decides not to launch it for whatever reasons, a human-driven network of Tesla cars could become as large a business on its own as all ride-hailing services today, ultimately accounting for 30% of the company’s enterprise value and dramatically improve its profitability.

Launching a ride-hailing service with drivers makes more sense strategically. A human-driven ride-hailing network of cars would allow Tesla to collect real-world driving data to feed its autonomous driving artificial intelligence (AI) training system.

There are also other advantages of the human-driven network:

Lower operating expenses – the cost to drive a Model 3 is roughly 30% less than that of a Toyota Camry, so Tesla's cost per mile may be advantageous for both drivers and passengers in several ways: i) higher take-home pay for drivers; ii) lower prices for passengers than Uber and Lyft; and iii) Tesla can take higher platform fees without sacrificing the first two.

More efficient financing and insurance – Tesla will be able to offer rates lower than traditional insurance companies and should be able to finance its own vehicles, while Uber and Lyft pay fees to third-party partners at the expense of drivers (less pay) and passengers (higher prices).

Higher trade-in or residual values – the trade-in or residual value of Tesla vehicles (currently around 95% after the first year of use) should be much higher than that of traditional ride-hailing vehicles (around 80%). “The public, at large, realizes that everyone’s moving towards electric vehicles and that it’s foolish to actually buy a new gasoline car at this point because the residual value of that gasoline car is going to be very low.” – Elon Musk on Q3 2022 earnings call.

Musk has repeatedly noted that "cars will go from owning to renting for some time to renting a lot to renting indefinitely." There will be an option to own a car or use it occasionally, and the owner will also be able to share the car with Tesla’s fleet. So many new businesses may emerge with the introduction of the ride-hailing service.

While Tesla aims to sell millions of vehicles of all kinds per year, whether for personal or commercial use, the growth of these sales is only possible with a clean energy ecosystem. The rapid adoption and penetration of EVs severely depend on an extensive network of EV charging stations, which, in turn, depend on energy gained from solar panels and energy storage units.

Tesla began building out its clean energy ecosystem in 2016 after the acquisition of SolarCity (for $2.6 billion in stock), then the largest installer of rooftop solar systems in the United States. This segment has grown exponentially since then, with solar roof deployments nearly tripled in 2021. At one point, Tesla was saying that the solar business could be bigger than its vehicle segment. However, vehicle sales have skyrocketed since then, and the latest reports indicate that Tesla has been unscaling the solar segment due to serious supply chain problems. Whether it is short-term obstacles or a possible change in strategy, Tesla is still one of the largest solar systems operators in the US. Musk is a firm believer in solar energy, and it is unlikely the company will shut down its solar division.

Moreover, using solar (and wind) combined with energy storage is becoming the cheapest energy option. Energy storage possibly plays an even bigger role in Tesla's clean energy ecosystem as it transforms the global electric grid and is an increasingly important element of the world’s transition to sustainable energy, with or without solar.

According to Bloomberg New Energy Finance forecasts, the energy storage solutions and services represent a $1.2 trillion revenue opportunity cumulative through 2050. The current capacity of energy storage solutions is still in its infancy compared to wind and solar deployments.

First introduced in 2019, Tesla's Megapack system is a powerful battery that provides energy storage and support, helping to stabilize the grid and prevent outages. Each unit can store over 3 MWh of energy, enough to power an average of 3,600 homes for one hour.

Tesla's energy storage deployments have nearly quadrupled in the last four years since the launch of Megapack and now represent over 15% of gigawatt hours globally. “We actually see the energy storage business growing more like 150% to 200% a year, faster than cars by a lot.” – Elon Musk on Q3 2022 earnings call.

Tesla is competing with Stem (

) for leadership in energy storage deployments, and according to several resources, Tesla has overtaken Stem as a global leader.

Demand for energy storage products is far outpacing the company’s current ability to supply. To address this growing demand, the company is rapidly ramping up production at its dedicated 40 Gwh Megapack factory in Lathrop, California, United States.

Further cost reduction of solar and energy storage products will foster mass adoption, positively impacting Tesla's top line in total revenue and bottom line in car sales revenue.

There might be a lot of hype and contradiction surrounding Tesla and Musk especially, but this company has never disappointed, delivering on all of its promises (maybe with some delays and minor changes) so far. With ample cash on its balance sheet (and its further growth) and tremendous optionality, Tesla truly offers a once-in-a-lifetime opportunity for investors.

“Tesla went, in fact, or passed Apple’s market cap at the time. And now, I’m of the opinion that we can far exceed Apple’s current market cap. In fact, I see a potential path for Tesla to be worth more than Apple and Saudi Aramco combined.” – Elon Musk.

Technology

Tesla is among the most technological companies in the world. The world's brightest engineers strive to work at Tesla, helping the company to create the most technology-advanced products. Indeed, the amount of technology behind Tesla's products is simply mind-blowing.

At the very heart of what Tesla does is its batteries. Batteries are what the original founding team was starting from almost two decades ago. Tesla went from low-capacity 18650-type cylindrical ion batteries designed for general purposes (produced and imported by Panasonic from Japan, used in the Roadster and early Model S and Model X) to much larger 2170-type, optimized for electric cars (produced by Panasonic at the Tesla Gigafactory 1 in Nevada and LG Chem at the Tesla Giga Shanghai, used in Model 3 and Model Y, as well as for energy storage products) to new (launched in 2022) and the largest so far, the 4680-type, which is 5x larger than 2170-type (produced by Tesla in-house in California and Texas, where the company has built the world’s largest ion battery factory).

There is one more battery type – prismatic type, which is made from LFP cells that contain no cobalt or nickel, making them cheaper to produce from more readily available materials but less energy-dense, which means they offer a much lower range than 4680-type. According to InsideEVs, half of all cars produced in Q1 2022 were equipped with LFP batteries (produced by CATL in China). This type of battery is ideal for entry-level vehicles (Model 3 and Model Y) and energy storage systems. LFP batteries are also much easier to recycle.

Recycling is also something worth mentioning. Though there are not too many batteries to recycle today, as EV cars have much more extended longevity (10-12 years, on average), recycling will become more significant in the next decade or so. And Tesla has already begun recycling battery packs at its Nevada factory at the rate of 50+ per week.

Tesla uses a very smart strategy to utilize various battery types for various of its products, depending on the cost of the product. This allows the company to increase gross margins for cheaper products without necessarily increasing the price of these products.

Despite building its own battery factory ready for mass scale and working on its own lithium refinery, Tesla continues to use other manufacturers like Panasonic and LG to diversify the production of batteries in order to be the first to achieve 1,000 gigawatt hours a year of production capacity in the United States. Moreover, Musk continues publicly urging other companies to produce more raw materials for batteries (iron and nickel specifically).

“We’re moving as fast as possible to achieve 1,000 gigawatt hours a year of production capacity in the United States, vertically integrated, anode-cathode. We’re moving at top speed to do that.” – Elon Musk on Q3 2022 earnings call.

Tesla unites its battery technologies with its proprietary powertrain systems, creating unrivaled performance, range, and efficiency. Powertrain refers to the components that generate the power required to move the vehicle and deliver it to the wheels, i.e., motors. Tesla uses dual motors to maximize traction and performance in an all-wheel drive configuration, and three electric motors for further increased performance in certain versions of Model S and Model X. New module and pack thermal architecture (pictured below) allow faster charging and provide more power and endurance in all conditions.

Bringing all pieces together requires world-class manufacturing. Throughout the years, Tesla has built 6 state-of-the-art factories, which are among the world's most efficient and technology-advanced. Each factory is a massive technology universe full of custom-built robots, assemblies, and other hardware.

The first factory opened by Tesla (in 2012) was the factory in Fremont, in the Bay Area of California, United States. It was the first to build all models (Model S, Model 3, Model X, and Model Y) and vehicle battery cells. The Fremont factory is the largest employer providing over 17,000 jobs. It also became the most productive car factory in the US.

Next came Gigafactory in Nevada, United States, which began the production of motors, batteries (by Panasonic), and power electronics in 2017.

That same year, Tesla opened Gigafactory New York, United States, where the company makes solar roofs, solar panels, and Superchargers.

In 2019, for the first time in its history, Tesla opened a factory outside the US. The Shanghai Gigafactory significantly helped the company reduce transportation and manufacturing costs for vehicles sold in local markets (Asia, being one of the largest, if not the largest, market for EVs in the world). The company produces batteries, motors, Model 3, and Model Y in Shanghai Gigafactory and anticipates increasing its capacity in the coming years.

Most recently, Tesla has opened two more factories: one in Berlin-Brandenburg, Germany, and one in Austin, Texas, United States, which became the company's new headquarters.

Gigafactory Berlin-Brandenburg is a significant achievement by the company, further expanding its international expansion, specifically in the European market, which has been and is mainly dominated by European car makers. Currently, Tesla manufactures batteries, motors, and Model Y in Germany.

Gigafactory Texas became the primary factory for Tesla's 4680 batteries, and it also produces Model Y.

In the most recent shareholder's meeting event, Musk hinted (with a slide on the screen, pictured below) that another factory is coming out soon.

Making Tesla's 'computers on wheels' safe and drivable requires sophisticated control software, which plays a critical role in Tesla's success. The control systems that the company has designed and developed help to optimize vehicles' performance, customize their behavior, manage charging, and control all infotainment functions.

Tesla was the first company to introduce over-the-air software updates. What Tesla is capable of doing with its software is incredible. For example, the company can update the software in all cars to make airbags better deployed to improve safety in a car crash. And it does it based on data it collects from hundreds of thousands of vehicles. With software updates, Tesla cars manufactured three-four years ago today can drive farther, faster, and more safely than back then.

“We are as much a software company as we are a hardware company. Software will play a crucial role in the future, not only in the cars but also in our factories.” – Elon Musk.

Software will also enable additional revenue streams for the company over time.

"As our vehicles are capable of being updated remotely over-the-air, our customers may purchase additional paid options and features through the Tesla app or through the in-vehicle user interface. We expect that this functionality will also allow us to offer certain options and features on a subscription basis in the future." – from Tesla's 10-K.

Musk's end goal with its software is to create fully autonomous cars. “Eventually all cars will be self-driving.” – Elon Musk.

In combination with its software, Tesla develops unique technologies and systems to enable self-driving vehicles using primarily vision-based sensors. Each Tesla vehicle has a Full Self-Driving (FSD) Computer inside, which enables the massive amounts of field data captured by all vehicles to continually train and improve Tesla's neural networks for real-world performance. This data helps Tesla develop its Autopilot.

While all Tesla vehicles still require active driver supervision and are not fully autonomous today (require regulatory approval), the Full Self-Driving computer and the purchase of Full Self-Driving capability can enable certain features that allow turning into a fully self-driving vehicle (at driver's risk). As of Q3 2022, there are more than 160,000 full self-driving vehicles in North America.

The company leverages many of the component-level technologies from the vehicles in the solar energy systems and the energy products, including the Supercharger, Tesla's charging station, which now has more than 40,000 superchargers globally, maintaining 99.6% network uptime. Like with its vehicles, all other products can also be updated over-the-air.

There is clearly so much more innovation going on at Tesla on both the hardware and software fronts. So many projects are in research and development, like a humanoid robot (Tesla Bot) or something we have yet to hear from the company. While competition will only intensify moving forward, innovation is what will help Tesla stay ahead of it. Maybe Tesla's next big thing is far outside the automobile industry.

“We are quite in a good position of investing in everything we can think of to possibly invest in, and we’re still generating cash.” – Elon Musk on Q3 2022 earnings call.

Business Model

Currently, Tesla generates most of its revenue (~87%) from the automotive segment, which includes vehicle sales, regulatory credits, and leasing. The remaining revenue comes from energy generation and storage (~5%) and services and other (~8%).

Automotive sales revenue includes revenues related to cash deliveries (vehicles that are not subject to lease accounting) of all new Tesla vehicles (Model S, Model X, Model 3, and Model Y).

The automotive sales also include:

Access to the Supercharger network (starting at $0.14 per kWh, based on how busy the network is at the time of charging);

Premium internet connectivity inside the cars (a monthly subscription of $9.99 or an annual subscription of $99 plus applicable tax);

FSD features (Autopilot costs an additional $6,000 while full self-driving capability – $15,000);

and future over-the-air software updates (like FSD features).

Automotive regulatory credits revenue includes sales of regulatory credits to other automotive manufacturers. To reduce CO2 emissions, governments around the world have introduced incentives for automakers to develop electric vehicles in return for credits. Since Tesla sells only electric cars, it receives these credits essentially for free and can sell them for a considerable profit to other automakers who can’t meet regulatory requirements. The credit system works in the US, Europe, and China.

Tesla has been very successful in selling regulatory credits in the past several years. For example, one of its customers, Stellantis (owner of Chrysler, Dodge, Fiat, Alfa Romeo, Citroen, Peugeot, Jeep, RAM, and a few others), bought credits from Tesla worth around $2.5 billion between 2019 and 2021 alone.

Finally, automotive leasing revenue includes the amortization of revenue for vehicles under direct operating lease agreements and those sold with resale value guarantees. Tesla, directly or through some financial organizations, offers leasing and loan financing arrangements in certain jurisdictions in North America, Europe, and Asia.

Additionally, automotive leasing revenue includes direct sales-type leasing programs offered by third parties, which buy vehicles from Tesla for the full price.

Services and other revenue consist of:

Non-warranty after-sales vehicle services (through company-owned service locations and Tesla Mobile Service technicians who perform work remotely at customers’ homes or other locations);

Sales of used vehicles;

Retail merchandise (apparel and lifestyle accessories), vehicle accessories (liners, racks, sunshades, snow chains, etc.), and charging accessories (Wall Connector, Mobile Connector, cables, adapters, etc.);

Sales by the acquired subsidiaries to third-party customers;

Vehicle insurance revenue (insurance product using real-time driving behavior in Arizona, California, Illinois, Ohio, and Texas).

Energy generation and storage revenue include:

Sales and leasing of solar energy generation (Solar Roof and Solar Panel) and energy storage products (Megapack, Powerwall);

Services related to such products;

Sales of solar energy systems incentives.

Tesla typically sells integrated solar and battery storage together. A 2,000 sq ft, one-story home will require a 7.34 kW Solar Roof and 1 Powerwall Battery. The estimated price for the Boston area is $207,000, excluding federal tax credit of an estimated $59,000.

Usually, car manufacturing is a low-margin business due to the high costs of production and materials. Tesla is not an exception. However, due to many optimizations in the manufacturing process and the overall much simpler structure of its vehicles, Tesla has the highest margins in the entire automotive industry.

Tesla's automotive gross margin has been increasing in the last several years, from 21.2% in 2019 to 25.6% in 2020 to almost 30% in 2021. In the first quarter of 2022, the company saw a gross margin of nearly 33%, though it went down to 27.9% in the latest quarter due to higher costs of raw materials, commodities, logistics, warranty, and expedite, as well as high costs of production ramp of Texas and Berlin-Brandenburg Gigafactories.

Tesla is still losing money in other segments. Services and other segment has a negative gross margin (but improving), while the gross margin for the energy generation and storage segment fluctuates from negative to positive quarter-over-quarter but is on the verge of becoming positive for the full year for the first time in the company's history.

As a result, the company's total gross margin is about 25%. Right now, hardware revenues dominate, but over time the company expects an acceleration of software-related profits, which will help improve margins considerably.

Tesla also has the highest operating margins in the industry, growing from negative ~1% in Q3 2019 to positive 17.2% in Q3 2022.

Historically, Tesla managed to generate significant media coverage for its products, which was the main driver of their sales. The company has famously spent little to nothing on traditional advertising and marketing, generating billions in profits.

Tesla sells its vehicles primarily through the DTC channel (its own website and an international network of company-owned stores) and through some third parties that sell used vehicles on behalf of Tesla.

In the solar and energy storage segment, the company sells products to residential, commercial, and industrial customers and utilities through a variety of channels, including its own website, stores, and galleries, as well as through its network of channel partners. Internationally, Tesla has dedicated sales teams. And when the company sells to utilities or channel partners, these partners typically sell Tesla's products to residential customers and manage the installation in customer homes themselves.

Competitive Advantages

Tesla has been a first mover in electric vehicles for a decade and enjoyed many benefits that came along with this advantage. However, the rapid mass adoption of EVs (thanks to Tesla) led to a complete transformation of the entire automotive industry. Traditional car manufacturers shifted their focus to EVs, while many new companies started to emerge that develop electric vehicles only.

Tesla's share of the EV market started to shrink gradually. It went down from more than 90% in 2017 to about 79% in 2020 to less than 65% today. It has been especially noticeable in the past two years as more and more car manufacturers ramped up production of their EVs and began deliveries.

Tesla's market share will decrease more over the following years. It does not necessarily mean that Tesla's growth will slow, as the number of EVs sold worldwide will increase manifold, but the competition will certainly intensify. There are already over 450 different EV models on the market, providing an ample variety of choices for any consumer's taste and budget.

It is also worth mentioning that Tesla is now seeing increased pressure from China, the world's largest EV market. Chinese rivals (like Nio, Li Auto, Xpeng, and BYD, among others) have not only learned how to successfully build EVs but also already show impressive delivery numbers, counted by millions.

Tesla also sees competition in other areas of the automotive segment. For example, its Supercharger network faces competition from other EV charging companies. One particular company, ChargePoint (CHPT) is the largest EV charging network in the world, with over 200,000 activated ports and over 350,000 ports accessible via roaming integrations. While Tesla's Supercharger network is still closed for non-Tesla vehicles, ChargePoint (and similar companies) allows charging any Tesla car and may take market share from Tesla by providing more convenient places (and possibly prices) for Tesla owners to charge their vehicles. Below is our recent deep dive writeup on CHPT.

Tesla even has competition in self-driving technologies, something it has been a pioneer in. Perhaps the competition in this area is less significant for Tesla, as Tesla most probably won't commercialize its self-driving technology outside its ecosystem, but there are companies that are working on similar products. One particular, Mobileye (Intel spin-off that has IPO’d recently), a driver-assist (ADAS) pioneer, is working on its own self-driving system for commercial deployment at scale.

The competition is also intense in other segments of Tesla's business. In solar energy, the company primarily competes with traditional local utility companies supplying energy to Tesla's potential customers. There is also a growing number of solar energy companies that provide products and services similar to Tesla. Solar projects are relatively quick and convenient to develop, and because spending on solar will only increase (by many estimates sevenfold in the next five years compared to the previous five), many more companies will emerge, further making the competition even more fierce.

A similar picture is in the energy storage business. The competition comes from both established and emerging companies with comparable products or alternatives. As previously mentioned, STEM is the largest competitor in this segment, capable of capturing the largest share of the overall market.

Elon Musk wouldn't be Elon Musk if he did not foresee the growth in competition. He actually contributed to the rise of this competition by pledging not to initiate any lawsuit against anyone who uses Tesla's patents related to EV technology (for so long as such a party is acting in good faith). In other words, Musk made Tesla's patents for free to encourage the advancement of a common, rapidly-evolving platform for electric vehicles for the benefit of all companies making electric vehicles and the world in general.

Tesla does innovate at a grand scale, and as previously established, technology does serve as a competitive advantage, especially on the cost-cutting front (making cars more affordable without losing the quality so that no competitor can't match the price for the same specs), mass manufacturing (building electric cars much faster than anyone else in the industry), and autonomous driving (with the rich data it generates every day, Tesla is set to become the first company to achieve the full self-driving, many years ahead of any competitor).

Another competitive advantage and perhaps Tesla's most valuable asset is its brand. Tesla's brand name became synonymous with electric vehicles and innovation in this space. Anyone considering buying a car knows Tesla not only as the company that sells electric vehicles but as the company that sells the best electric vehicles today. Tesla vehicles probably won more car awards than any other car manufacturer. And one may argue that new entrants in the space, like Lucid, now offer a superior car to Tesla, but Tesla continues to sell vehicles by numbers Lucid won't see in the foreseeable future (if ever). Tesla reached the status of a mass market brand, while Lucid remains a small niche player.

Tesla has such a powerful brand that it literally does not need any advertising and marketing. While competitors will spend millions on ads, Tesla will spend millions on making its technology even more advanced.

Some believe that Elon Musk himself is a competitive advantage regardless of his controversial reputation. Not only does he have serious skin in the game (Musk owns a considerable share of the company), he is perhaps one of the most prolific entrepreneurs and CEOs of our generation, someone who runs several companies at the same time, solving the biggest problems of humanity.

Musk became a cult for millions of people who follow him on social media. And while Twitter (after its recent acquisition by Musk) may be a severe distraction for him and a reputational risk for Tesla, it does not stop Musk from successfully leading Tesla (at least at the time of this writing).

The greatest leaders are great because they can build incredible teams around them. Nothing will be possible at Tesla without its people. People are another competitive advantage for Tesla. And Musk clearly acknowledges it, mentioning at every single Tesla event how the team is vital in the company's recent progress and success.

Management

Not many people know the team behind Tesla, as Musk usually steals the show. But the team plays a significantly more vital role than its famous leader.

To begin with, none of the original founders (of Tesla Motors) are with the company. Some noticeable executives have also left the company in the past several years, including Jerome Guillen (former President of Trucking and Automotive, who also led the engineering team since 2012 and informally was a core leader at the company) and JB Straubel (one of the Tesla founders (not Tesla Motors), who was a Chief Technology Officer at Tesla for 15 years and who basically made Tesla what it is today).

The current executive team consists of just two more people besides Elon Musk, and both have, too, been with the company from its early days.

Zachary Kirkhorn has been with Tesla since 2010 and has served as a Chief Financial Officer (also called Master of Coin within the company) since March 2019. Previously, Kirkhorn served in various finance positions at Tesla, including most recently as Vice President, Finance, Financial Planning, and Business Operations. Kirkhorn holds dual B.S.E. degrees in economics and mechanical engineering and applied mechanics from the University of Pennsylvania and an M.B.A. from Harvard University.

Andrew Baglino joined Tesla back in 2006 as one of the first key employees. He is now a Tesla veteran and has been serving as the Senior Vice President, Powertrain and Energy Engineering since October 2019. Previously, Baglino served in various engineering positions. He holds a B.S. in electrical engineering from Stanford University.

Tesla's board of directors plays a critical role in the company's success. Most significant decisions come from the board, and its members are probably the only people who can stop Musk from doing some crazy things.

The board has been under fire in the past for lack of members with relevant automotive experience, but it recently started to look much stronger.

Among noticeable board members are:

Robyn Denholm (board member since 2014, one of the few with automotive experience, served at Toyota Motor Corporation Australia for seven years);

Ira Ehrenpreis (board member since 2007, an early investor in SpaceX, founder and chairman of one of the most prominent annual energy innovation industry events, the World Energy Innovation Forum (WEIF), served on a number of industry boards, served as the chairman of the Silicon Valley Technology Innovation & Entrepreneurship Forum, active leader at Stanford University);

Kathleen Wilson-Thompson (board member since 2018, previously served in many roles at Walgreens Boots Alliance, a global pharmacy and well-being company, from 2010 to 2021, and also spent 17 years at Kellogg);

James Murdoch (board member since 2017, held a number of leadership roles at Twenty-First Century Fox, a media company, over two decades, including its Chief Executive Officer from 2015 to March 2019);

Joe Gebbia (board member since 2022, co-founder and board member of Airbnb).

Culture

Tesla is a highly mission-driven company with one of the most vital missions among all public companies. Its mission, "to accelerate the world’s transition to sustainable energy," helping humanity exit the fossil fuel era, affects probably all people on earth.

Very few companies have such an impact as Tesla, even though only a small fraction of the global population will ever be able to use Tesla's products.

Tesla has a vision of a world powered by solar energy, running on batteries, and transported by electric vehicles. This is one of Musk's central beliefs and life goals. He is one of those rare executives who wants to leave a real impact for hundreds of years.

“I will do everything to accomplish Tesla's mission and make the world better.” – Elon Musk.

No wonder so many people around the world love Musk, support the company, and want to be a part of it, whether by driving one of its cars, being its shareholder, or working at the company.

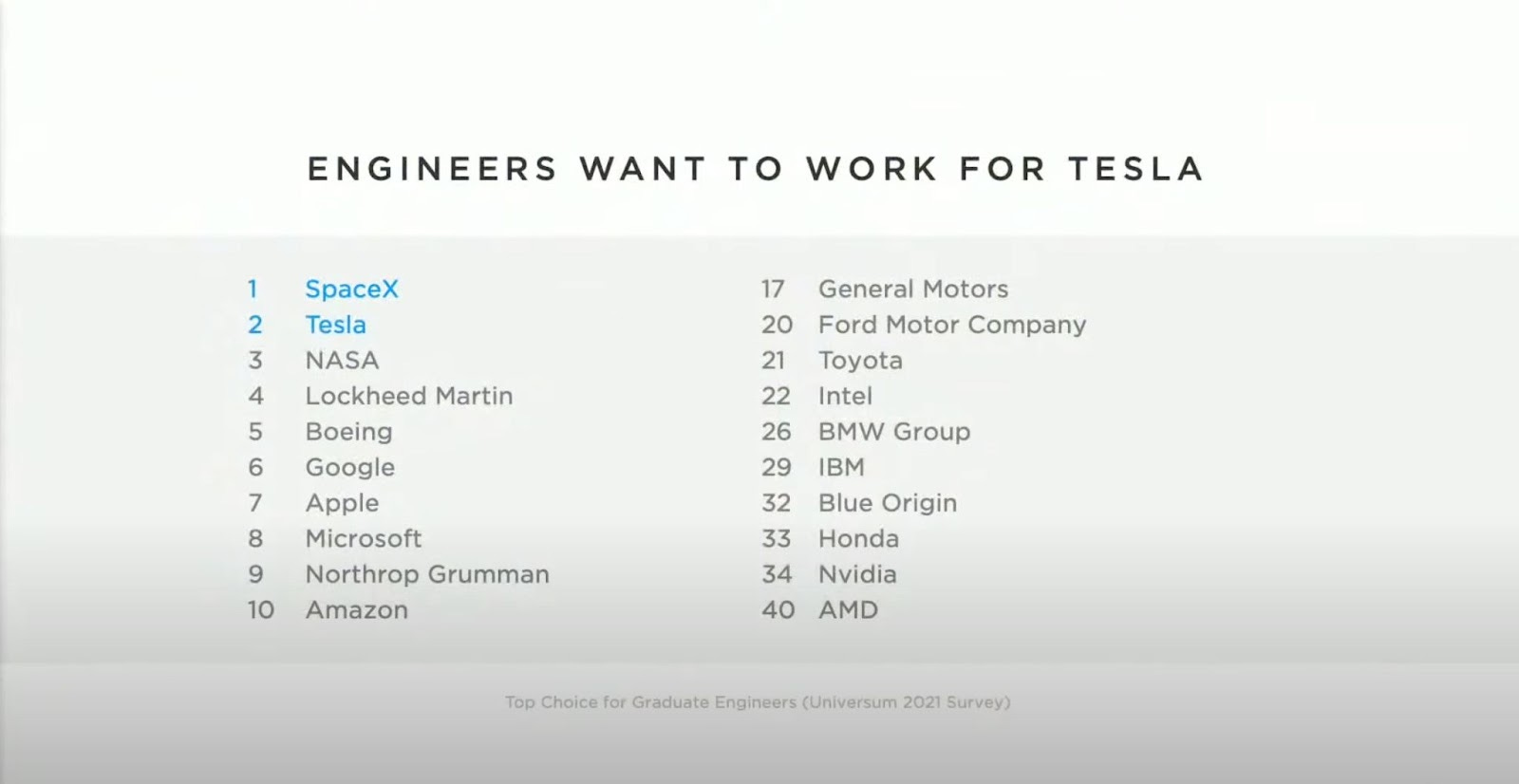

The world's brightest minds strive to work at Tesla. Perhaps, more than anywhere else (except SpaceX). These two companies will profoundly impact our lives here on earth and maybe one day somewhere on the other planet.

“Where the smartest engineers want to work, that company is most likely to succeed big.” – Elon Musk.

Headquartered in Austin, Texas, United States, Tesla currently provides more than 100,000 people with impactful work across three continents.

The company is driven by its culture of open communication, which is more typical for technology companies rather than car manufacturers. Tesla, on average, provides a highly competitive wage that meets or exceeds wages in comparable manufacturing roles, not factoring equity and other benefits. All Tesla employees are eligible to receive Tesla stock yearly, depending on their performance.

Tesla has pretty strong ratings on both Glassdoor and Comparably. Glassdoor's rating of 3.6 / 5 seems a bit modest, but it is based on over 8,000 reviews, which have been left throughout many years. Most negative reviews are about work/life balance. Elon Musk has a strong CEO approval rating of 73% based on a solid more than 3,700 ratings.

On Comparably, Tesla scores a B+ rating for culture based on 858 employee participants and over 5,800 total ratings. Elon Musk has a CEO rating of 78/100 (A) based on 601 employee ratings. Tesla ranks in the Top 10% of other companies on Comparably with 10,000+ Employees for CEO Rating Score.

Financials

All information in this section is based on the financial performance of Tesla as of the end of Q3 2022, reported on October 19, 2022.

"Q3 was another record quarter on many levels. We had our industry-leading operating margin reach 17%. And our free cash flow surpassed $3 billion in Q3 and approached $9 billion in the past 12 months.

We have excellent demand for Q4, and we expect to sell every car that we make for as far into future as we can see. So, the factories are running at full speed, and we’re delivering every car we make and keeping operating margins strong. We are still a very small percentage of the total vehicles on the road. Of the 2 billion cars and trucks on the road, we only have about 3.5 million. So, we’ve got a long way to go to even reach 1% of the global fleet.

We have an incredible product portfolio. I think we’ve got the most exciting product portfolio of any company on earth. We’re in the final lap for Cybertruck. We’re building a Cybertruck line here at Giga Texas and making a lot of progress in the robotaxi platform design.

I think it’s an incredibly exciting future and really an unprecedented future." – Elon Musk on Q3 2022 earnings call.

Income Statement

Revenue

Revenue in the third quarter of 2022 was $21.45 billion, a 56% YoY increase and 27% sequential growth over the prior quarter of 2022.

The analysts' consensus for revenue was $21.88 billion. Tesla missed revenue by $428.34 million or 1.96%. It was the first miss in the last 12 quarters.

Automotive revenue grew 55% compared to the same period last year, while Energy generation and storage revenue saw a 39% YoY increase, and Services and other saw an 84% YoY increase.

The solid YoY growth in Q3 2022 was impacted by growth in vehicle deliveries, increased average sales price (ASP), and growth of other business segments. Revenue was negatively affected by a strong dollar.

For nine months of 2022, the total revenue was $57.14 billion, a 58% growth over the same period last year. The revenue in three quarters of 2022 has already exceeded the total revenue for the entire of 2021.

Gross Margin

The total gross margin in the third quarter of 2022 was 25.09%, a decrease of 152 basis points or 6% from the prior year period. This was driven by the changes in automotive sales revenue and cost of automotive sales revenue, which led to a lower automotive gross margin (decreased from 30.5% to 27.9% in Q3 2022 compared to Q3 2021).

The cost of automotive sales revenue grew by 61% compared to Q3 2021 due to rising raw material, commodity, logistics, and expedite costs, the ramping up of production at Gigafactory Berlin-Brandenburg and Gigafactory Texas, and the proprietary battery cells manufacturing.

"Removing regulatory credits and Austin and Berlin, our operating margins would have been our strongest yet, and auto gross margin would have been nearly 30%. Each car we build in Austin and Berlin is contributing positively to profitability." – from Q3 2022 earnings call.

However, for nine months of 2022, the total gross margin increased to 26.38%, an improvement of 110 basis points compared to the gross margin of 25.28% for the full year of 2021.

The total gross profit was $5.38 billion, an increase of 47% from the $3.66 billion reported in the third quarter of 2021, primarily due to the higher revenue.

Operating Expenses

Operating expenses grew 6% YoY to $1.6 billion. R&D expenses increased by 20% YoY primarily due to a $47 million increase in employee and labor-related expenses, a $29 million increase in R&D expensed materials, a $24 million increase in facilities, outside services, freight, and depreciation expense, and a $19 million increase in stock-based compensation expense.

SG&A continued to improve and showed a decrease of 3% primarily due to a decrease of $184 million in stock-based compensation expense, most of which is attributable to the lower stock-based compensation expense of $185 million on the 2018 CEO Performance Award.

Despite this growth, operating expenses as a percentage of total revenue keep improving. Tesla does a tremendous job increasing revenue while achieving operational efficiencies, in addition to decreasing operating expenses.

Profitability

Tesla achieved profitability on an Adjusted EBITDA basis back in 2017 and on a Net Income basis in 2020. It has been increasing its profitability ever since.

"On automotive profitability, our GAAP operating margin was 17.2%, with automotive gross margin at 27.9%. Operating margin is one of our best yet, with improvements in operating leverage. However, Austin and Berlin ramp costs weighed on our margins, particularly if you compare it to Q1.

On energy profitability, we achieved our strongest gross profit yet for this business, driven primarily by record volumes of our Megapack and Powerwall products." – from Q3 2022 earnings call.

In Q3 2022, the operating gross margin was 17.2%. Tesla delivered a record operating profit of $3.7 billion.

EPS in Q3 2022 was $1.05 compared to $0.54 in the same quarter last year. The consensus was $1.00 (beat by $0.05 or 5.23%).

Guidance

Tesla does not provide detailed guidance, but management includes commentary on the outlook.

"As we look ahead, our plans show that we’re on track for 50% annual growth in production this year, although we are tracking supply chain risks which are beyond our control. On the delivery side, we do expect to be just under 50% growth due to an increase in the cars in transit at the end of the year.

Austin and Berlin ramp costs will continue to weigh on margins, although we expect the impact to be less than what we saw in Q3. We are continuing to build as many cars as possible while also maintaining strong operating margins." – from Q3 2022 earnings call.

Analysts' consensus for Q4 2022 revenue is $26.37 billion (48.84% YoY growth). For the full year of 2022, they expect $83.38 billion, which represents a 54.92% increase over 2021.

Balance Sheet

The company ended the quarter with $21.10 billion in cash and cash equivalents and marketable securities. The company has around $2 billion in debt and finance leases. In Q3 2022, the company made debt repayments of $0.9 billion.

The stock-based compensation (SBC) in the quarter was $362 million, a decrease of 23.76% from the quarter a year prior. As a percentage of revenue, SBC was just 1.69%, a very healthy percentage for a technology company.

Since going public in 2010, Tesla has increased the number of shares outstanding by 126% while delivering a stock price appreciation of a whopping 11,000%+.

In the last 12 months, the dilution was a moderate 1.9%, while the stock price decreased by 51%.

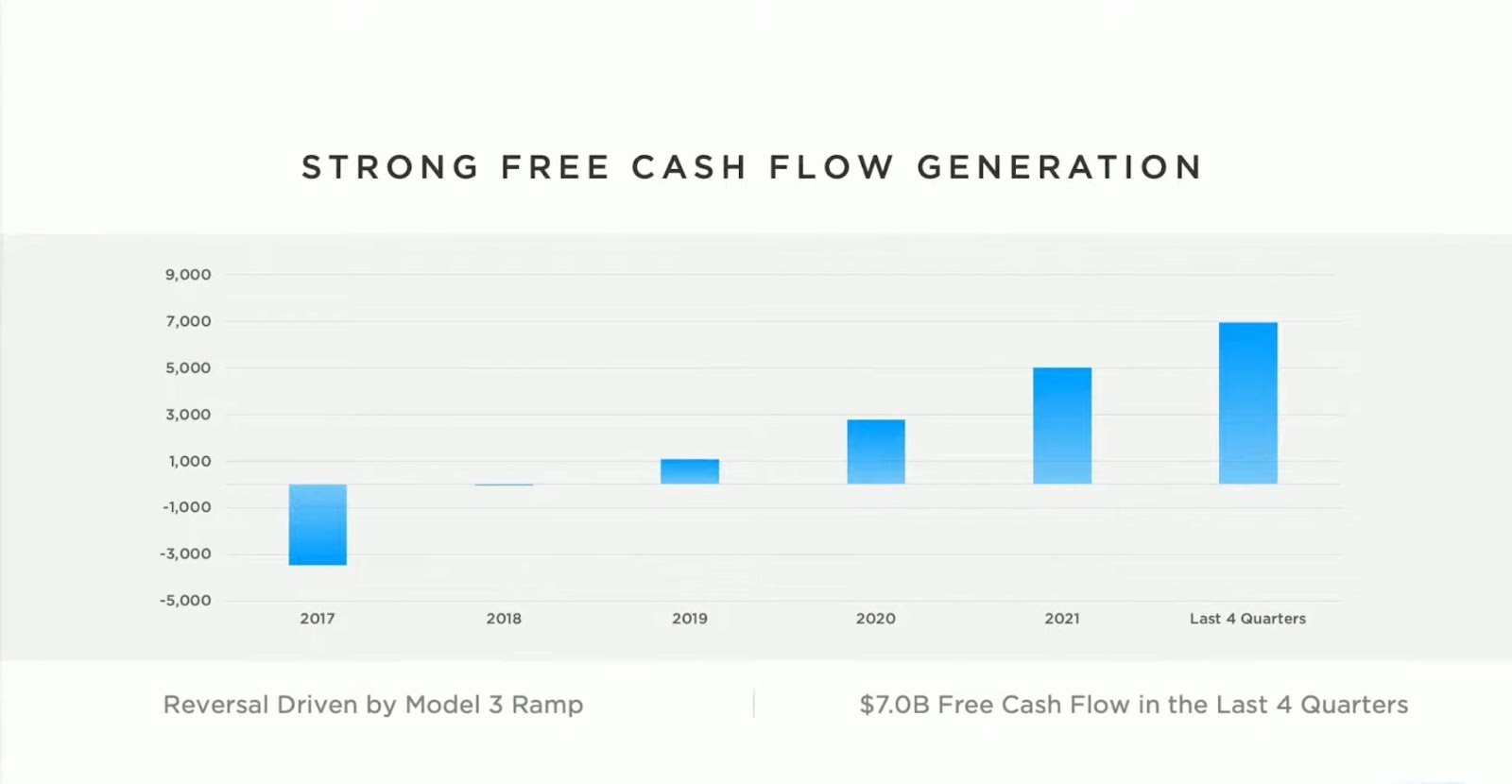

Cash Flow

Tesla had a record free cash flow (FCF) in Q3 2022 of $3.3 billion. In the past 12 months, FCF exceeded $8.9 billion.

Tesla continuously generates more cash than it spends.

Key Metrics

Besides financial metrics, Tesla reports several operational metrics that help evaluate the overall growth and health of all business segments.

These metrics include:

The number of total vehicle production (by models);

The number of total vehicle deliveries (by models, including those in the operating lease);

The number of total operating lease vehicle count (how many cars are in the operating lease);

Global vehicle inventory days of supply (inventory divided by deliveries);

Solar deployed (in MW);

Storage deployed (in MWh);

Store and service locations (globally);

Mobile service fleet (number of mechanics);

The number of Supercharger stations;

The number of Supercharger connectors (sold both to individual and commercial clients).

Risks

Tesla is exposed to a number of risks, including risks specific to its business, industry, regulations, and operations, as well as some other risks related to Elon Musk.

Below are some critical risks worth considering:

Dependence on regulatory credits (the more companies meet emissions targets, the less they will require buying credits from Tesla. Long-term, Tesla will see a significant decline in this revenue stream);

Significant dependence on Elon Musk and the risk if he decides to appoint an outside CEO;

Brand reputation risk with recent Musk’s takeover of Twitter;

Skyrocketing lithium, cobalt, and nickel prices that push the price of EV battery packs up, increasing the price of EVs and driving their adoption back;

The pace of production ramps in Texas and Berlin-Brandenburg factories;

The introduction of new products and manufacturing technologies on time;

Regulation risks for self-driving technology, which may push the introduction of robotaxi service farther away (if ever);

The rapid growth in competition (covered in detail in the Competitive Advantages section) and, as a consequence, Tesla's market share drop;

A possible recession that will push Tesla sales down and slow revenue growth.

Ownership

According to the latest proxy statement (DEF 14A) filed on June 23, 2022, the ownership structure of the company looks the following way:

The beneficial ownership percentages in the table above are based on 1,035,976,271 shares of Common Stock outstanding as of March 31, 2022.

In August 2022, Tesla completed a 3-1 stock split, increasing the number of shares three times (3,107,928,000 shares).

Since then, the company has issued additional 38,072,000 shares (1.2% of total shares). The information below is based on approximately 3,146,000,000 shares outstanding as of Q3 2022.

Tesla's largest shareholder is Elon Musk. On the date of the latest proxy statement, he held approximately 796,465,818 shares (~25% of the company). Since then, he has sold around 72,207,000 shares (about 9% of his entire holding) worth approximately $19 billion.

Another insider with a significant share (~1.4%) is an ex-board member of Tesla, Larry Ellison, a co-founder and executive chair at Oracle.

The largest outside investors are The Vanguard Group (6.7%), BlackRock (5.4%), State Street Global Advisors (3.1%), and Capital Research and Management Company (3.1).

Valuation

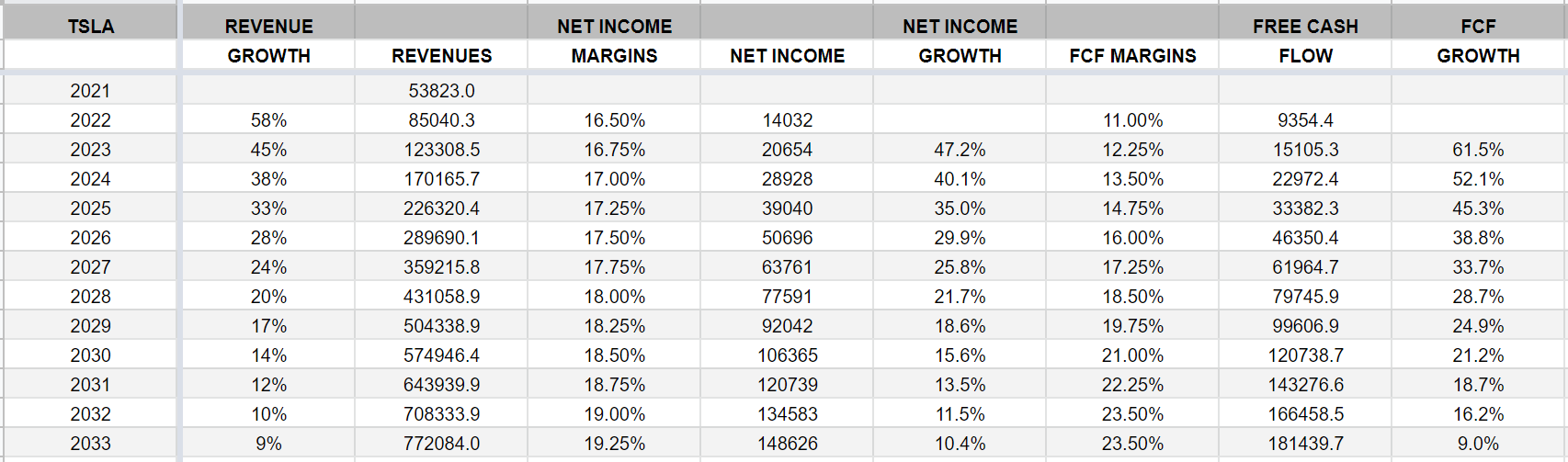

Talking about TSLA’s valuation is finally fun because it’s come down so much the past year. Not too long ago TSLA had a P/E in the triple digits and even though they were growing revenues by 50% and EPS much faster than that, we knew the P/E would need to contract, it wasn’t a matter of “if” it was “when” and that “when” has now passed because the P/E went from 200x in early 2021 to 32x in late 2022 despite the fundamentals and balance sheet continuing to get stronger every quarter.

Even though TSLA is becoming a mature company they continue to show impressive top & bottom line growth. I’ll be using the estimates below for the following valuation metrics, including the current enterprise value of $551 billion and the current stock price of $179.05

Using 2022 estimates, TSLA is trading at:

6.6x EV/sales

27.8x EV/EBITDA

38.2x EV/Net Income

60.5x EV/FCF

Using 2023 estimates, TSLA is trading at:

4.7x EV/sales

19.5x EV/EBITDA

27.7x EV/Net Income

36.1x EV/FCF

It’s probably not a coincidence (or maybe it is) that TSLA is currently trading at 38x 2022 EV/net income when they’re expected to grow net income by 38% in 2023. Often times you see stocks at the end of the year getting priced at multiples based on the following year’s estimates. You’ve probably noticed this in my investment models (next section) where I use the following years earnings (or net income) growth as my multiple for the current year, this isn’t always true but I think it’s the right/conservative way to build models and give yourself some cushion. To expand on this further, TSLA might have grown EPS and net income by 70-80% this year but it would be unreasonable to expect TSLA to trade at 70-80x earnings if they can’t keep up that growth. If earnings growth going forward is going to be in the 30% range than it’s reasonable to assume that TSLA should trade at a similar P/E multiple, perhaps a slight premium which would be a 1.2x to 1.4x PEG ratio or 1.2x to 1.4x the expected earnings growth rate meaning if TSLA is expected to grow earnings by 36-38% next year then I think it’s fair if TSLA traded at 36-38x earnings up to 43-53x earnings (if the market thinks they deserve to trade at a premium). As an example of stocks that trade at a big premium, just look at AAPL, they’re growing earnings by 8-10% per year yet they trade at 23x earnings. I’m not suggesting that TSLA should trade with the same PEG ratio as AAPL but it’s not ludicrous to think that TSLA could/should trade at a premium PEG ratio, especially in a bull market if interest rates are coming back down. Not to skip ahead to the investment model stuff but throw a 48x P/E on $5.71 (non GAAP EPS) next year and you get a $274 stock — I think this is the bull case for TSLA in 2023 which is 53% higher from here. If TSLA hits that $5.71 number next year and trades with a 1.0x PEG ratio (assuming 38% YoY growth) then you have a $217 stock which is 21% higher from here.